Week Ahead | 28/06/2019

Weekly outlook: July 1st to 5th | In the aftermath of the G20 meeting and ahead of the US employment report.

With the week expected to begin with any possible repercussions of the G20 summit, especially of the Trump-Xi meeting and ending with the US employment report for June, we could see volatility rising. UK politics on the other hand are expected to take a back seat this week as well, despite the race for Theresa May’s replacement being still on the headlines and UK’s PMI’s for June coming to the forefront. The Aussie could be moved by RBA interest rate decision on Tuesday, yet before that, Chinese data could also influence its direction, as well as Australia’s retail sales growth rate on Thursday. Besides the FX market, one must note that also the OPEC+ group is to have a meeting in Vienna. Should the US-Sino relationships improve, we could see the group and its allies maintaining current oil production levels, while if the relationships of the two countries deteriorate, we could see the group extending production cuts, as Chinese (and not only Chinese, if I may add) demand for the commodity may be reduced.

USD – G20 and US employment report in focus

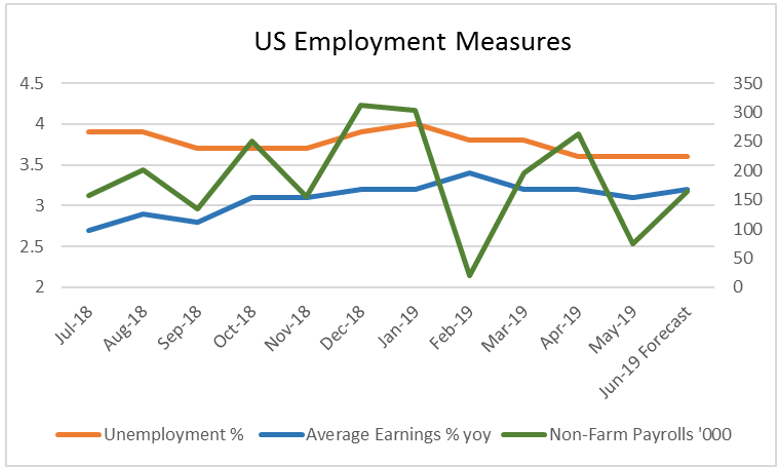

As the markets open early in Monday morning, the first repercussions of the G20 summit and especially the Trump-Xi meeting will start becoming obvious. The outcome of the Trump-Xi meeting is more far fetching than the obvious effects on the US-Sino trade relationships. Analysts tend to underscore that the Fed’s current dovishness could be moderated and the market’s bearish expectations about the USD curtailed, should there be a positive outcome of the meeting. The basic scenario at the current stage is for the two leaders to agree on a ceasefire, as they did in the Buenos Aires G20 meeting last year. Yet, the possible scenarios vary from further deterioration of the US-Sino relationships as a down side risk, up to announcing specifics of a possible deal on the upside. However, it is not only the Trump-Xi meeting that could alter the Fed’s dovishness, also the US employment report for the last month of Q2 (midyear) will be of interest for the bank, which carries a dual mandate (inflation and employment). Currently forecasts include a rebound for the Non-Farm Payroll (NFP) figure after the shock drop in May’s report to 75k. At the same time, the unemployment rate is expected to remain unchanged at the lowest level for decades now, at 3.6%, definitely below the threshold of full employment. Should also the average hourly earnings grow at a decent rate, we could be seeing another picture of a tight US labour market, which provides the Fed with a small cushion for the employment part of its mandate and could provide some support for the USD. As for other financial releases, we expect the ISM manufacturing and non-manufacturing PMI figures both for June, on Monday and Wednesday to gather interest. Both are forecasted currently to drop, and should that be the case, we could see the USD slipping as the drops could imply a weakening of economic activity in both sectors of the US economy.

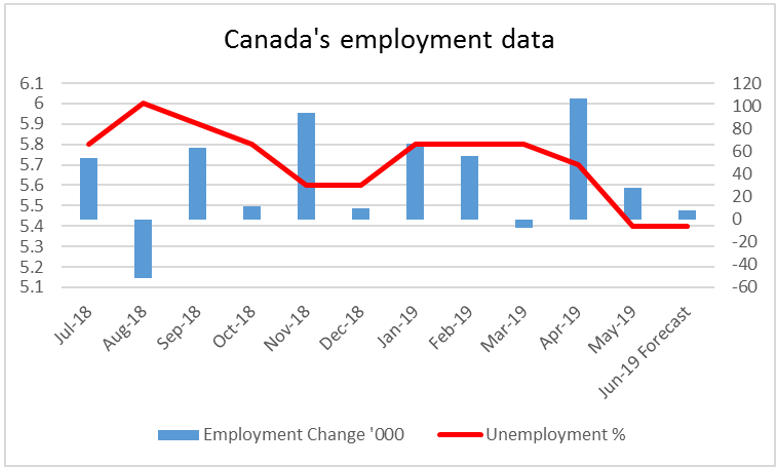

North of the US border the Loonie, is expected to be influenced by the release of Canada’s employment data for June, on Friday. Currently the employment change figure is expected to drop reaching +8k, if compared to May’s reading of +27.7k, while the unemployment rate is expected to remain unchanged at 5.4%. Despite the unemployment remaining at rather low levels for Canadian standards, the picture of a rather tight Canadian labour market could be blurred, should the employment change figure drop as forecasted, causing the Loonie to slip. Furthermore, the Ivey PMI for June, released a bit later on Friday, is forecasted to tick down reaching 55.8, if compared to May’s reading of 55.9. Albeit the retreat expected, being quite small, if seen in conjunction with the labour data, could cause the Loonie also to slip, albeit it remains at rather satisfactory levels. Prior to that, on Wednesday, we get the trade balance figure for May. The figure is forecasted to be a widened deficit of -2.8 billion currently, if compared to April’s reading of -0.97B and could be predisposing bearishly the CAD. It should be noted, that the Loonie has had a nice run last week, especially against the USD, also pushed by the rise in oil prices. We expect the commodity currency to remain closely linked to the oil market in the coming week, hence any fluctuations in oil prices, even if influenced by the OPEC+ group, could also influence the CAD.

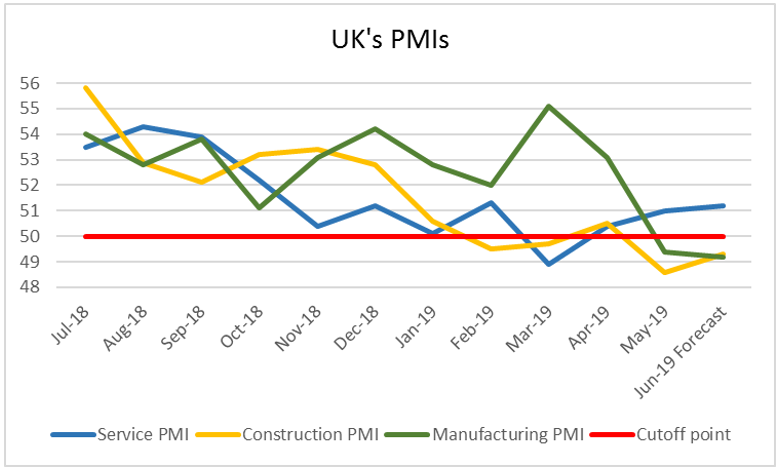

With the race for Theresa May’s replacement, being center stage for UK politics, understandably it is creating a lot of headlines and until now is keeping the pound under pressure. There seems to be some uncertainty if Boris Johnson, which seems to be gathering most odds of becoming UK’s next PM, would be willing to let the UK crash out of the EU without a deal. Jeremy Hunt on the other hand seems to be placing more weight on an orderly Brexit, yet is still expected to come in second. The UK Parliament looks quite uncertain if it may be able and/or willing to try blocking a no deal exit and the opposition looks weak. It would be indicative of the situation that Boris Johnson refused to rule out suspending Parliament in order to force a no-deal Brexit. The EU has stated that it will not accept any renegotiations of the deal and time limits seem to be tight, if not too tight (given the summer recess) for any meaningful renegotiation. Media report of possible food shortages and at the same time, that stocking of stores may be fuelling the UK economy. On the financial releases front, June’s PMIs are due out for the UK in the coming week and could move the pound. Currently the heavy weight Services PMI is expected to rise showing some increase in economic activity. However, it should be noted that the manufacturing PMI as well as the construction PMI are expected to remain below the reading of 50.0, which could be used as a cut-off point, between expansion and contraction. We could see the GBP remaining under pressure, yet the financial releases could provide some volatility, especially given the release of UK’s final GDP rate for Q1, which despite remaining unchanged (if compared to the preliminary release), still gave cable a lift of 22 pips at the time of the release.

Moving on the other side of the world, in Australia RBA is to release its interest rate decision late in the Asian session on Tuesday. RBA had cut rates in its last meeting (June) by 25 basis points (bp) reaching +1.25% and is expected to cut rates again next week by 25 bp, lowering them to +1.00%. Currently AUD OIS imply a probability of 79.45% for such a scenario and most analysts seem to concur with such a move. It would be indicative that RBA governor Lowe last week had stated that it is not unrealistic to expect a further cut in the cash rate and was very hopeful that it will not need to cut as far as some central banks in Europe. It should be noted that the market seems to be predisposing itself for a further rate cut in November, yet probabilities currently are against it currently. Should the accompanying statement show extensive dovishness, such that may indirectly imply a further cut, we could see the AUD tumbling. Please bear in mind that RBA could also be influenced by the outcome of the G20 meeting. Should there be an improvement of the US-Sion relationships, we could see the bank moderating any possible dovishness and the Aussie could strengthen. If the bank in new light decides to remain on hold, maintaining a wait and see position, we would expect the Aussie to strengthen substantially. As for financial releases, we expect Aussie traders to keep a close eye on China’s NBS and Caixin manufacturing PMI’s for June, due out on Sunday (the 30th of June) and Monday respectively. Should there be a substantial slowdown or contraction of economic activity indicated, we could see the Aussie weakening ahead of the RBA interest rate decision. On the flip side, some comfort could be provided for the AUD, from the release of Australia’s retail sales growth rate for May, on Thursday. The rate is expected to accelerate, get out of the negative area and show growth once again on a month on month basis.

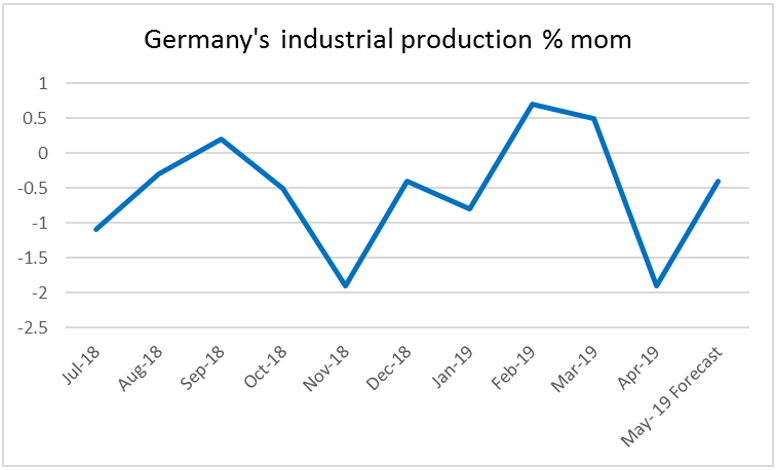

The G20 meeting could also provide some developments regarding the US intentions for tariffs on the European cars. The issue is to be discussed and should there be any negative developments, or any indicationjs that the US may go ahead with such tariffs, we could se the common currency weakening. In a more indirect way, the EUR could benefit from a possible improvement of the US-Sino relationships an vice versa, as the Eurozone has a substantial exposure to China. Also we maintain our worries about the US president’s comments for the “cheap” euro and the ECB’s stimulus. It should be noted that the prospect of a possible stimulus for the EUR, from the ECB, still seems to be weighing, to a greater or lesser extent, on the single currency. Apart from the political and monetary fundamentals, second tier financial releases could also be influencing the EUR’s direction next week. Eurozone’s final PMIs for June are due next week, yet are expceted to show no change since the preliminary release and should that be the case, we could see little reaction from the market. Traders are also expected to be monitoring Germany’s employment data for June and Eurozone’s for May on Monday, Eurozone’s PPI rate for May and Germany’s retail sales for May on Tuesday, however the highlights could be Germany’s industrial production growth rate for May, as well as Germany’s factory orders for May.