Week Ahead | 11/10/2019

Weekly outlook: October 14th to 18th| China’s releases and CPI rates in focus

With last week providing a pleasant surprise for traders at the last day, the new one begins with new hopes for better days. Finally, there seems to be some light at the end of the tunnel for Brexit, the US-Sino relationships seem to be making progress and Friday does not look so gloomy like the rest of the week, and the weekend may not be the only reason. On the financial releases front Chinese rates and figures are expected to be widely discussed next week, as well as the UK releases, albeit the pound could still be Brexit oriented. From there on, a number of inflation rates for September are due out and could keep traders interested, however also employment data from the UK and Australia are expected to spark discussions. However, let’s take a closer look at what next week has in store for the markets.

AUD – Employment data and Chinese releases in focus

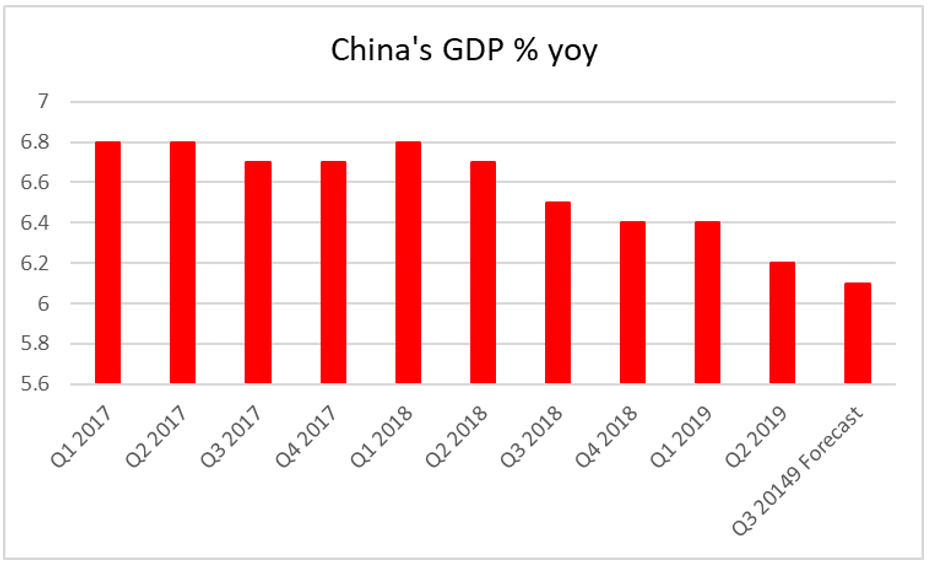

The Aussie made an impressive comeback against the USD in the past two days, practically regaining any losses made in the past 3 weeks. Main reason for the comeback is cited to be the progress made in the US-Sino negotiations as the Australian economy has a considerable exposure to China. It should be noted that Chinese releases could have a considerable effect on the Aussie starting early in the week as the Chinese trade data for September are due out on Monday. The China effect may continue, as on Tuesday China’s inflationary measures for September are due out and then on Friday, the star of Chinese releases, the GDP growth rate for Q3 is due out, wit hthe release being accompanied by a press conference of China’s National Bureau of Statistics (NBS). But its not all China for the Aussie, also Australia’s employment data for September on Thursday could provide direction for he AUD. On the monetary front, RBA’s meeting minutes are to be released on Tuesday, giving the AUD a stir probably as the markets may be scrutinising the document for any clues about the bank’s future intentions as well as what makes the bank tick.

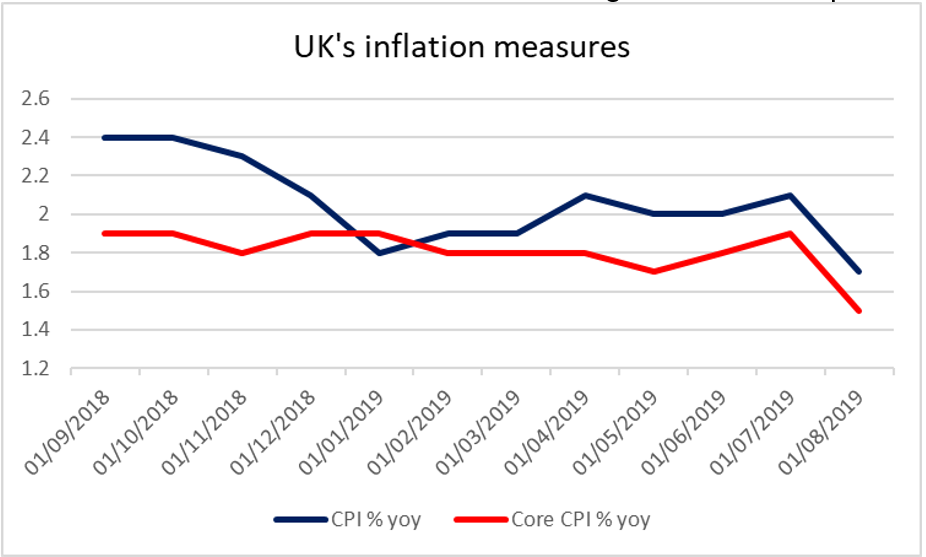

The pound finally rallied as good news about the possibility of a Brexit deal, flooded the markets yesterday. The market regained substantial hope yesterday in the afternoon as the UK and Irish Prime minister practically announced that there could be a path towards a solution of the issue. Also, the two PMs practically opened the road for a possible deal even before the Brexit deadline of the 31st of October. Intense negotiations are expected to follow the announcement and please bear in mind that the current euphoria could easily be replaced by despair, should such negotiations break down. We retain as our base scenario that the UK and the EU could agree on the terms on which the UK is to leave the trading bloc. Hence should there be further positive headlines we could see the pound retaining considerable support. However, it’s not only politics for the sterling. Also, several financial releases could play a part in the pound’s direction. Starting on Tuesday, UK’s employment data for August are due out, while on Wednesday we get UK’s inflation rates for September and we close the UK financial releases cycle on Thursday, with the release of UK’s retail sales growth rates for September.

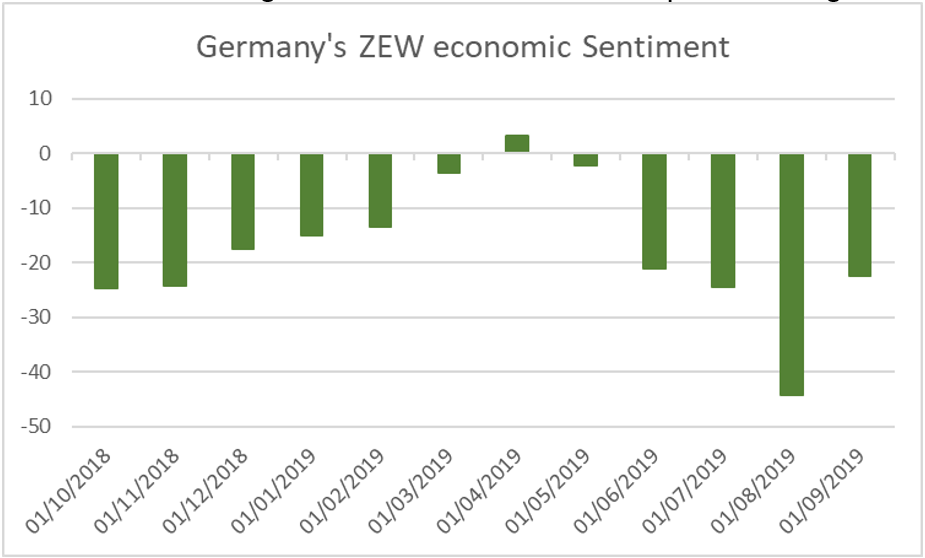

Eyes in Frankfurt are expected to be closely watching the Chinese releases and especially the trade and growth data, as the area’s exports to China are substantial. However also a number of financial releases affecting the common currency are due out next week. Starting with the Zone’s industrial production growth rate for August on Monday we are about to discover if the sector is slowing down or accelerating. On Tuesday, Germany’s more forward-looking indicator, the ZEW economic sentiment reading for October is to show whether Eurozone’s economic locomotive is still possessed by deep pessimism. On Wednesday, the main release is expected to be Eurozone’s final HICP rate for September, yet we would advise not to overlook also the trade balance figure for August. On Thursday, EUR traders could be taking a break, while on Friday the usually low impact Current account balance figure (August) is to be released and provide a more comprehensive picture of the area’s cash inflows and outflows.

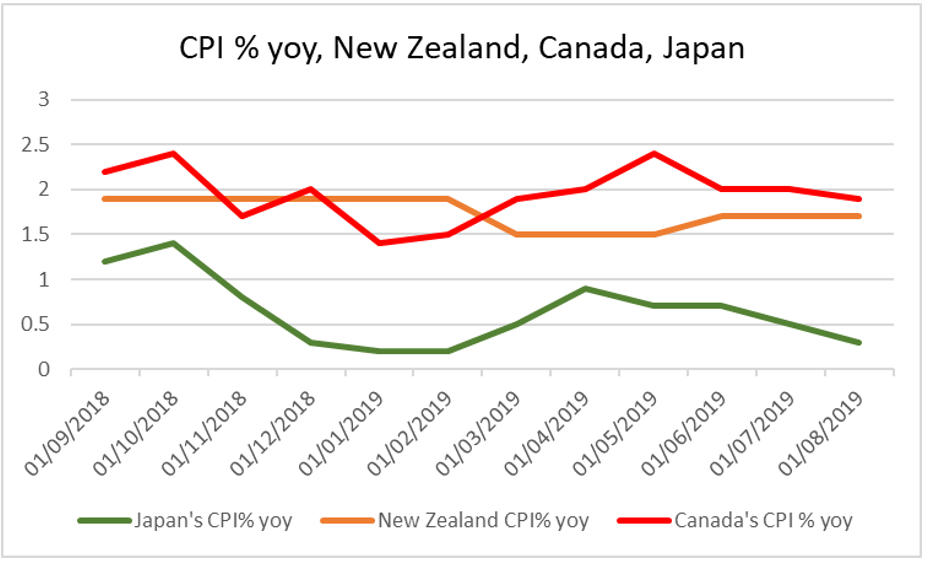

Next week inflation rates are to be released for New Zealand, Canada and Japan. In every single case, the release gains on importance albeit for different reasons. For Japan, inflation is a key macroeconomic issue as the economy suffers from the low rate level, forcing the BoJ to keep an ultra-lose monetary policy in place. At its last meeting the bank stated that it would provide further stimulus yet remained rather pessimistic about inflation rates starting to rise in order to reach the bank’s target of +2.00%. Should the September rates on Friday be even lower than the current anaemic levels, we could see the JPY weakening, as it would constitute another blow to BoJ’s efforts in order to boost inflation. Also, please bear in mind that the release is for the last month before Abe’s government, hikes the sales tax rate in October, which is heavily discussed in Japan right now and could affect price levels. In the past week, JPY had been affected substantially by safe-haven flows, as the market’s uncertainty seems like a rollercoaster, with the risk on mood near the end of the week strengthened, by the progress of the US-Sino negotiations creating safe haven outflows for the JPY which retreated. We could see the JPY continuing to be affected by such forces as its role as a safe-haven is dominant in the global FX arena. RBNZ officials were quite content when they left the meeting were a rate cut of 50 basis points was decided, as they may have thought that a double rate cut would do the job. The release of the inflation rates for Q3 on Wednesday, is expected to put the bank’s determination to the test. The rate is forecasted to slow down on a year on year level, reaching +1.4% yoy, if compared to prior quarter’s rate of +1.7%. Should the rate slowdown as forecasted, we could see RBNZ having second thoughts about remaining on hold. It should be noted that the Kiwi was benefited by the progress in the US-Sino negotiations and RBNZ officials will also be on the look out on the release of the Chinese indicators. On the same day (Wednesday) in the American session, we get Canada’s inflation rates for September. After today’s impressive release of the Canadian employment data, we could see Looney traders eyeing the CPI release for further gains. Should the rates accelerate and if combined with the tightening of the Canadian labor market as marked today, we could see confidence slowly returning to the BoC and governor Poloz, adopting a more hawkish stance. Should the rates accelerate, we could see the CAD strengthening, yet be advised that the Looney also has its eyes turned to the oil market and could be affected by any fluctuations of the commodity’s prices.

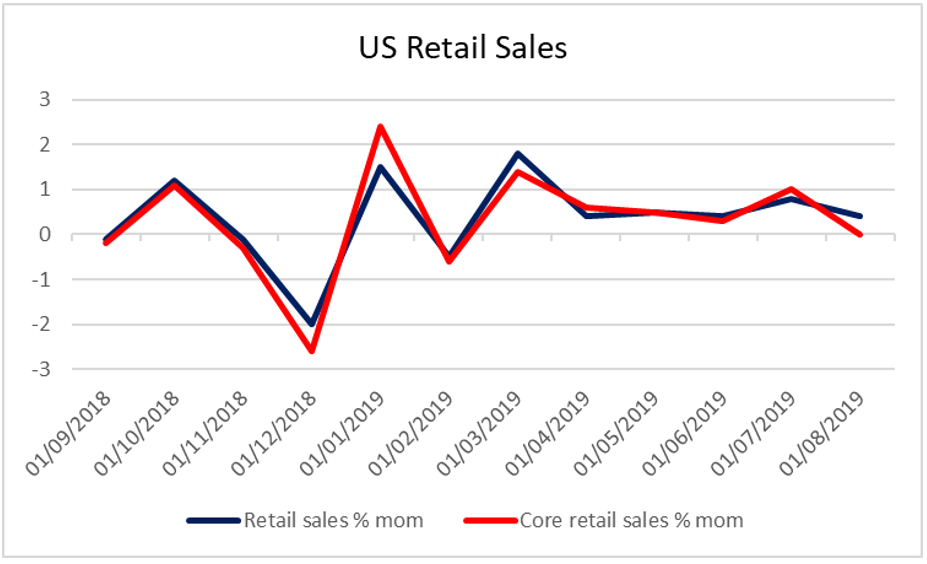

The USD had a rough week, with increasing worries about a possible breakdown of the US-Sino negotiations on Thursday and today. As these lines are written, the negotiations are slowly being wrapped up and Chinese Vice Premier is to meet US President Trump. There was a very positive climate today about further progress being made, in contrast to what was the feeling the previous days. Should there be further progress in the trade talks, or even a possible mid agreement, including a currency pact or not, we could see the US intentions for further tariffs on imports from China, being postponed from next week to a later stage. We expect to see if the much-discussed progress is actually going to be expressed in a joint US-Sino statement. At the same time, we would not be surprised to see President Trump tweeting about the issue. On the internal political front, please note that the pressure on President Trump is increasing as a result of the ongoing impeachment probe, while at the same time the US President is being heavily criticised about the handling of the Turkish operations in northern Syria’s Kurdish region. On the monetary front, as the Fed’s meeting is approaching, statements made by Fed officials, are expected to gain more and more weight and at the same time being scrutinised by analysts for further clues on whether the bank is to cut rates for a third time or if it will remain on hold. As for financial releases, it seems like a slow week for the greenback, yet some releases seem to stand out of the crowd. We tend to view the release of the retail sales growth rates for September, as the star of next week’s financial releases however also production data such as the NY Fed Manufacturing and the Philly Fed Business index, both for October, as well as the industrial production growth rate for September could gather some interest.