Week Ahead | 24/05/2019

Weekly outlook: May 27th to 31st | EU Parliament Elections, Brexit and BoC interest rate decision in focus

EU Parliament election results are to be announced on Sunday night and could rattle the EUR on Monday. Also the UK is expected to have some political developments as Theresa May has announced that she will be leaving her office on June 7th. The US is still in a bitter feud with the Chinese and the saga is expected to continue to rock the markets. North of the US border, Canada’s central bank will be having a policy meeting and currently is expected to remain on hold. As for financial releases we single out Germany’s and France’s preliminary CPI rates for May, as well as China’s NBS Manufacturing PMI for May and the second release of the US GDP growth rate, among a number of financial data, which could be taking a back seat this week.

EUR – EU Parliament elections and preliminary CPI rates could provide direction

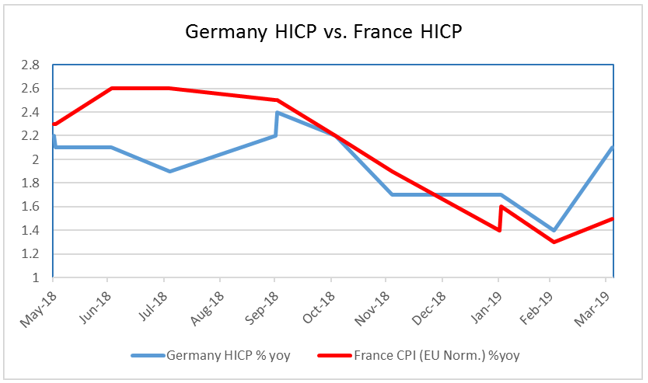

Despite ballots already closing, the EU Parliament elections result is expected to be announced on Sunday evening and affect the common currency on Monday. Various scenarios could be played out, depending on the outcome. Should populists rise substantially we could see them trying to ease Eurozone budget rules, especially given that Italy’s government has signalled such intentions. Overall, the importance for the EUR relies practically on the possible instability the election result could provoke in a number of countries, such as Italy, Germany, the UK and France. Also there depending on the new balance of power which will be formed there could be a shifting of the EU policies or even of the agenda, while efforts for further unification of the old continent, at least at finance level, could fall apart. On the financial releases front, we expect the release of France’s and Germany’s preliminary HICP rates for May on Wednesday and Friday respectively, to provide direction for the common currency. Both rates are expected to slow-down currently and should that be the case we could see the common currency weakening as such results could foreshadow also a slowing down of Eurozone’s inflation rate. Also it should be noted a possible slowdown of the prementioned inflation rates could dim expectations for a rebound in the second half for the area. On second base EUR traders are expected to keep an eye out for Monday’s release of Germany’s Gfk Consumer Sentiment for June, Eurozone’s Industrial sentiment and business climate indicators both for May. Other points of interest for EUR traders are expected to be Germany’s unemployment data for May and Germany’s retail sales on Wednesday and Friday respectively.

No major financial releases are to be expected this week for the pound and actually Monday is to be a bank holiday for the UK. The pound was Brexit driven for over a year now and given Theresa May’s resignation for the 7th of June we could see political developments regarding the future state of UK politics along with May’s replacement moving the pound. We could see the resignation have a detrimental effect on the GBP as the possible successor from the Tory party is expected to be more of a hardliner regarding Brexit, hence increasing the odds for a hard Brexit. Currently there is speculation about Boris Johnson being a possible replacement for Theresa May. The possibility of a second referendum exists, as well as the possibility of general elections yet at the current stage seems remote to start materializing in the next week, yet should there be any indications implying such a scenario, they could support the pound. It should be noted that the UK Parliament is entering a recess that is expected to last through the next week and more or less is expected to moderate the impact of Brexit on the GBP somewhat. Also the results of the EU Parliament elections could have a substantial effect on the UK political scene. Nigel Farage with his Brexit party is expected to fare well, while the Tories are expected to lose substantially, with some polls showing them dropping to fourth place, while Labour is expected to retain the second position. Definitely such results are expected to mount pressure on the Tory party, probably toughening the stance of hard Brexiteers. On the flip side should the Labour party win the elections we could see mixed feelings of even some support for the pound.

USD- The greenback still in the US-Sino trade war hurricane

The USD is expected to continue to be affected by the US-Sino trade war and not be able to escape any further developments. Any possible headlines about applying tariffs on the total of the Chinese imports could affect the USD as well as any indications of easing of tensions. Never the less the Fed’s intentions moved the USD in the past week and especially as expectations about a possible rate cut rose on Thursday and weakened the USD. We could see argumentation about the issue continue to affect the USD’s direction and it should be noted that Fed officials were quite adamant about the Fed’s current policy being the appropriate for the US economy at the current stage. Despite the US calendar starting with a holiday on Monday (Memorial day) and being rather light, we would like to draw trader’s attention to three US financial releases this week. The main is expected to be the GDP growth rate second estimate for Q1 on Friday, which if accelerates could provide some support for the USD. The second would be on Friday, the US consumption and core PCE prices for April, which if they slowdown as forecasted could weaken the USD, but their main point of interest is if they are going to cause any alterations in Fed official’s tone about the Fed’s policy. Last but least on Tuesday we get the US consumer confidence, which is expected to rise and if so could support the USD.

CAD – BoC interest rate decision and oil market to move the Loonie

North of the US border, on Wednesday Canada’s BoC is expected to release its interest rate decision on Wednesday. The bank is widely expected to remain on hold and at the current stage CAD OIS imply a probability for the bank to do so of 98.71%. Given that the bank has relented its hawkish bias in the last statement, the recent uncertainty in global trade and the recent drop of oil prices, we wouldn’t expect any substantial hawkish comments. We could see the bank remain in a wait and see position in order for the fog to clear and the bank being able to reach decisions on more sound data. Yet at the same time it should be noticed that the recent acceleration of the retail sales could be a ray of hope for the bank. As for financial releases, Canada’s GDP for Q1 is due out on Friday and should it accelerate could provide some substantial support for the CAD. Also the Loonie traders will be keeping an eye out for any developments in the oil market. Should oil prices start dropping again on the back of the possible detrimental effects of the US-Sino trade war or the slack in the US oil market, we could see CAD weakening, while if there are any production cuts implied by OPEC members, especially Saudi Arabia, we could see the Loonie getting some support.

JPY- Safe haven flows and industrial production to be eyed by traders

The yen was moved primaruly by safe haven flows the past week and USD weakeness and we could see it continue to form its price action agianst a nuber of other currencies sing the same pattern. Despite the low impact of financial releases, there are some which cannot be omitted. Startting with Monday during the asian session, BoJ Gocvernor Kuroda will be speaking and we could expect some comments for Japan’s hot topic right now, the new sales tax. Abe’s government is maintain ing the view that the country should go ahead nad implement the hike of the sales tax, while other voices strongly oppose it, fearing that it could lead to recession, or even slowdown inflation, as consumption may be threatened. On the finacial releases front, on Friday, we get tJapan’s unemployment rate and thde preliminary industrial production growth rate, both for April. Both seemto be poised to supoprt he JPY, yet given the low impact of Japanese financia lreleases last week on the Yen, we could see them bein of low key.