Week Ahead | 22/06/2018

June 25th to 30th | Market focus on RBNZ’s interest rate decision

Next week’s market movers

• On Monday, we get Germany’s ifo Business Climate indicator for June.

• On Tuesday, the US Consumer Confidence indicator for June.

• On Wednesday, the US Durable Goods growth rates are due out.

• On Thursday, the RBNZ interest rate decision could be the center of discussions bit we also get the preliminary release of Germany’s HICP rate for June and the final US GDP growth rate for Q1.

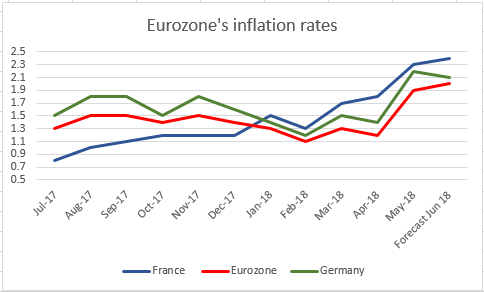

• On Friday, we’ll have a busy day as we get Japan’s unemployment rate for May, France’s and Eurozone’s preliminary inflation data for June, Germany’s unemployment data for June, UK’s final GDP growth rate for Q1 and in the American session we get the US consumption rate for May, Canada’s GDP growth rate for April and the US university of Michigan final Consumer Confidence figure for June.

• On Saturday, investors may be working overtime as China’s NBS Manufacturing PMI for June is due out.

In the next week a plethora of financial data releases could attract the market’s attention. Our team handpicked the ones which it considers as the most influential and discusses their possible forecasts and their respective effects on various currencies.

On Monday, during the European session Germany’s ifo Business Climate indicator for June will be released. The indicator is forecasted to drop, reaching as low as 101.8 compared to previous reading of 102.2.

Should the actual figure meet the forecast we could see the EUR weakening as the drop of the indicator would be indicative of the pessimistic views regarding the business climate of the largest economy in the Eurozone for the next six months. The rather low reading is a continuation of the past two readings (April and May) and worries may grow as the Business Climate does not seem to be able to rise back up.

On Tuesday, in the American session, the US CB Consumer Confidence indicator for June is due out. The indicator is forecasted to tick up to 128.1 compared to previous reading of 128.0.

The uptick could provide some support for the USD as the reading is already at rather high levels and the uptick could underscore the high confidence of the average consumer to the US economy.

On Wednesday, during the American session the US durable goods orders growth rates will be released. The durable goods orders (excluding transport) growth rate is forecasted to decelerate, reaching as low as +0.4% mom compared to previous reading of +0.9% mom, while the headline durable goods growth rate is forecasted to accelerate reaching -0.9% mom compared to previous reading of -1.6% mom.

Should the actual rates meet the forecast we could see the market getting mixed signals. Despite that slowing down of the decrease in the headline rate, the overall picture is negative as the headline rate remains in the negatives and the core rate is slowing down. The USD could weaken on such a release.

On Thursday, early in the Asian session we get RBNZ’s interest rate decision. The bank is widely expected to remain on hold at +1.75% and currently NZD OIS imply a probability for the bank to remain on hold at 99.40%. Having said that, it should be noted that RBNZ has a dual mandate over inflation as well as unemployment. The last reading of the headline CPI rate is at +1.1% yoy which could be characterized as rather low compared to the bank’s target of +2.00%±1.00%. Despite the inflation rate being within the bank’s target range the fact that it currently is near it’s lower boundary could hold back the bank for any possible rate hike in the near future. All the above arguments could be strengthened by the fact that RBNZ governor had stated that he would like to see the core CPI rise before any rate hike and that since then there weren’t any updates regarding inflation. On the other hand the unemployment rate is at rather low levels considering the last reading of 4.4%, something which could give the bank some breathing space. Overall we currently see the case for the bank to reiterate the status quo by keeping a more neutral tone and if not maybe have a slightly dovish tone, given recent slight weakening of the financial data.

In the American session we get the US final GDP growth rate for Q1. The rate is forecasted to remain unchanged at +2.2% qoq compared to the preliminary release. Should the rate remain at +2.2% qoq we could see the USD weakening as the rate is rather low. On the other hand we may have a market which may be expecting the reading as it is the final version, as well as a future acceleration in the next quarter, hence market reaction may be rather muted.

On Friday, during the Asian morning, Japan’s unemployment rate is due out for May. The rate is forecasted to remain unchanged at 2.5% compared to previous reading. Should the actual reading meet the forecast we could see the Yen strengthening. Be advised that Japan is rather used to such low unemployment rates hence the market’s reaction may be muted.

Later in the European morning, we get the preliminary release of France’s CPI (EU Norm.) rate for June. The rate is forecasted to tick up reaching +2.4% yoy compared to previous reading of +2.3% yoy. Should the actual rate meet the forecast we could see the common currency getting some support as such a rate could indirectly support the argument for a slight acceleration in Eurozone’s CPI rate later on.

Later in the European session Germany’s unemployment data for June are to be released. The unemployment rate is forecasted to remain unchanged at 5.2%, while the unemployment change is forecasted to narrow to -8k compared to previous reading of -11k. Should the forecasts be realized we could see the EUR slipping as despite the unemployment rate remaining unchanged, the narrowing of the unemployment change deficit is not positive news.

Also in the European session we get the final release of UK’s GDP growth rate for Q1. The rate is forecasted to remain unchanged at +0.1% qoq compared to the preliminary reading. The static GDP growth rate should not be good news for the pound especially at so low levels despite BoE considering it as of a rather temporary nature.

Last in the European session, Eurozone’s preliminary CPI rate for June is due out. The rate is forecasted to tick up to +2.0% yoy compared to previous reading +1.9% yoy. Should the actual reading meet the forecast we could see some smiling faces in Frankfurt as the rate hits its target after more than a year. The common currency could get some support from such readings.

In the American session we get the US Consumption growth rate for May. The rate is forecasted to slow down to +0.4% mom compared to previous reading of +0.6% mom. If the reading actually slows down we could see the USD slipping as a slowdown to the value of all spending by consumers could imply a decrease of the consumer’s willingness and ability to spend in the economy.

At the same time we get from Canada, the GDP growth rate for April. The rate’s last reading was of +0.3% mom. Any reading higher than +0.3% mom could provide some support for the Loonie especially ahead of the BoC meeting on the 11th of July.

Later on, in the American session, the final US University of Michigan Consumer Sentiment indicator for June is due out. The figure is forecasted to drop to 99.0 compared to previous preliminary reading of 99.3. Should the actual reading meet the forecast we could see the USD weakening as the indicator’s reading drop implies a more pessimistic view on behalf of the consumer than was implied in the preliminary reading. However the opposite effect could take place considering that previous month’s reading was at lower level.

On Saturday, during the Asian morning we get China’s NBS Manufacturing PMI for June. The figure is forecasted to drop to 51.6 compared to previous reading of 51.9.

Should the actual reading meet the forecast we could see the Kiwi and the Aussie slipping on Monday as their respective economies have great exposures to China and such a drop could imply less exports to China.