Week Ahead | 26/04/2019

Weekly outlook: April 29th to May 3rd | FOMC, BoE and US employment report to dominate the headlines.

We expect a blend of political events and financial releases to move the markets next week. Especially on the financial releases side, there are plenty of releases in contrast to the week before and some of high importance. US releases which are expected to be under the spotlight are definitely the FOMC interest rate late on Wednesday and the US employment report for April on Friday. In the UK, BoE’s interest rate decision is expected to keep GBP traders busy along with the release of April’s PMIs, especially the service sector PMI. In next week’s fundamentals, we expect the US-Sino negotiations to provide volatility once again as they restart on the 30th of April. Also any repercussions of the US-Japanese talks this week especially the meeting between Abe and Trump, albeit the effect may have weakened over the weekend. Across the Atlantic, despite no withdrawal bill being on UK Parliament’s agenda next week, we expect Brexit to hit the news once again. On the flip side it’s all quiet in the land of the rising sun as Japan, will be entering a prolonged period of holidays, yet at the same time please be advised that there may be thin trading risks involved. Analysts are pointing out, that the total of the coming week could entail the prementioned risk and single out May 1st as a particularly high risk date. We would also like to add Monday 29th of April, though.

USD – FOMC and US employment report to provide waves of volatility

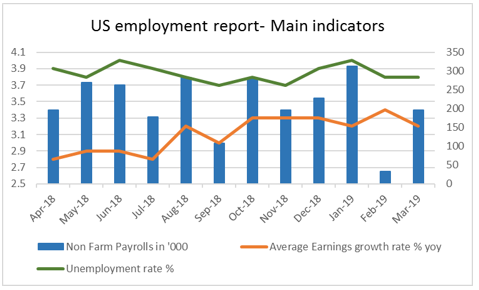

With the Japanese mounting pressure for a speedy resolution of the US-Japanese negotiations, the Trump-Abe meeting is of the essence and its repercussions could provide some volatility for the USD and the JPY, albeit weakened over the weekend. On the other hand there is no dilution available for the effect of the US-Sino negotiations, which are to begin their next round of talks next week (30th of April) in Beijing. Despite US President Trump reassuring that the negotiations are going well, a lot of promises were made in the past and the negotiations have yet to deliver results. Despite there being a lot of headlines about a quick resolution and a possible deal, which could be signed near the end of May by US president Trump and Chinese president Xi, we maintain some reservations. Never the less the negotiations are expected to cover trade issues including intellectual property, forced technology transfer, non-tariff barriers, agriculture, services, purchases and enforcement any deal agreed. Should there be good news coming out, especially something more concrete, we could see volatility rising for the USD but for other currencies like the Aussie and the Kiwi as well. On the financial releases front the release of FOMC’s interest rate decision is expected to be in the spotlight on Wednesday. The bank is widely expected to remain on hold at +2½ % and feds funds futures (FFF) seem to support the idea, as they imply a probability of 99.5% for such a scenario. The bank could be in a wait and see position, especially about the outcome of the US-Sino negotiations, in order to have better clues about the outlook of the US economy. Comments from fed Chair Powell for a “patient” stance could be expected, in his press conference later on. On the flip side, should the bank sound dovish once again we could see the USD weakening, especially as it seems to pursuit its +2.00% yoy inflation target and should the US GDP rate slowdown today. On Friday, the headlights of the markets are expected to be on the release of the US Employment report and especially the NFP figure. We expect the report to show another picture of a rather tight US labour market, removing a possible headache for the Fed. Should that be the case, we could see the USD getting some support, especially if there are any upside surprises regarding the average earnings growth rate. However there also other financial releases from the US which could be of interest. On Monday Fed’s favorite inflation measure the Core PCE price index for February is due out, along with personal consumption. On Tuesday the CB consumer confidence indicator for April is to be released and on Wednesday, we get the ISM manufacturing PMI for April. On Thursday we get the US factory orders growth rate, while on Friday, after the US employment report is out, we get the ISM non- manufacturing PMI also for April ending a rich series of data releases relating to the USD.

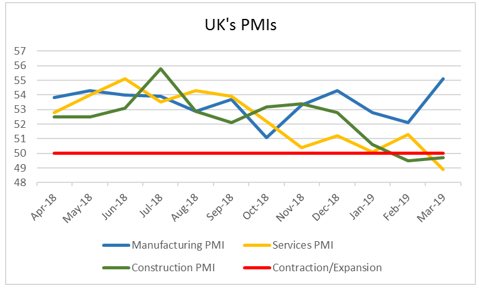

As the new week enters, we could see financial releases affecting the pound and especially BoE’s interest rate decision. The bank is widely expected to remain on hold at +0.75% once again as Brexit uncertainty currently clouds UK’s economic outlook. Currently GBP OIS seem to support this scenario as they imply a probability of 99.01% for the bank to keep rates unchanged. Another element which could provide more interest would be the release of the bank’s inflation report and especially the projections which it includes. The projections could shed further light as to what the expectations of the bank are, especially given the possibly negative effect of the ongoing Brexit uncertainty on the UK economy until now. Also, in the following press conference, BoE governor Mark Carney could make some further warnings for the same issue. However it’s not only BoE’s interest rate decision in the financial releases horizon for the pound, this week. April’s PMIs are due out and could have a substantial effect on the sterling. We tend to concentrate on the Services PMI as it describes the course of economic activity in the largest sector of the UK economy and had suffered a substantial blow in its release for March, showing a contraction. Never the less, PMI’s for the manufacturing and the construction sector, will be completing the picture. Despite the UK parliament not having in its agenda a Brexit withdrawal bill for the coming week, developments on the issue are ongoing in the inner UK political scene. Choices for Theresa May seem to be getting harder, as negotiations with the Labour party have been reaching critical levels and UK’s PM seems to be running low on leverage. Also in the intra-Tory front, hard Brexiteers are mounting pressure for Theresa May and even a roadmap for her resignation was requested, by Tory MPs. Also, Theresa May tries to avoid UK participation in the EU Parliamentary elections, however chances for such a scenario seem to be running low at the current stage and the Tories could be in for a loss. Unless the negotiations with the Labour party start bearing fruit, we do not expect positive headlines for Brexit the coming week, in which case the pound could weaken even further.

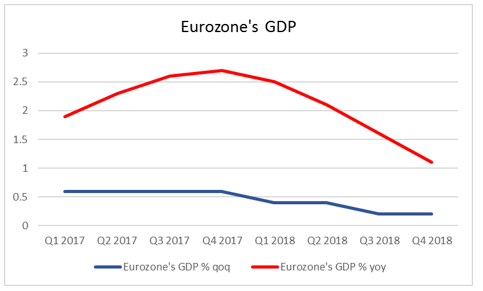

After a bearish week, a substantial number of financial releases could rock the common currency. We tend to focus, primarily on Eurozone’s GPD release on Tuesday and a series of inflation rates affecting the Eurozone, scattered through the week, peaking on Friday with Eurozone’s preliminary CPI rate for April due out. First things first, Eurozone’s biggest worry, growth could be in the epicenter of attention, for EUR traders this week as the preliminary GDP growth rate for Q1 is due out on Tuesday. The rate is near stalling on a quarter on quarter (qoq) level and the area’s recent releases (PMI’s, industrial output) weren’t exactly foreshadowing better days, probably the opposite. Should the GDP rate show any signs of further deceleration, God forbid stalling or recession, the common currency could be in deep waters and some eyebrows maybe raised about ECB’s opinion of growth returning in the second half of the year. The release of April’s flash HICP rates for the area on Friday, along with Germany and France on Tuesday will also be playing a major role for the common currency’s direction. Should there be any further slowdown of the rates, we could see arguments for further easing of ECB’s monetary policy strengthening. On second base there are also other financial releases which are to provide a better picture of the Eurozone’s economic state. Starting with Monday, Eurozone’s industrial sentiment for April, seems to be standing out among a number of financial releases. While on Tuesday we get Germany’s and Eurozone’s employment data for April and March respectively, along with Germany’s GfK consumer climate for May.

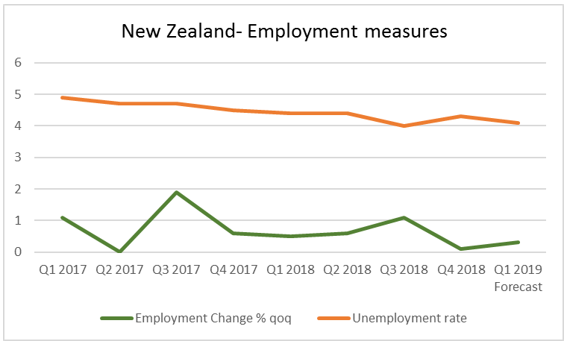

With Chinese data improving and showing some sort of stabilisation, the PMI releases next week are to show whether the Chinese have actually bottomed out or not. Given the wide exposure of the Australian economy to China, we could expect Aussie traders to keep a watchfull eye over the releases, especially after the Aussie’s weak performance in the current week and the slowdown of Australia’s inflation rate. Starting with NBS manufacturing PMI for April on Tuesday, the indicator’s reading is expected to remain unchanged currently at 50.5, if compare to March. Should the reading remain unchanged, it would imply growth for a second consecutive month, however on the other hand it may not be sufficient to convince trader’s about the prospects of China’s manufacturing sector, as the reading fails to put more distance from the cut off point of 50.0. The situation seems to improve somewhat on Thursday as the Caixin manufacturing PMI for April is expected to rise slightlty. Kiwi traders will also be looking at the Chinese data, for some relief, as the NZD also had a weak performance lately. However, with the RBNZ having a dual mandate (inflation and employment) and seeming ready to cut rates, New Zealand’s employment data release for Q1, becomes of the essence for Kiwi traders. The unemployment rate is forecasted to drop reaching 4.1%, if compared to prior quarter’s reading of 4.3%, while at the same time the employment change rate for the same period is forecasted to accelerate and reach 0.3% qoq, if compared to prior quarter’s reading of +0.1% qoq. Should the actual rates meet their respective forecasts, we could see the NZD getting stronger, as the ywould be indicative of a tight labor market and could lessen the chances of a rate cut by the RBNZ, or at least postpone it further done the road.