Week Ahead | 14/01/2019

Weekly outlook: January 14th to 18th | Brexit and inflation rates to move the markets.

Entering the new week on a fundamental basis, Brexit is expected to dominate the headlines as the UK parliament is to vote on Theresa May’s Brexit plan. Across the Atlantic, the intentions of the Fed, the ongoing US government shutdown and the possibility of US president Trump declaring a state of emergency could be keeping the markets on the edge of their seat. On the financial releases front, a number of releases relating to inflationary measures could provide for further volatility.

USD – Fed’s intentions along with US Government shutdown could be maintained as main issues.

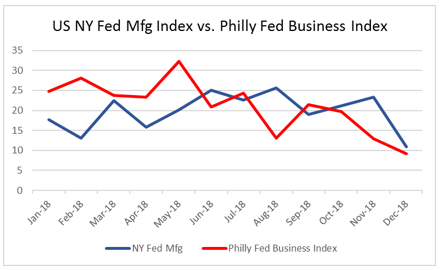

With the US government shutdown being the longest recorded, it might start affecting the markets as the US may be entering unchartered waters and uncertainty grows. The possibility of president Trump declaring a state of emergency seems to be increasing as the shutdown is prolonged, however how the markets will react remains to be seen. Also should there be further headlines about the Fed’s intentions see could see the USD entering a volatile state once again and should there be more dovish comments by Fed officials, we could see the USD weakening further. On the financial releases front for the USD, manufacturing data could be standing out as the NY Fed Manufacturing Index and the Philly Fed Index, both for January are to be released on Tuesday and Thursday respectively. Both are forecasted to note an increase of their readings and the question is if they will be able to revert the bearish sentiment of the PMI release for the past month. On the other hand the US industrial production for November is forecasted to decelerate on Friday, sending negative signals. Also of special interest will be the release of the US retail sales growth rate for December on Wednesday, which is forecasted to remain stable on a month on month basis and the preliminary University of Michigan Sentiment indicator for January which is expected to drop and could weaken the USD on Friday.

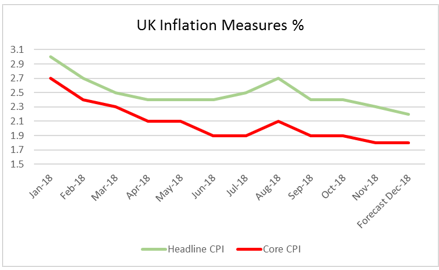

On Tuesday 15th January, the UK parliament is expected to decide on Theresa May’s Brexit plan. Currently analysts predict that the plan will most probably be rejected as no majority seems to exist to support it. Such an outcome could imply a prolonged and deepening uncertainty for the pound making even more uncertain any forecast about the final outcome of the Brexit process. With the Brexit date approaching the question remains whether the UK will be able to avoid a hard Brexit, which could have severely adverse effects on the UK pound. Voting is expected to be in the late UK afternoon, however volatility for the pound may start earlier, as headlines are expected to reel in and could influence the pound’s direction and continue after the result is announced as headlines are expected to continue to reel in. Should the deal be the Theresa May has just three days to set out a plan B, which may have the shape of an existing customs union agreement the EU already has with a third country, maybe with some added features. Also it should be noted that at the end the UK government could unilaterally ask to revoke the Brexit process or even end up crashing the UK out of the EU. The Labour party has already announced that it plans to ask for a confidence vote, in case Theresa May’s plan gets rejected. Should such a confidence vote be successful in removing Theresa May from office, a new government will have to be formed within 14 days or else there will be new general elections. On the financial releases front it should be noted that the release of the UK’s inflation rates (CPI and PPI) for December, could intensify the volatility for the pound on Wednesday, as well as UK’s retail sales growth rate on Friday.

Fundamentally the common currency may also be affected somewhat by the ongoing Brexit developments and we could see some volatility on that, during the week. On the financial releases front, we could see the EUR weakening as the final releases of the inflation rates for France, Germany and the Eurozone are due out. All readings are expected to remain unchanged if compared to their respective preliminary releases and lower than last month’s reading. Should the deceleration of the inflation rates be confirmed as forecasted, we could see the common currency weakening. Also the release of Germany’s GDP growth rate for 2018, is not expected to help the EUR on Tuesday. The German GPD growth rate is forecasted to decelerate substantially reaching +1.5% yoy, if compared to 2017’s reading of +2.2% yoy. Should the actual rate meet its forecast, we could see the EUR weakening as the rate’s slowdown, could strengthen the arguments for a general slowdown of Eurozone’s growth.

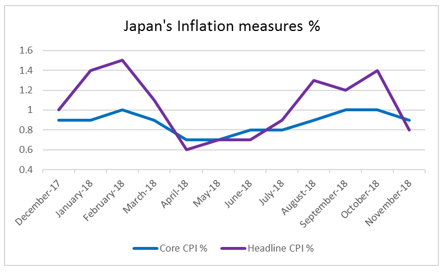

In the absence of any fundamental political uncertainty the Yen is expected to be more data driven. Starting on Wednesday, Japan’s corporate goods price growth rate for December is expected to remain in the negative area unchanged at -0.3% mom. At the same time the machinery orders growth rate for November is expected to slow down and reach +3.5% mom, if compared to prior reading of +7.6% mom. Both releases, if their respective forecasts are realized could weaken the JPY as they could imply that inflationary pressures remain in the retreat and the businesses are less willing to invest in machinery. The bearish sentiment for the Yen, could be further enhanced on Friday as the headline and core inflation rates for December are due out. The core rate is forecasted to tick down and reach +0.8% yoy, if compared to prior reading of +0.9% yoy. Should the actual rate meet its forecast and the headline rate also behave in a similar manner, we could see the Yen weakening, as the slowdowns would opposing BoJ’s efforts boost inflationary pressures.

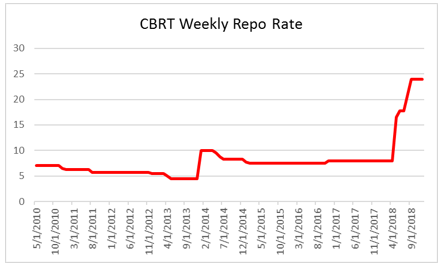

On Tuesday, we get from Turkey, CBRT’s interest rate decision. The bank is expected to remain on hold at +24.00% and analysts point out that this month in response to a slowdown in inflation. CBRT had stated that it would deliver additional monetary tightening if needed, therefore we it would be a paradox to cut rates on Wednesday’s meeting. A Reuter’s poll, seems to favor the bank remaining on hold as mentioned, as most participants seem to consider a possible rate cut by the bank as premature. However, it is election period for Turkey and pressure from current president Erdogan may have increased on CBRT to loosen its monetary policy. Also it should be noted that US president Trump has issued a harsh warning today of “devastating the Turkish economy” if it attacks Kurds in Syria. Overall, the markets could prove very sensitive to the interest rate decision and a possible rate cut could weaken substantially the TRY. On the other hand, should the bank remain on hold as expected we could see the TRY getting some support.

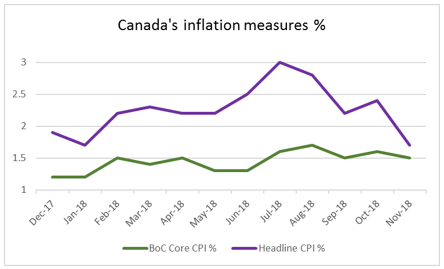

USD/CAD seems to be picking up in the past few sessions and the bearish sentiment for the CAD could be enhanced on Friday, by the release of Canada’s headline and core inflation rate for December. Currently the core CPI rate is forecasted to remain unchanged at +1.7% yoy if compared to prior month’s reading, while the BoC core CPI rate’s last reading was of +1.5% yoy, while there is currently no forecast available. Should the headline rate remain unchanged as forecasted we could see the CAD weakening as the rate remains below the BoC’s media inflation target of +2.00%. Should the core rate also remain unchanged or even slowdown, we could see the bearish sentiment growing even further. Please note that we see the risks relating to the particular release being tilted to the downside. Also please note that after BoC’s interest rate decision, we expect the direction of the Loonie to be data driven and closely related to the oil market.