Week Ahead | 13/05/2019

Weekly outlook: May 13th to 17th | US retail sales along with UK and Australia employment data to affect the markets

With the US-Sino negotiations resulting at the present stage, in a deadlock and the relationships of the two countries worsening, we expect the risk averse sentiment in the markets to continue to prevail in the coming week. Also there could be some volatility in the markets produced by Brexit should there be any developments on that front as well. As for financial releases we highlight the Australian employment data, China’s industrial production, the US retail sales growth rates, Eurozone’s second estimated GDP for Q1 and Canada’s CPI rates for April.

AUD– Employment data, China’s industrial production and Elections in focus

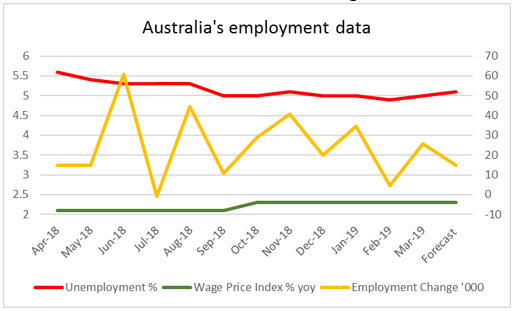

Australia’s employment data are due out this week and despite the RBA not having a dual mandate, it’s expected to affect the Aussie. The first release is during Wednesday’s Asian session and relates to the wage price index for Q1. As the rate is being released on a quarterly basis and is considered to affect inflation, we could see some increased interest in the release which if it remains unchanged or accelerates somewhat could provide some support for the AUD. On the flip side, on Thursday the unemployment rate is expected to tick up and the employment change figure to drop, both indicating some slack in employment market during April, causing the Aussie to slip. However it’s not only Australian data related to the Aussie. China’s industrial output and retail sales growth rates, both for April are due out on Wednesday. Especially the Industrial output rate could have a more substantial impact on the AUD and should it slowdown, we could see the AUD weakening, as it would imply that Australian exports to China may lessen in the future. Fundamentally, we see the case for any further escalation in the US-Sino negotiations to weaken the Aussie, as it is considered a close proxy for the Chinese Yuan. Be advised that the Aussie had been trading in one of its lowest ranges against the USD in the past week for over three years. Also, Australia will be holding elections on Saturday with the all the seats of Parliament and the majority of the Senate seats up for re-election. Be advised that currently the Labour party seems to maintain the upper hand, yet the difference is small and could be overturned.

GBP – UK employment data and Brexit to move the pound

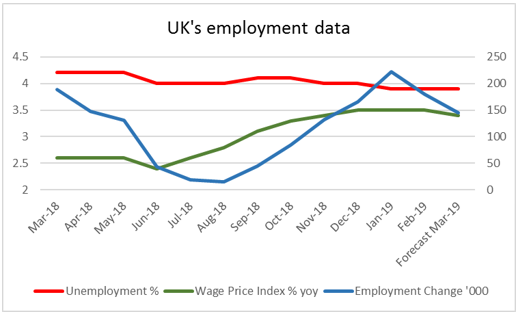

It’s expected to be a slow week for GBP traders, as for financial releases, yet on Tuesday one cannot just bypass the release of UK employment data for March. The picture of a tight UK labour market, which was the case in previous months may blur somewhat as in March there could be some signs of slack. The unemployment rate is expected to remain unchanged at 3.9%, which is considered low for UK standards. On the other hand the employment change figure is forecasted to drop and reach 145k, if compared to prior month’s 179k while average earnings on a three month basis is expected to tick down for March, reaching +3.4% yoy, if compared to February’s +3.5% yoy. Should the actual rates and figures meet their respective forecasts we could see the GBP slipping on the easing of the UK labour market. On the other hand, there could be some developments for Brexit, which could provide some volatility for the pound. The negotiations of the UK government with the Labour party seem to be at a stalemate currently, yet Theresa May is to resume talks this week. Also there are reports that May could refer to Brussels for some alteration of the agreed solution, in order to convince the Labour party. In case the negotiations break apart, we could see the pound weakening, while if the negotiations start bearing fruit, we could see the pound getting some decent support at last.

EUR- Trade, GDP, ZEW and Industrial production to affect EUR

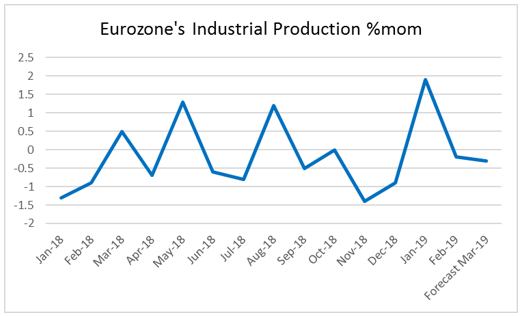

With US-Sino relationships deteriorating, the big question that arises, is whether the US will be opening a second front, this time with the EU. Should we see more headlines this week, about the US intentions to impose tariffs on European cars, we could see some volatility affecting the common currency. Various reports have mentioned the possibility the US reaching a decision on imposing the prementioned tariffs on Saturday and as we get nearer, the issue is expected to get even hotter. Judging from the tacticts the US used in the negotiations with China, we could expect a strategy leaning towards a more aggressive stance. EU officials had stated that should tariffs be imposed, there would be an immediate response. On the financial releases front, there is little to provide direction for the EUR, however some indicator’s stand out. Starting with growth rates, the pre;liminary GDP% for the Euro area at +0.4% qoq for Q1 is expected to be confirmed on Wednesday. The release is to be accompanied by an accelerating preliminary GDP rate for Germany (same period), which gets out of Q4’s stagnation (Q4: 0.0% qoq), reaching for Q1 +0.4% qoq. Overall, the rates could imply that there seems to be a slow recovery taking place, which could provide some support for the common currency. Before that, on Tuesday EUR traders are expected to closely watch the ZEW economic sentiment which is forecasted to rise further reaching 5.0 for May, if compared to prior month’s reading of 3.1 and could provide some support for EUR, as it would be evident of a more optimistic view in Germany. On the flip side, the same day the industrial production growth rate for the Eurozone, is expected to remain in the negatives (Mar: -0.3% mom vs. Feb: -0.2% mom) and could weaken EUR.

USD- Retail sales and trade relationships to be the main points of interest

With the US-Sino negotiations at a stalemate and the relationships of the two countries deteriorating, we expect the risk averse climate in the markets to continue. The chinese response is still looming and once out, could make things even worse. Yet China is not the only player in this game. The US could escalate further the trade conflict, especially if there are headlines about imposing tarrifs on the total of the imports coming from China. Currently we maintain the position that eventually the two sides will probably strike some sort of a deal, however until then it’s going to be a bumpy ride. A number of releases are due out from the US this week, however we would concentrate practically on four. We start on Wednesday, as the retail sales growth rates for April are due out. Both rates are expected to decelerate with the headline slowing down to +0.3% mom (vs. Mar: +1.6% mom) and the core to reach +0.7% mom (vs. Mar: +1.2% mom). Should the actual rates meet their forecasts, we could see the USD weakening, as it would be indicative of the average US consumer being less willing and/or able to spend more in the US economy. On the other hand, the same day the US industrial production growth rate for April is to accelerate and reach +0.1% mom(vs. Mar: -0.1% mom), getting out of the negative area. Good news are expected to continue on Thursday as the Philly Fed business index is forecasted to rise for May reaching 9.5, (vs. Apr: +8.5). Also on Friday the preliminary University of Michigan consumer sentiment indicator for May, is also expected to rise reaching 97.5 (vs. Apr: 97.2).

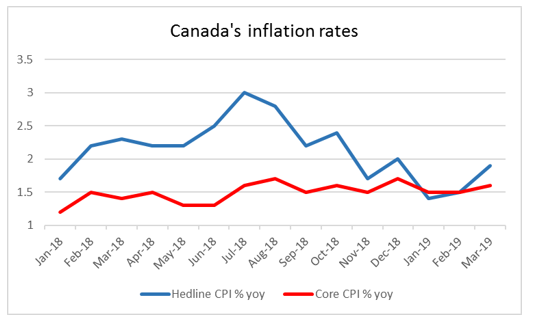

CAD- Inflation rates to provide further direction

With the CAD enjoying a solid employment report for April, Loonie traders are expected to focus on the release of April’s inflation rates for Canada. The headline rate is expected to accelerate somewhat reaching +2.0% yoy (vs. Mar: +1.9%yoy), while the core rate’s last reading for March was of +1.6% yoy. Should the actual rates accelerate, we could see the Loonie strengthening, as if they are combined with the solid employment report for April, arguments for a more hawkish stance from the BoC could get more support. On the other hand one should bear in mind that the Loonie tends to have a positive correlation with the oil market as one of Canada’s main export products is oil.