Week Ahead | 04/02/2019

Weekly outlook: February 4th to 8th | Are RBA’s and BoE’s interest rate decisions going to continue the dovish tone?

Entering the new week, two interest rate decisions, the RBA’s and BoE’s could have wider implications than expected. After a number of central banks are turning dovish due to the rising global risks and outlook uncertainty the next two decisions could be confirming the dovish tone. On the other hand, as a number of Asian countries will be closed for the New Lunar year celebrations and the US calendar is expected to have only a few high impact releases, there could be some surprises for the markets. Also let’s not forget that some US releases, delayed due to the US shutdown could have a more significant impact that usually, should they be released this week.

AUD – RBA’s interest rate decision in focus.

RBA is to announce its interest rate decision tomorrow during the Asian session (03:30 GMT) and is widely expected to remain on hold at +1.50%. Currently AUD OIS imply a probability for the bank to remain on hold of 98.90% strengthening the arguments for such a scenario. Despite RBA’s optimistic tone, weakening financial data and trade uncertainty may provide a number of more dovish comments in the accompanying statement. Analysts point out that market expectations have started to emerge for a possible rate cut in contrast to the bank’s view that it’s next move is to be a hike. Should the bank negatively surprise the markets we could see the Aussie weakening. Despite the inflation rate for Q4, being better than expected, it still slowed down if compared to its prior reading, distancing itself from RBA’s target and could ultimately provide for further dovishness. Add to that also a possible slowdown of the retail sales growth rate (forecast:-0.1% mom vs. Prior:+0.4% mom) for December, which is due out just before RBA’s interest rate decision being released and the bearish sentiment for the AUD could grow even further. Should the bank also release any downward revisions in its growth and inflation forecasts on Friday, in its Monetary policy statement we could see the bears roar even louder for the Aussie.

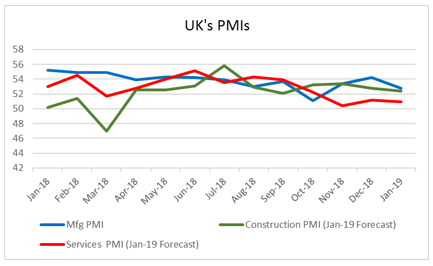

In case you are wondering, there is not a vote for Brexit in the UK parliament’s agenda this week, but we could see headlines reeling from Brussels if Theresa May has any negotiations with the EU. Currently the UK PM seems to be forming her new Brexit proposal and should things work out as planned, we could see her meeting with EU officials late this week and returning to the UK parliament by February 13th or 14th. For the time being businesses in the UK seem to bracing for a hard Brexit and the PMI’s for January could indicate lower activity. Given that the Manufacturing PMI already has dropped (January: 52.8 vs. December:54.2), should the Construction PMI (forecast: 52.4 vs. Prior: 52.8) and the Services PMI (forecast: 50.9 vs. Prior: 51.2) also drop, we could see the bearish sentiment being enhanced for the pound. Please bear in mind that after the manufracturing PMI dropping more than expected on Friday, we see the risks tilted to the downside for the release of the other two PMIs (Construction and Services). Especially for the allmighty UK services PMI which is forecasted to dangerously near the contraction cut off point of 50.0. Never the less the BoE interest rate decision on Thursday, is also expected to influence the pound’s direction. The bank is widely expected to remain on hold and maintain the current interest rate level of +0.75%. Currently GBP OIS imply a probability of 98.9% for such a scenario strengthening arguments for the bank to remain on hold. As the bank is not expected to hike rates until after Brexit and given the latest Brexit developments, it will be interesting to see how the bank will acknowledge any potential risks in case of a hard Brexit. As the bank had warned in the past, a hard Brexit could trigger a recession for the UK economy and we could see it intensifying its language tone due to the latest developments. Should the bank have a more dovish tone and a shift of its stance accordingly, we could see the pound weakening substantially near the end of the week.

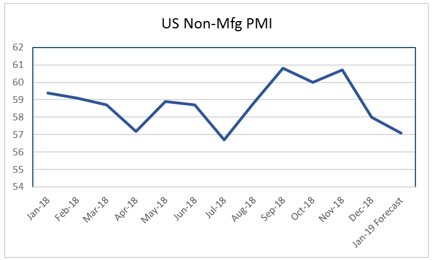

After last week’s FOMC interest rate decision and January’s employment report kept the market participants on the edge of their seats, this week seems to be rather slow for US financial releases. Starting with Monday’s factory orders growth rate for November, the rate is expected to accelerate reaching +0.2% mom if compared to prior month’s reading of -2.1% mom. Should the rate accelerate as forecasted, we could see the USD getting some support as the acceleration is substantial, the rate gets out of the negative area and is in line with the higher than expected reading of Friday’s ISM manufacturing PMI for January. On the other hand, should the ISM non-manufacturing PMI for January drop (forecast: 50.9 vs. Prior: 51.2) on Tuesday as forecasted, we could see the USD weakening. In general as there seems to be a lack of high impact releases available to support the USD, we could see the greenback finding difficulties to find further support. Never the less, we could see a number of US financial releases coming out this week, which were delayed due to the partial US government shutdown, providing surprises during the week. Also the fact that a number of Asian markets will be closed for the Lunar New Year holidays, could provide for some thin trading during the week, which could in turn provide for some sharp reactions.

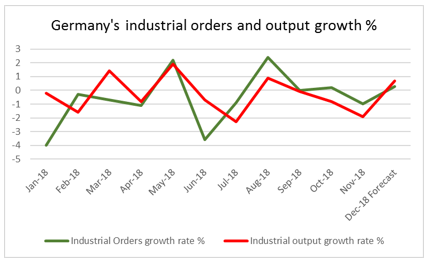

The common currency could be getting some small hopes from the release from the release of the German industrial orders and output growth rates for December. The industrial orders growth rate for the Eurozone’s biggest economy is forecasted to accelerate substantially, confirming the German economy minister’s (Peter Altmaier) January comments that the order books are full. Should the industrial orders growth rate accelerate as forecasted (forecast: +0.3% mom vs. Prior: -1.0% mom) on Wednesday, as well as the industrial output growth rate (forecast: +0.8% mom vs. Prior: -1.9% mom) on Thursday, the EUR could get some support as the as both rates are expected to accelerate substantially and get out of the negative area, showing growth again. Never the less the common currency will have to surpass a bearish momentum first, which could be enhanced by the release of Eurozone’s retail sales growth rate for December (forecast:-1.6% mom vs. Prior:+0.6% mom), which is forecasted to slowdown, showing contraction of retail sales during the Christmas month. The same should apply for a possible slowdown for Eurozone’s producer prices index (forecast:-0.7% mom vs. Prior: -0.3% mom) for the same period, as it is forecasted to drop deeper in the negatives, marking a possible retreat of inflationery pressures in the Eurozone.

On Wednesday (21:45,GMT), just before Thursday’s Asian session we get New Zealand’s employment data for Q4. The unemployment rate is expected to rise reaching 4.1%, if compared to Q3’s reading of 3.9% and the employment change rate to slowdown reaching +0.3% qoq, if compared to prior quarter’s reading of +1.1% qoq. On the flip side the labour cost index is forecasted to tick up reaching +2.0% yoy, if compared to prior reading of +1.9% yoy. Overall, we see the results indicating some slack in New Zealand’s labour market, should the forecasts be realised and the rise of the unemployment rate could overshadow the tick up of the labor cost index. Should the bearish feeling for the Kiwi be strengthened we could see it weakening, however it should also be noted that the NZD/USD had a bullish course over the two past weeks which may pose an obsticle in the bears way. On Friday we ge the Canadian employment data for January. The employment change figure is forecasted to drop (forecast:6.0k vs. Prior:9.3k) and at the same time the unemployment rate is expected to tick up (forecast: 5.7% vs. Prior: 5.6%), providing arguments for the bears, regarding the Loonie. Once again it should be noted that the CAD just as the NZD (see previously) had strengthened against the USD in the past two weeks and that dynamic will be put to the test.