Week Ahead | 01/04/2019

Weekly outlook: March 18th to 22nd | Brexit and FOMC interest rate decision front and center

Entering the new week in the fundamentals, we expect Brexit to be one of the main fundamental issues for the week, once again. It should be noted though that the GBP could also be influenced by a number of financial releases along with BoE’s interest rate decision. For the USD the main event could prove to be FOMC’s interest rate decision and any possible developments in the US-Sino trade war. FOMC and BoE won’t be the only ones releasing their interest rate decisions this week though. The Swiss SNB and Norway’s Norgesbank could also provide for fluctuation for their respective currencies. On the other hand, during this week EUR traders will probably be waiting for the release of the preliminary PMI’s of March on Friday, however the release of Germany’s ZEW indicators could also provide some volatility. It should be noted that a number of other economies also find themselves at crossroads as CPI rates and employment data are to be released.

USD – FOMC interest rate decision to be the main event.

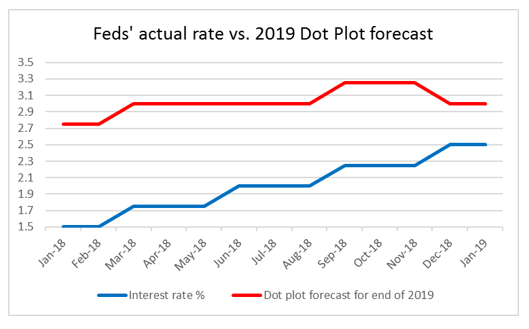

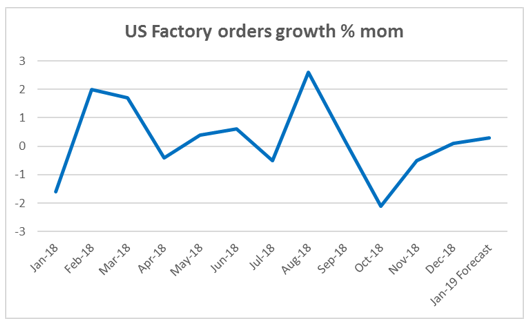

The FOMC interest rate decision is expected to be the main event for the USD this week. The bank is widely expected to remain on hold at +2.5% and currently Feds Funds Futures imply a probability of 99.0% for such a scenario, rendering the rate level part of the decision as an open and shut case. However there’s been lots of water under the bridge, since December when the bank released its dot plot and economic projections. Don’t forget that the bank’s last dot plot had implied two more rate hikes in 2019 and the big question is if FOMC members are to curtail expectations and if so by how much. The market seems to be suspicious of a possible rate cut by year’s end, however we do not share such a scenario, at least not yet. Should the dot plot show that policymakers are consdering that even one rate hike is necessitated for the US economy until the year’s end, that could prove quite bullish for the USD. Other than that, we expect that communication is to have a dovish tone as it had in the past meeting advising patience once again possibly and should the economic forecasts intensify arguments for a possible slowdown we could see the USD weakening. Please be advised that Jerome Powells following press conference could extent volatility for USD pairs. As a second fundamental issue, we maintain our worries about future developments in the US-Sino negotiations as a number of comments coming from both Beijing and Washington, seem to point towards uncertainty as the Trump-Xi meeting could be postponed substantially. Should there be negative developments on the issue over the week, we could see the USD’s role as a safe haven being highlighted once again and the greenback could have some gains. On the financial releases front, on Tuesday the USD could get some support as the factory orders growth rate for January is forecasted to accelerate (Forecast: +0.3% mom vs. Prior: +0.1% mom). The same applies for Thursday, as the Philly Fed Mfg Index for March is expected to rise substantially and get out of the negative area (Forecast: 5.0 vs. -4.1).

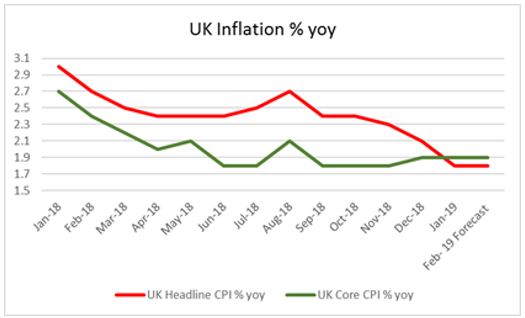

Brexit seems to be in the front row this week for the pound, as the UK parliament is to vote on Theresa May’s deal for a third time. Our base scenario currently remains for Theresa May’s deal to be rejected once again as nothing has changed, however UK’s Prime Minister is intensifying her efforts and building up pressure, by warning that a possible extension could be a long one. The critical part of the issue is expected to be once again whether Theresa May will be able to bring hard Brexiteers (especially the DUP) over to her side. Should the deal be approved despite our expectations, we could see the pound rallying, as the UK would be exiting the EU in an orderly fashion. On the other hand should the UK Parliament once again reject the deal, we could see the pound weakening, yet the market may be turning its attention to Thursday’s EU summit for more clarity on the issue. Should the EU provide a long extension of the Brexit date we could see the pound getting a small shock but over the longer run it could provide for some support for the GBP as alternative scenarios may start resurfacing. However on the financial releases front BoE’s interest rate decision should be the main event for the pound. The bank is widely expected to remain on hold at +0.75% and currently GBP OIS imply a probability of 99.37% for such a scenario. We expect a vote of 0-0-9 for the bank to remain on hold, and in face of the wider Brexit uncertainty to maintain a dovish wait and see tone. In general, we do not expect there to be much deviation from the last meeting’s communique, yet should there be, we could see it weighing more on the dovish side. Also there are a number of important financial releases which could catch the eye of pound traders. Starting with Tuesday, UK’s employment data for January may weaken the pound as the employment change figure is expected to drop (Forecast: 120k vs. Prior: 167k) as well as the average earnings growth rate (Forecast: +3.2% yoy vs. Prior: +3.4% yoy), while on the other hand the unemployment rate is expected to remain unchanged (Forecast: 4.0% vs. Prior: 4.0%). On Wednesday the pound may be getting some support as both the headline inflation rate (Forecast:+1.8%yoy vs. Prior:+1.8% yoy) as well as the core rate (Forecast:+1.9% yoy vs. Prior:+1.9% yoy) are forecasted to remain unchanged for February. On the contrary a possible slowdown of the retail sales growth rate (Forecast: -0.3% mom vs. Prior: +1.0% mom) for February could weaken the GBP, just ahead of BoE’s interest rate decision.

There are a number of financial releases due out this week from Japan, yet we tend to concentrate mainly of the release of February’s inflation rates. The headline rate’s last reading for January was one step before deflation at +0.2% yoy, while the core rate is expected to remain unchanged at +0.8% yoy for February, if compared to prior month’s reading. Should the actual headline rate decelerate even more, we could see the JPY weakening substantially, as the rate’s possible deceleration would be rendering BoJ’s ultra loose monetary policy and efforts to accelerate inflation as of little use. Never the less, it should be noted once again that the JPY could be affected once again from safe haven flows, especially should there be any further negative developments with North Korea (as last week) or the US-Sino relationships.

EUR- Light Calendar with preliminary PMI’s eyed.

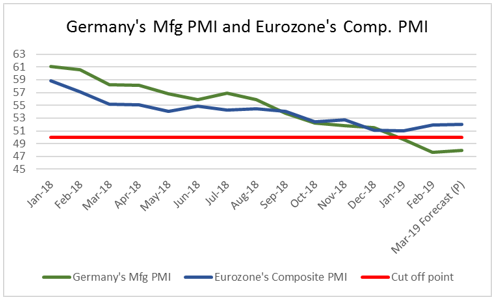

The common currency traders seem to have a rather light schedule this week. The main releases could be Germany’s ZEW economic sentiment for March and the release of the preliminary PMI’s for March. Starting on Tuesday, Germany’s ZEW economic sentiment for March (Forecast: -11.0 vs. Prior:-13.4) could reveal a less pessimistic view for the next six months of the German economy. The main focus of the market though, is expected to be placed on the release of March’s preliminary PMI’s on Friday. We tend to concentrate on Germany’s preliminary manufacturing PMI (Forecast: 48.1 vs. Prior: 47.6) and Eurozone’s preliminary composite PMI (Forecast: 48.1 vs. Prior: 47.6). Both indicators show some progress, however the overall forecasted releases may not actually convince investors that a turnaround and better days are in the cards for the Eurozone yet.

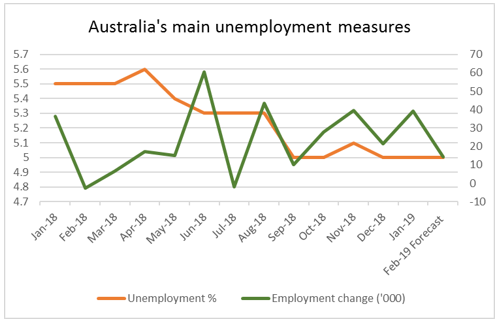

The Aussie will be having a bumpy ride at the beginning of the week, as on Tuesday RBA’s minutes of its last meeting are due out. The minutes are expected to shed more light as of the bank’s intentions and could trigger a more dovish stance for the bank, especially as the latest meeting was followed by a slowdown of the Australian GDP growth rate. We will be also focusing on any details concerning the obsticles for the bank to cut rates, as well as the boards view on the financial data. The minutes are to be followed on Thursday by the release of Australia’s employment data for February. As the employment change figure (Forecast: 14.5k vs. Prior: 39.1k) is expected to drop substantially and the unemployment rate to remain unchanged (Forecast: 5.0% vs. Prior: 5.0%), we could see the Aussie weakening especially should there be a dovish tone in the minutes on Tuesday.

Starting with Norway, Norges Bank is to release its interest rate decision on Thursday during the European session and is expected to hike interest rates by 25 basis points, from current +0.75% to +1.00%. Backed by past forward guidance and strong financials, market participants seem to have little doubt as to whether the bank will have any second thoughts on hiking as described above and always in a “gradual” approach. Should the bank also have a rather hawkish accompanying statement, possibly foreshadowing a second rate hike in 2019, we could see the NOK getting substantial support. On the downside increased rate diffrentials (especially with the ECB), the possiblity of a hard Brexit and a possible global economic slowdown could be among the main risk factors associated with the bank. The same day, Switzerland’s SNB is also expected to announce its interest rate decision and is expected to remain on hold at -0.75%. Currently CHF OIS imply a probability of 97.34% for such a scenario and market focus seems to revolve around the accompanying statement. The bank was out of the market’s radar lately, yet we do not expect for the bank to stop its expansionary monetary policy. Swiss financial releases remain rather soft, with inflation almost as low as Japan’s and growth decelerating. Should the bank keep an eye out for exchange rates and given the recent dovish outlook of the ECB (Switzerland’s main trading partner), it is difficult to see SNB keeping a hawkish outlook for the Swiss economy. We would expect the bank to maintain a dovish outlook maintaining negative rates which could weaken the CHF.

CAD – Inflation, Retail sales and the oil market in focus.

Loonie traders will have to wait until the end of the week for the release of February’s inflation rates. The headline rate (Forecast: +1.5% yoy vs. Prior: +1.4% yoy) is expected to tick up, while the core rate’s last reading was of +1.5% yoy. Should the actual headline rate tick up as forecasted and the core as well we could see the CAD getting some support. At the same day, the retail sales growth rate for January (Forecast: +0.4% mom vs. Prior: -0.1% mom) is due out. Despite the CPI rates bearing more weight, the substantial acceleration of the retail sales growth rate getting out of the negative area, could provide some support for the CAD as well. Yet as always, the CAD remains also oil driven so it would be advisable to pay close attention to the direction of oil prices, as well as any fundamental developments of the oil market.