Week Ahead | 02/08/2019

Weekly outlook: August 5th - 9th | RBA, RBNZ and GDP rates to provide direction

With a very eventful week nearing its end, the next seems to be less turbulent, yet still could shake the markets. From New Zealand and Australia, we get RBNZ’s and RBA’s interest rate decisions which are to provide further direction for the Aussie and the Loonie, yet note that New Zealand’s employment data for Q2 are coming out before RBNZ’s interest rate decision, while the next day China’s trade balance is due out . The EUR is about to enjoy a week with only a few financial releases yet the industrial orders and output growth rates of Germany may still provide volatility. Brexit politics may take a back stage for the pound, yet near the end of the week UK’s GDP growth rate for Q2, will be keeping pound traders busy probably. The GDP growth rate of Japan on the other hand may provide volatility for the JPY on the same day. Also on Friday Loonie traders could be keeping an eye out for Canada’s July employment data. Last but not least, the troubled USD, will probably have only a few financial releases out after Wednesday.

AUD – RBA Interest rate decision to dominate

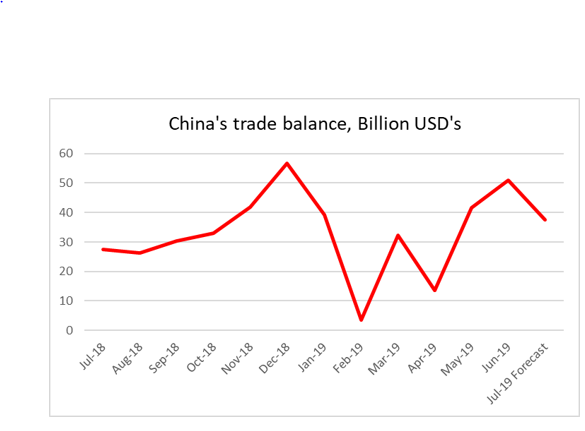

The Aussie maintained a clear downward trendline which intensified yesterday after the new threats for possible US tariffs on Chinese products, reaching a new 6 month record low level. The Aussie kept falling even as Australia’s CPI and retail sales growth rates outperformed expectations. Next week RBA’s interest rate decision is expected to highlight the Aussie’s direction. The bank is to release its cash rate decision on Tuesday early in the Asian session and is widely expected to remain on hold at +1.00%. Currently AUD-OIS imply a probability for the bank to remain on hold of 88.17%, with the rest favouring a rate cut of 25 basis points. In its last interest rate decision (beginning of July) the bank cut rates by 25 basis points for the second consecutive time and seems be willing to remain in a wait and see position in order to be able to appreciate the overall effect of the cuts. Given that the bank may want to maintain the way clear for further rate cuts, the US-Sino trade war seems to be entering a period of deeper uncertainty and the inflation rate is still below the bank’s desired band (+2-3% yoy) despite picking up pace, we tend to expect an accompanying statement tilted to the dovish side, which could weaken the Aussie further. On the other hand, a more neutral stance may be favoured as we mentioned above the bank may want to maintain a wait and see position. It should be noted though that also, China’s releases could be weakening the AUD somewhat. On Thursday, China’s trade balance for July is due out and is expected to be a narrowed surplus, which could not bear good news for the AUD. Should China’s trade balance, be coupled with an enhanced negative import growth rate, we could se the adverse effect on the Aussie magnify. Also a retreat of inflationary pressures in the Chinese economy on Friday, could have an adverse effect on the Aussie. Please bear in mind that fundamentally the Aussie could weaken further should the US-Sino trade relationships escalate further in the week to come.

GBP – UK’s GDP front and center

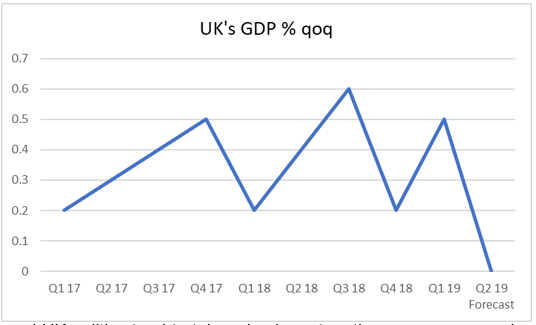

With BoE’s interest rate decision maintaining the current levels, as was widely expected, the main element of the event was the warning the bank issued about Brexit and a global slowdown, by lowering its forecasts on Thursday. On the political front Brexit and UK politics tend to take a back seat as the summer recess has begun for the UK Parliament, yet we would not be surprised to see new headlines about UK politics. Especially, after the majority of the Tories was reduced to merely one MP, after the Liberals won a by election in Wales. Despite the Conservative party still maintaining a (thin) majority in Parliament UK politics are to be come even more shaky, promising a storm next month. As a general comment we tend to see UK politics to exercise further pressure on the pound, as Johnson’s Brexit rhetoric remains hard and UK politics uncertain. On the financial releases front, UK GDP rate preliminary release for Q2 on Friday stands out. The quarter on quarter rate is forecasted to slow down and reach stagnation and should that be the case, we could see the pound weakening substantially. Also some bearish effect could be in the cards for the pound should the Services PMI underperform market expectations on Monday.

EUR – Quiet week ahead

Fundamentally the common currency could be negatively affected by the increased insecurity regarding global trade and may remain under pressure. Especially as the US-Sino trade spat tends to escalate we could see the single currency remaining under pressure, as some analysts tend to underscore it’s negative effect on Germany’s manufacturing output and trade balance. On the positive page of Eurozone’s fundamentals could be the recent announcement of the trade deal with the US about beef, which could ease worries somewhat. On Tuesday we should be getting a taste of the effect as Germany’s industrial orders growth rate for June is due out, while on Wednesday its sister indicator, Germany’s industrial output growth rate, also for June is due out. German financial data releases are to be crowned by the release of Germany’s trade data for the same month. Special attention is expected to be given not only to the trade balance per se, but also to the export growth rate which keeps the German economy going. Prior to that, on Monday we get the final readings of France’s, Germany’s and Eurozone’s PMI’s, yet market reaction may be somewhat muted as the preliminary releases may have absorbed most of the market’s reaction.

JPY – Safe haven flows and GDP to show direction

Should we have to single out one market reaction to Trump’s tweets on Thursday, regarding the US additional tariffs to be applied to Chinese imports, that would be the surge of the JPY. The yen’s rally against the USD seems to have been fuelled by an enhancement of the risk off sentiment of the market, which was quickly expressed by safe have inflows for the Japanese currency. Should there be further escalation in the US-Sino relationships, we would not be surprised to see JPY strengthening further. However, we would like to draw the attention to another trade war as well. As the Japanese government has removed South Korea from a list of privileged trading partners, the Koreans threatened with counter measures, a move which also carries some national patriotism flair, among the two countries. As for financial releases, albeit they don’t affect he JPY so intensely, we note the release of the household spending growth rate for June on Monday. The star of Japanese releases though is expected to be GDP growth rates for Q2, on Friday. Should the releases show a slowdown, especially the GDP one, we could see the JPY weakening

NZD- RBNZ and employment data in focus

Like the Aussie so the Kiwi has had a bearish course against the USD in the last week. It should be noted that the recent escalation of the US-Sino also intensified the weakening of the Kiwi. On the financial releases front, two releases stand out, New Zealand’s employment data on Tuesday and of course RBNZ’s interest rate decision on Wednesday. However first comes first. On Tuesday the unemployment rate is expected to tick up reaching +4.3%, while the job growth rate is expected to accelerate and reach +0.4% qoq, if compared to prior reading of -0.2% mom. Also the labor cost index is expected to accelerate slightly reaching +2.1% yoy, if compared to prior reading of +2.0% yoy. The forecasted rates and figures some tendencies for a tightening of New Zealand’s labour market and if realised as expected could provide a boost for the Kiwi. On Wednesday, RBNZ’s interest rate decision is due out. The bank is widely expected to cut rates by 25 basis points and currently NZD OIS seem to show that the market has fully priced in (100%) the cut. With the interest rate decision, being fully priced in, should it be materialised, we could see the market’s attention turning to the accompanying statement. Given the uncertainty surrounding the economy of New Zealand, we would not be surprised to see the document’s tone being slightly tilted to the dovish side, as is wide uncertainty about China and global trading conditions. Should the bank signal that more rate cuts are possible, we could see the event having a bearish effect on the Kiwi, extending its drop against the USD.

USD- Second tier releases ahead

With one of the most eventful weeks nearing its end with the release of the US employment report for July, we couldn’t resist to comment on it. In politics, the US-Sino trade relationships hit new lows as the Shanghai negotiations between the two parties ended, with no sign of progress on the horizon. Not a day went by and the US President was tweeting about new tariffs of 10% to be imposed on Chinese imports by September 1st. We could see the situation escalating further should there be a harsh response from the Chinese which for the time being, stated that should the US actually impose the new tariffs, there would be retaliation measures. A by effect that the recent escalation had, was to widen the belief that more rate cuts are to come from the Fed, after its decision to cut rates by 25 basis points, for the first time in a number of years. The USD, had a positive reaction to the Fed’s decision as Fed Chairman Powell was quick to note that it would not be a prolonged easing cycle, dismissing fears expressed by some analysts. Never the less tables were turned the next day, as US President started tweeting around. Many analysts were quick to comment that the timing of the tweets was not by coincidence, but exactly to increase the chances of more rate cuts to come by the Fed. It should be noted that the week ended with US employment report sending out mixed signals, as the NFP figure dropped (as expected), the unemployment rate remained unchanged and on the positive side, the average earnings growth rate picked up pace by a bit. Next week, we could see Fed officials making some statements, especially from Rosengren and George which dissented the decision. Statements from Fed officials are expected to be closely watched and could affect USD’s direction. On the political end we could see the US-Sino relationships once again dominating headlines, especially should there be any easing as the US president left a back door open to negotiations. As for financial releases, albeit there are to be a number of them, we tend to single out the release of the ISM non manufacturing PMI for July on Monday and the PPI final demand for July on Friday, with both indicators forecasted to treat the USD favourably.