Comentário Diário | 23/05/2019

USD gets little to no support from Fed’s minutes

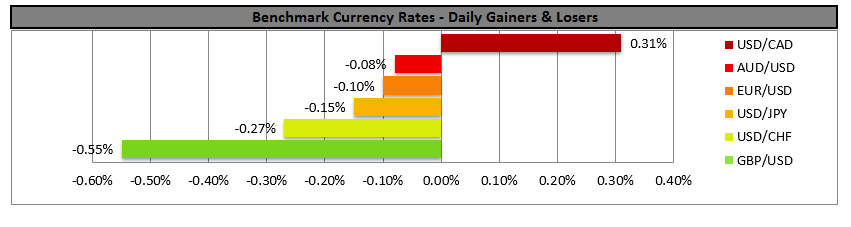

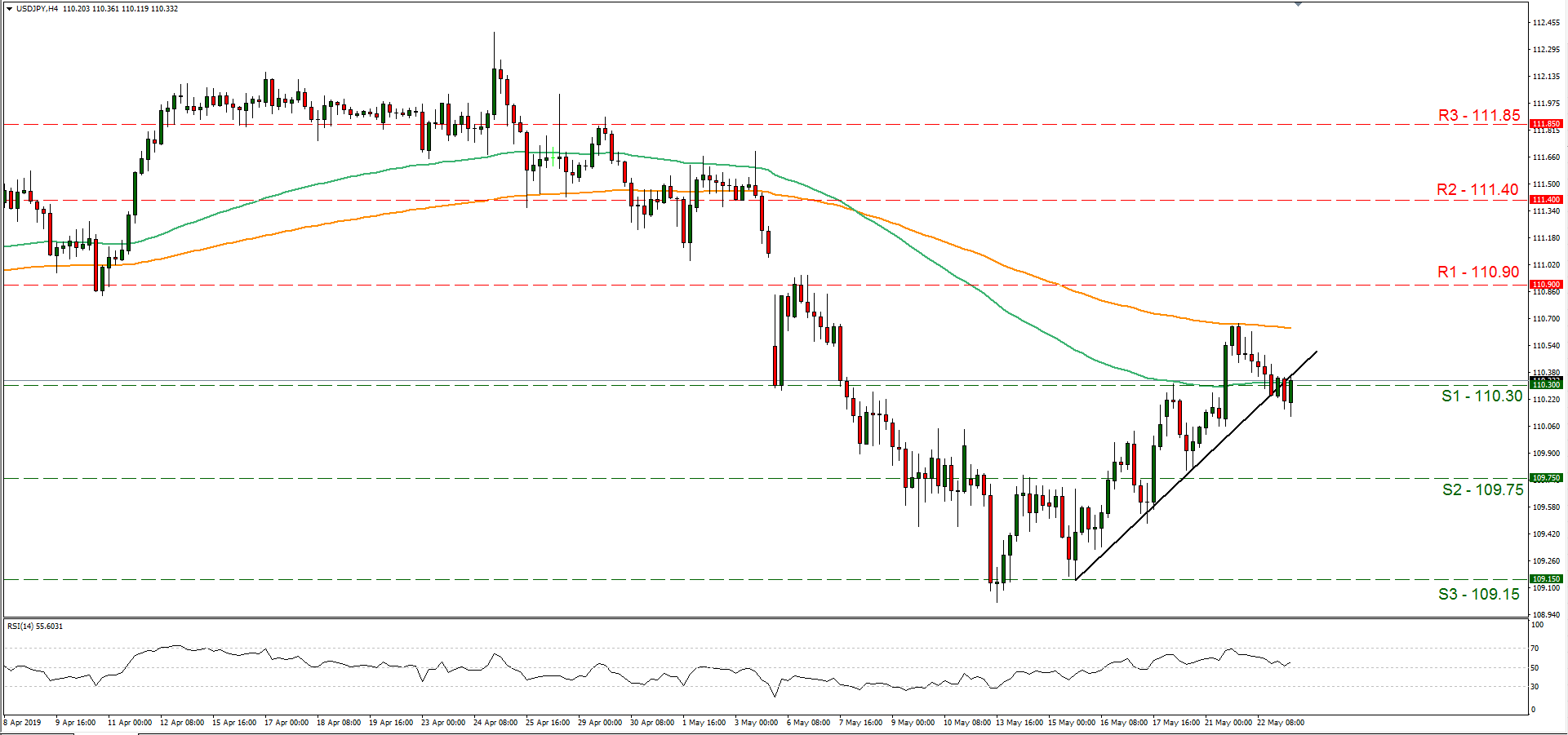

The USD produced little gains from the Fed’s minutes, remaining mostly flat against its major counterparts yesterday. The minutes revealed that there is support among the Committee's members to Powell’s opinion that inflation weakness is due to transitory factors. Also the minutes show a support for a patient approach for some time, even should global conditions improve. The Fed also discussed arguments for and against shortening the bond portfolio maturity levels. We see the case for the Fed to maintain a bias towards a neutral stance towards the interest rate level despite past expectations of the market of a possible rate cut. There could be a slight support for the USD, given the implied temporary nature of the inflation dip. USD/JPY stabilised lower yesterday, testing the 110.30 (S1) support line. Technically, it should be noted that the pair’s price action has broken the upward trendline incepted since the 15th of May hence we switch our bullish outlook, in favour of a sideways scenario. Should the bulls once again take over, we could see the pair aiming if not breaking the 110.90 (R1). Should the bears take over, we could see the pair breaking the 110.30 (S1) and aim for the 109.75 (S2) support level.

Oil prices weaken as there is a new injection in US oil inventories

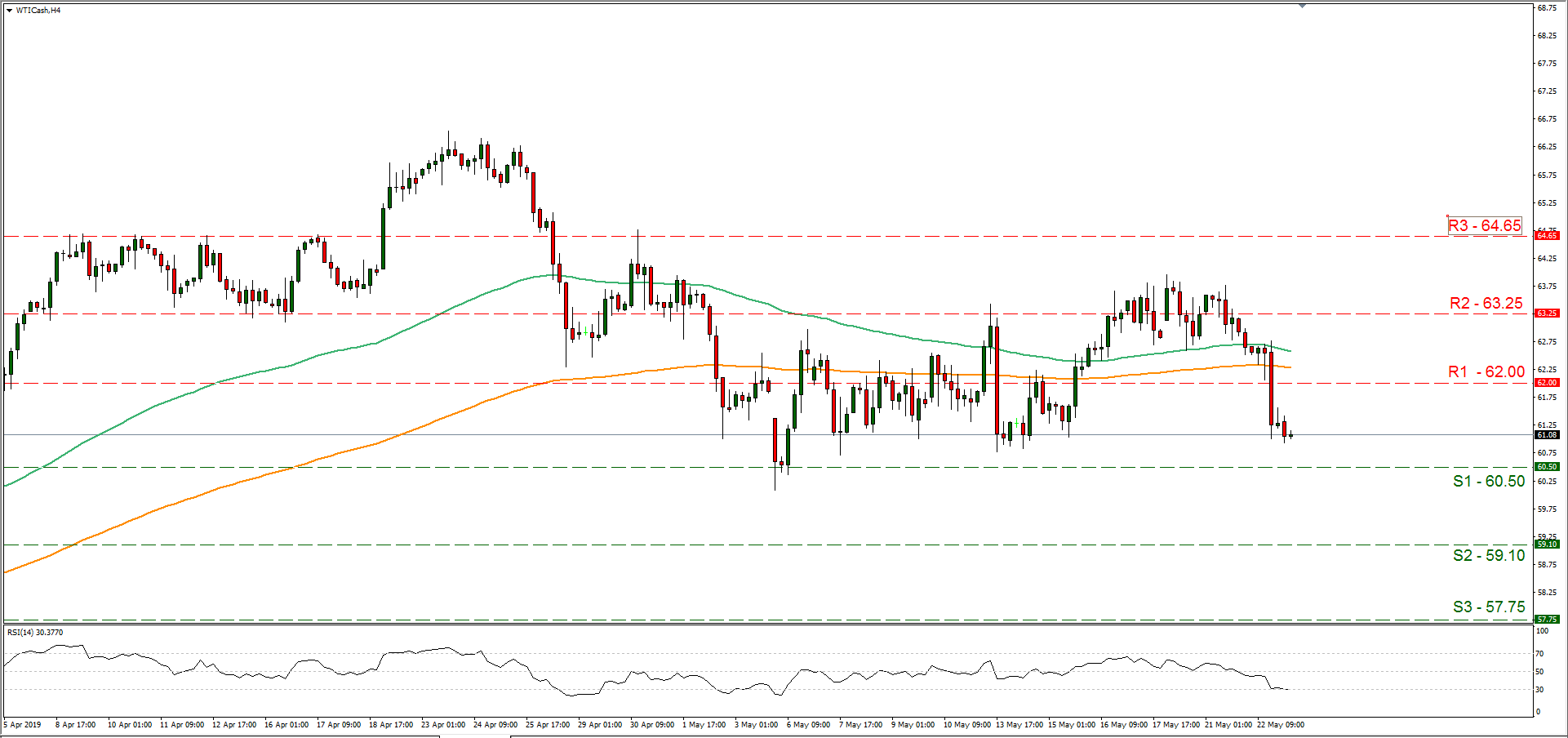

Oil prices weakened yesterday, as the US crude oil inventories showed another injection and economic worries were enhanced. The EIA crude oil inventories figure was another injection, this time of 4.74 million barrels, which underscored the slack in the US oil market. Also analysts tend to point out that the US-Sino trade war may have a detrimental effect on oil demand as prices as a slowdown may reoccur. On the flip side the production cuts and US-Persian tension continue to provide support for oil prices. On the short term we could see oil prices weakening as the slack in the US oil market persists, yet OPEC production cuts could support oil prices. Oil prices dropped yesterday, breaking the 62.00 (R1) support line (now turned to resistance). As the slack in the US oil market seems to persist, we could see oil prices maintain the bearish momentum. It should be noted though that oil prices could prove sensitive to fundamental news especially headlines relating to OPEC production levels and on second base the US-Sino trade wars. Should WTI long positions be favored by the market, we could see it breaking the 62.00 (R1) resistance line and aim for the 63.25 (R2) resistance hurdle. On the other hand, should the commodity be under the selling interest of the market, we could see it breaking the 60.50 (S1) support line and aim for the 59.10 (S2) support barrier.

Other economic highlights, today and early tomorrow

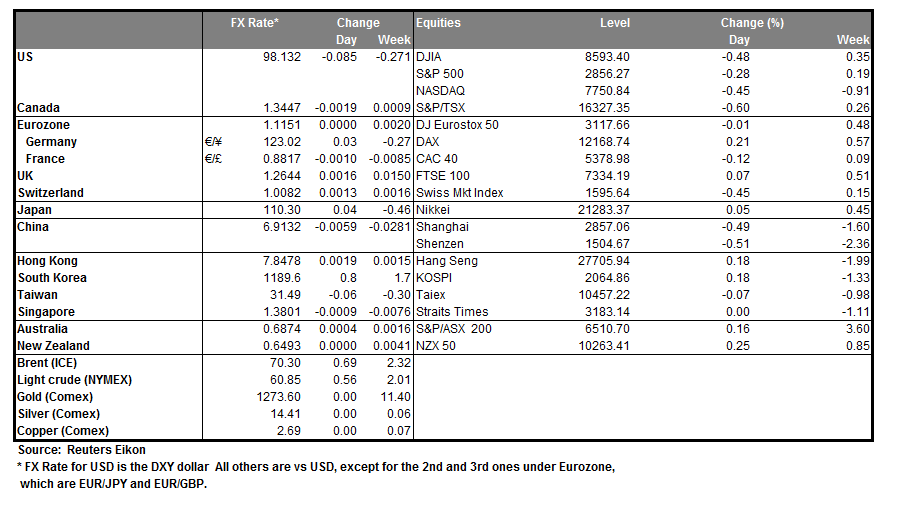

In the European session, we get from Germany the GDP for Q1, the preliminary Markit manufacturing PMI for May and the Ifo Business climate for May. From Eurozone, we get the preliminary Markit composite PMI for May and ECB is to release the account of the last policy meeting. In the American session, we get the US new home sales figure for April. In tomorrow’s Asian session, we get the Japan’s inflation rates for April. As for speakers, Fed’s Kaplan, Barkin, Bostic and Daly and ECB’s De Guidos speak.

WTI H4

• Support: 60.50 (S1), 59.10 (S2), 57.75 (S3)

•Resistance: 62.00 (R1), 63.25 (R2), 64.65 (R3)

USD/JPY H4

• Support: 110.30 (S1), 109.75 (S2), 109.15 (S3)

•Resistance: 110.90 (R1), 111.40 (R2), 111.85 (R3)