Comentário Diário | 16/05/2017

RBA minutes pack few surprises

• The minutes of the latest RBA policy meeting contained no surprises and more or less reflected the meeting statement. There was little in the minutes to suggest that there may be a change in policy anytime soon, which is consistent with our view that the RBA is likely to keep its powder dry in the foreseeable future. Given that we got no new information with regards to the Bank’s forward guidance, the Australian dollar moved little at the release. Perhaps the most noteworthy point in the minutes was that officials remain worried about the labor and housing markets. Given the Bank’s focus on the labor market, we think that the next major market mover for the Aussie is likely to be the employment report for April, due out during the Asian morning Thursday. Besides Australian data, we think that much of AUD’s forthcoming direction is also likely to be decided by the path of iron ore prices, investors’ risk sentiment, as well as incoming Chinese data, considering Australia’s heavy trade exposure to the world’s second largest economy.

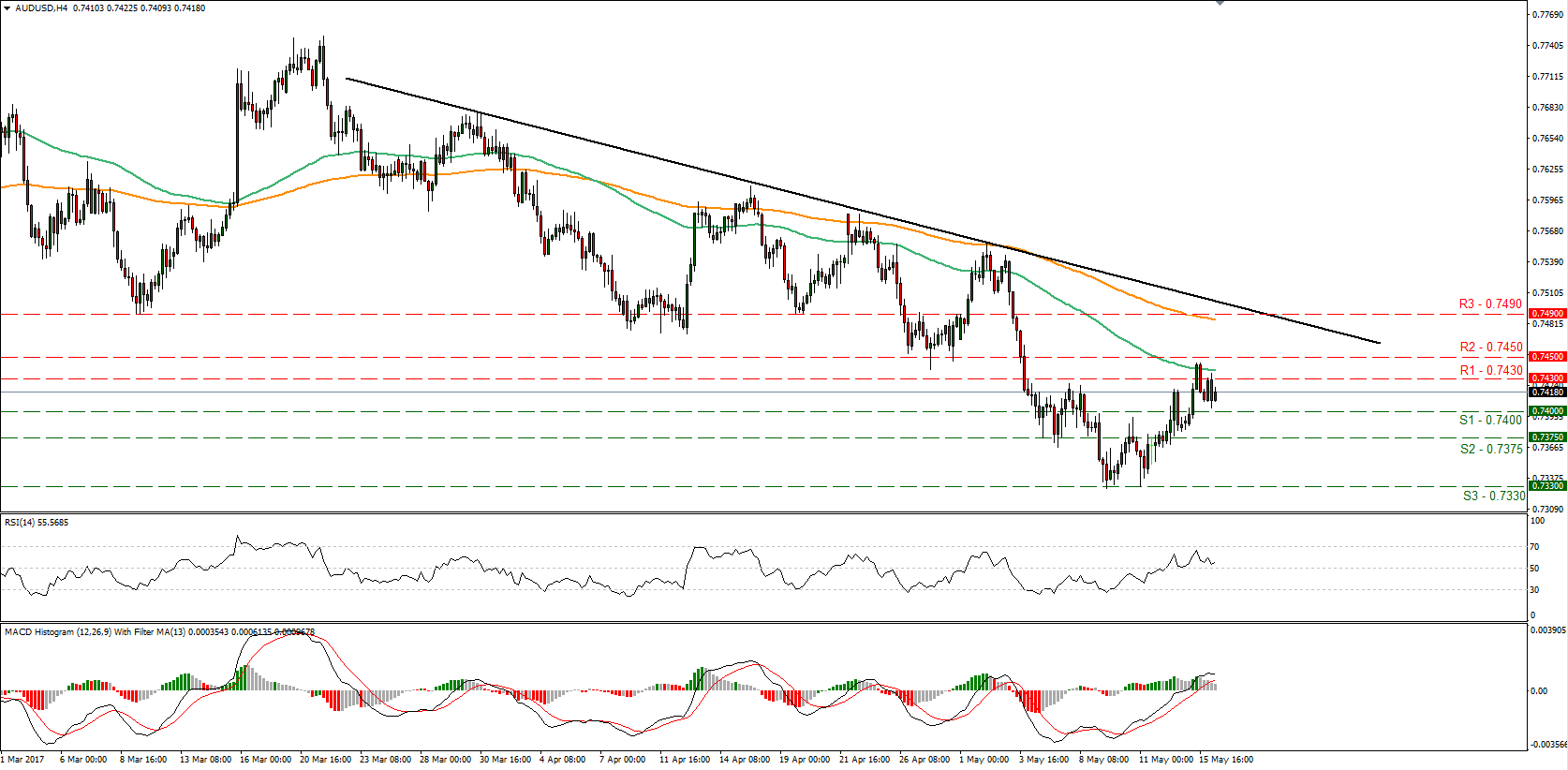

• AUD/USD traded lower yesterday ahead of the minutes, and moved little on their release. Given that the rate is still trading below the downtrend line taken from the peak of the 30th of March, we believe that the short-term trend remains negative. Nevertheless, we see the possibility for the pair to turn up again and continue correcting north. A break above 0.7450 (R2) could confirm the case and is possible to open the way for a test near the crossroad of the 0.7490 (R3) hurdle and the aforementioned downtrend line. The catalyst for more upside corrective extensions may be Thursday’s employment data, where the net change in employment is expected to stay positive even following the previous month’s remarkable surge.

Today’s highlights:

• During the European day, the main event will probably be the release of the UK CPI data for April. The forecast is for both the headline and the core rates to have risen notably, something supported by the nation’s services PMI for the month, which indicated that service firms raised their prices charged at the fastest pace since 2008. Even though something like that could bring the pound under renewed buying interest, we stick to our guns that the Bank of England is likely to remain on hold in the foreseeable future should the data evolve more or less in line with its expectations. What’s more, we think that sterling’s forthcoming direction over the next weeks is likely to be decided primarily by news surrounding the upcoming General Election, rather than developments regarding monetary policy.

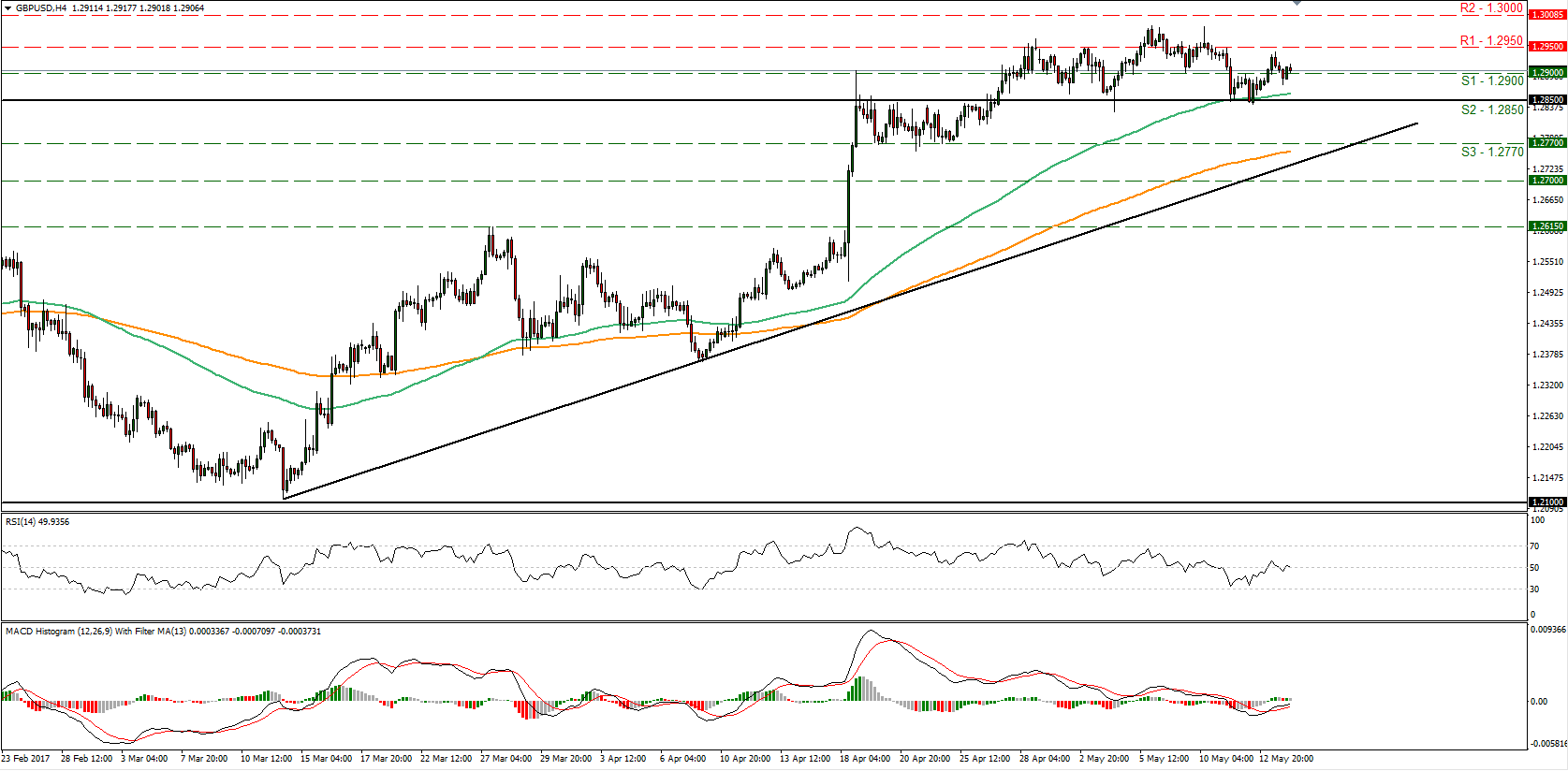

• GBP/USD traded in a consolidative manner yesterday and during the early European morning Tuesday, it is trading near the 1.2900 (S1) barrier. Bearing in mind that the pair has been oscillating between the key support of 1.2850 (S2) and the psychological zone of 1.3000 (R2) since the 27th of April, we consider the short-term outlook to be neutral for now. Nevertheless, accelerating CPIs today could encourage the bulls to target the 1.2950 (R1) zone, where a decisive break may trigger extensions towards the round figure of 1.3000 (R2).

• From Germany, we get the ZEW survey for May. The consensus is for both the expectations and the current conditions indices to have risen. This would probably be an encouraging development for ECB policymakers, as it could signify that the bloc’s economic powerhouse continues to perform at a robust pace. We also get Eurozone’s trade balance for March and the second estimate of Q1 GDP. From the US, we get building permits, housing starts, and industrial production, all for April.

• We have only one speaker on the agenda: ECB Executive Board member Benoit Coeure.

AUD/USD

• Support: 0.7400 (S1), 0.7375 (S2), 0.7330 (S3)

• Resistance: 0.7430 (R1), 0.7450 (R2), 0.7490 (R3)

GBP/USD

• Support: 1.2900 (S1), 1.2850 (S2), 1.2770 (S3)

• Resistance: 1.2950 (R1), 1.3000 (R2), 1.3050 (R3)