Week Ahead | 31/05/2019

Weekly outlook: June 3rd to 7th | Brexit, ECB’s and RBA’s interest rate decisions, along with US employment report to move the markets

Brexit and to be more specific developments in the inner UK political stage after Theresa May’s announced resignation are expected to move the pound. At the same time we get a number of financial releases which could have substantial effects on their respective currencies. Starting with the Eurozone ECB’s interest rate decision, could have a substantial effect on the common currency. Also, RBA could be cutting interest rates for the first time in a number of years and the Aussie could weaken even further. Last but not least on Friday, the greenback could be rattled by the release of the US employment report for May. On the fundamentals, the enhancement of the uncertainty about global trading conditions and worries for a possible slowdown could continue to affect the markets.

AUD – RBA’s interest rate decision and a number of releases to move the Aussie

Aussie traders are to have a busy week ahead as a plethora of financial releases relating to the AUD are due out. Starting with the most important, the RBA is to release its interest rate decision on Tuesday during the Asian session and is widely expected to cut rates by 25 basis points (bp), lowering the level to +1.25%, from current +1.50%. Currently the market seems to have priced in such a rate cut as AUDOIS imply a probability of 92.0% for such a scenario. Also the market seems to be pricing in another cut in August, in which case the rates are to drop by another 25bp. Other analysts are predicting even a third cut in November, yet for the time being it may be a bit premature. Never the less, should the bank cut rates and also release an accompanying statement with a dovish content which could be paving the way for a second cut (in August maybe) we could see the market reacting bearishly for the AUD. However before that, on Monday we get China’s Caixin PMI for May and should it drop as the NBS manufacturing PMI for May did today, the market maybe discounting the AUD even before RBA’s interest rate decision. Also the release of Australia’s retail sales for April could have a bearish effect for the Aussie, should it decelerate. However after RBA’s interest rate decision, some ray of hope may come out as on Wednesday the GDP growth rate for Q1 is due out and on Thursday, Australia’s trading balance for April is to be released.

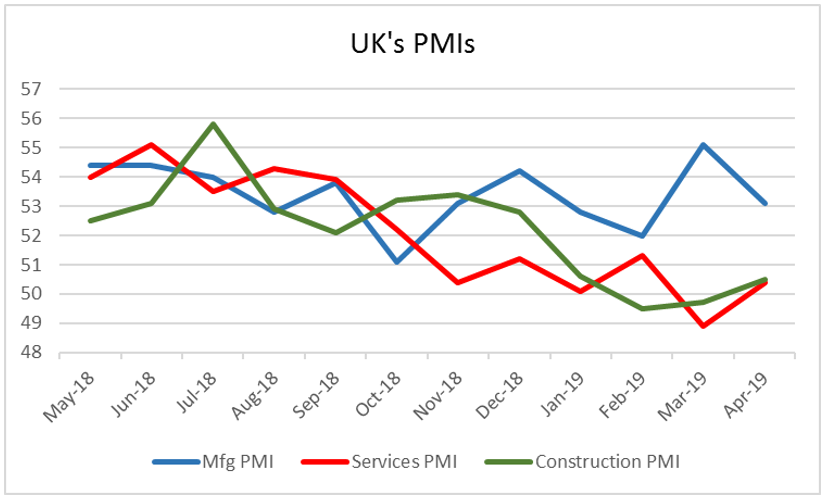

As the new week begins and the UK Parliament reopens, one could expect headlines about the succession of Theresa May dominate the market. Donald Trump’s visit to the UK could stir some interest especially should there be any tweets about Brexit or any possible future trade agreements of the UK with the US. Theresa May is to resign on the 7th of June, and at the current stage Brexit hardliners, seem to be favoured by the result of the EU Parliament elections, to succeed Theresa May. The pound seems to have priced in a number of negative scenarios for Brexit, yet we suspect that it could weaken even further, as developments for her succession roll out. On the financial releases front there do not seem to be any important data to be due out, but the PMIs for May. All three PMI’s (Manufacturing on Monday, Construction on Tuesday and Services on Wednesday) are forecasted to remain rather soft and if so, could have little influence over the pound’s direction. We could see the pound being under pressure next week, if not weaken even further should there be further negative developments in the UK political scene.

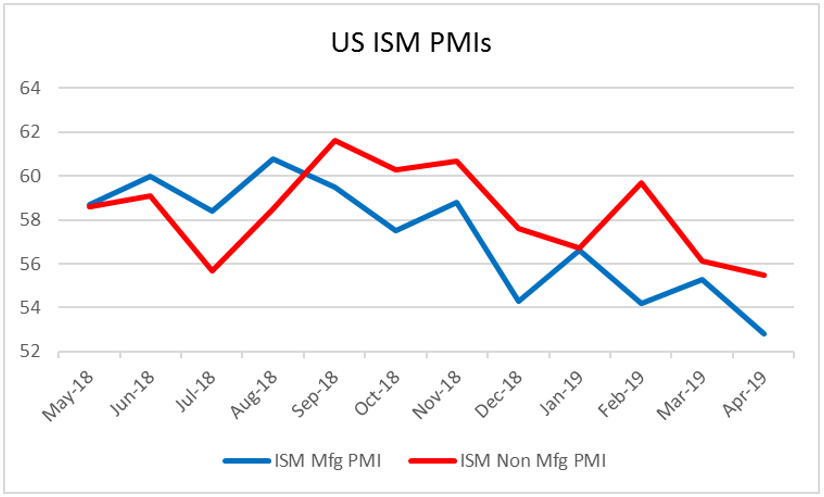

Trump’s threats about imposing tariffs on imports from Mexico, passed through the markets as a hurricane early today. The tariffs are to be imposed from 10th of June, at a level of 5% for all imports from Mexico and gradually rise to reach 25%, until October. The only way to stop this would be to immediately deal with the illegal immigration flow to the US. NAFTA implications are also expected as the move is considered a clear violation of the agreement as well as WTO commitments. The wider trade tension issue is expected to continue to rattle the markets, as fears for a possible global slowdown continue to grow. It would be indicative of the market’s reaction and risk off sentiment, how the greenback retreated against the Japanese Yen, since Thursday. It’s difficult to find any signs of easing on the horizon, in the coming week, hence we could see these tension lingering on if not intensifying. However it would also be interesting to monitor the any statements from Fed officials in the coming week. The market seems to be closely monitoring any statements made, especially after Fed’s Clarida seems to have opened a very small crack for a possible easing of the Fed’s monetary policy in his last statements on Thursday. We expect the opening remarks of Powel in the Fed’s conference (The Fed listens) on the 4th of June to be under scrutiny for any hints, as well as Clarida’s speech. On the financial releases front, before the release of the US employment report for May on Friday in the American session, we could see the ISM manufacturing PMI for May on Monday and the ISM Non-Manufacturing PMI for May on Wednesday could be moving the USD. The US employment report though is to be the star of the week, and should it show some easing of the US labour market, we could see the greenback retreating, at least somewhat. We could see the Non-Farm Payrolls figure dropping somewhat, correcting lower (current forecast for May: 100k) from the previous massive reading of 263k. Never the less we do tend to concentrate also on the average hourly earnings growth rate, which currently is expected to remain unchanged at +3.2% yoy, and despite being at rather descent levels, lack of further progress could undermine further advancements of inflation.

Its not only the US releasing employment data for May, on Friday. At the same time Canada’s employment data for May are due out and we could see the release affecting the Looney. The unemployment rate is expected to tick up reaching 5.8%, if compared to prior month’s reading of 5.7% and should also the employment change figure drop from previous reading of 106.5k (probably) we could see the Lonney weakening. The result could be magnified, given that the GDP rate missed its target for Q1 of +0.7% qoq and settled for +0.4% qoq. Also the somewhat dovish decision by the BoC on Thursday, is not be getting a helping hand from a slack in the Canadian labour market. The bank remains quite data depended and also made it clear that it is quite worried about the developments in the oiil market as well as the globaltrading conditions. Hence we expect Loonie traders to also continue to maintain a watchfull eye over the oil market and should oil prices continue to drop, we could see the CAD mirroring their move.

EUR- ECB interest rate decision along with CPI rates to affect the EUR

ECB’s interest rate decision, is to announce it interest rate decision on Thursday and is widely expected to remain on hold at 0.0%. Currently EUR OIS imply a probability of over 99% for the bank to remain on hold. recent data seem to be more on the soft side and at the current stage we do not see the bank tightening its policy in 2019. We could see the bank leaning more towards further easing, however how this is exactly to take place remains to be seen. It should be noted that fears of a possible Japanification of the Eurozone are still present in the area. We expect the bank to maintain an accomodative stance in the near term, as inflation is not expected to pick up pace substantially reaching the bank’s goal of +2.00% yoy, nor is the GDP growth rate. Also EUR traders are expected to keep watch over the release of Eurozone’s preliminary CPI rate for May, Germany’s industrial orders and industrial output growth rates for April, as well as Germany’s trade balance for April, as the latter three seem to concern the economic engine of the Eurozone.