Week Ahead | 01/10/2018

October 1st to 5th | The US employment report with its NFP figure, along with Brexit and RBA’s interest rate decision, set to define the week.

As we are entering the new week the US employment report is expected to dominate the week’s headlines in regards of US financial releases, near the end of the week but the US PMI’s for September could also influence the USD’s direction until Friday. On the other side of the Atlantic, the UK political scene could be providing headlines as Theresa May’s party will be having its annual conference in Birmingham and a heated debate about Brexit is expected, with Boris Johnson directly challenging Theresa May’s Chequers Brexit plan. On the monetary spectrum, RBA’s interest rate decision could rattle the AUD, along with Australia’s retail sales growth rate for August on Friday.

US Dollar- Rough beginning with a sweet end of the week.

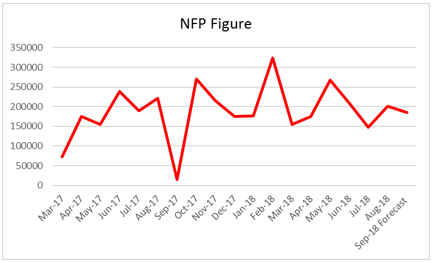

Starting with the king, the USD could have a have a rough start in the week, as the US Manufacturing PMI for September is expected to drop to 60.3, if compared to August’s reading of 61.3. The same scenario is to be repeated on Wednesday as the Non-Manufacturing PMI is also expected to drop, reaching as low as 58.1, if compared to previous month’s reading of reading of 58.5. However, the rewards for the USD could be hiding in the US employment report for September. From the report three key indicator’s stand out: the Non-Farm Payrolls (NFP) figure (forecasted: 185k vs Prior of 201k), the average hourly earnings growth rate (forecasted +2.8% yoy vs. prior +2.9% yoy) and the unemployment rate (forecasted 3.8% vs. prior 3.9%). Despite two out of three key indicators forecasted to be weakening the USD (the average hourly earnings growth rate and the NFP figure), we could say that they remain at rather tolerable levels and the overall picture is of a tight labor market, which allows the Fed to proceed at its current rate hike path and hence could provide some support for the greenback.

GBP- Entering a bear’s week?

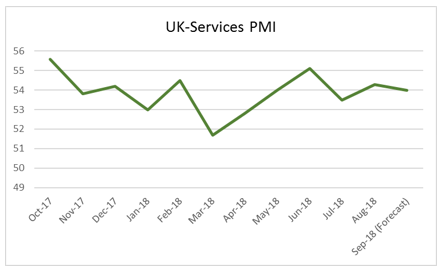

Across the Atlantic, the UK will be having a rather difficult week ahead as the Conservative party’s conference in Birmingham is expected to have some heated discussions on the agenda. With PM Theresa May fighting a crucial political battle for the control of her party against main rival Boris Johnson, tensions could feed the headline reels of media. Brexit is the main topic of confrontation and no side seems to be taking prisoners. Should there be further negative headlines about Brexit investor’s confidence for the pound could be undermined and the pound could be weakened. The crescendo of the conference is expected to be on Wednesday when Theresa May herself will take the podium and deliver her speech. But it’s not only the fundamentals which could be weakening the pound this week. UK’s financial releases could also be against the sterling as they are forecasted to have lukewarm results if not drop. Specifically starting on Monday, the Manufacturing PMI for September, is expected to drop (forecasted 52.5 vs. prior 52.8), as well as the Construction PMI (September forecasted 52.5 vs. prior 52.9) and mainly the almighty Services PMI (September forecasted 54.0 vs. prior 54.3). Hence, we could be in for a bearish week for the pound.

CAD- Pushed by NAFTA and employment data

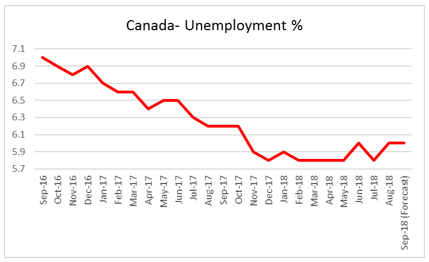

The CAD started the week with a bang as the US and Canada were able to hammer out an agreement regarding the basic principles of the new NAFTA agreement. The CAD had already started to strengthen on Friday as hopes grew on a new NAFTA agreement. During the weekend the two sides had intense negotiations and a lot of work was put in for them to announce that a deal has been struck just as the midnight deadline was about to expire. But there could be other positive news to come for the Loonie. On Friday, one could only highlight the release of the Canadian employment data for September, which could also provide some support for the CAD as the Employment Change figure is forecasted to rise to +24.7 (vs. prior -51.6k) and the unemployment rate to remain stable at 6.0%. The rosy picture is blurred somewhat though, as the Ivey PMI indicator for September is expected to drop to 61.4 (vs. prior 61.9) on Thursday and the Trade balance deficit for August is expected to widen to -1.44B (vs. prior -0.11B) on Friday.

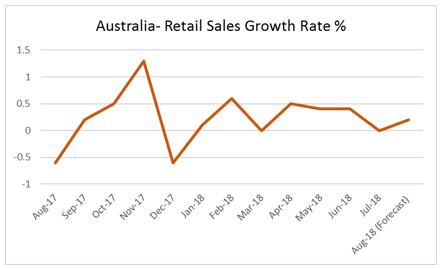

AUD- RBA’s interest rate decision and retail sales could provide boost

The AUD course could be fundamentally dictated by any further developments of the US-Sino trading relationships. Should there be further escalation, we could see the Aussie weakening and vice versa, as Australia’s currency is considered a close proxy of the Chinese yuan. Apart from the fundamentals, on the financial releases side, we see three releases playing a key role for the AUD this week. The first would be RBA’s interest rate decision. The bank will release its interest rate decision on Tuesday during the Asian session and is widely expected to remain on hold at +1.50%. Currently AUD OIS imply a probability of 99.59% for the bank to remain on hold. Should the bank remain on hold as forecasted, we could see the market’s attention turning to the accompanying statement. As the economy seems to carry rather healthy indicators with an inflation rate near the bank’s target, a low unemployment rate and a rather strong GDP growth rate, we could see some hawkish elements being included in the accompanying statement, providing a more upbeat tone and supporting the Aussie. The second release would be Australia’s trade balance surplus for August, which is expected to narrow a bit (forecasted +1.4B vs. prior +1.5B) but remains at rather tolerable levels. Last but not least the retail sales growth rate for August could be providing some support for the Aussie as it is expected to accelerate a bit (+0.2% mom vs. 0.0%mom).