Week Ahead | 18/08/2017

August 21st – 25th | Jackson Hole economic symposium, key data in focus

• In the US, the annual Jackson Hole economic symposium will kick off. Keynote speakers include Fed Chair Yellen and ECB President Draghi, which suggests that the financial world will be tuned in for any fresh policy signals.

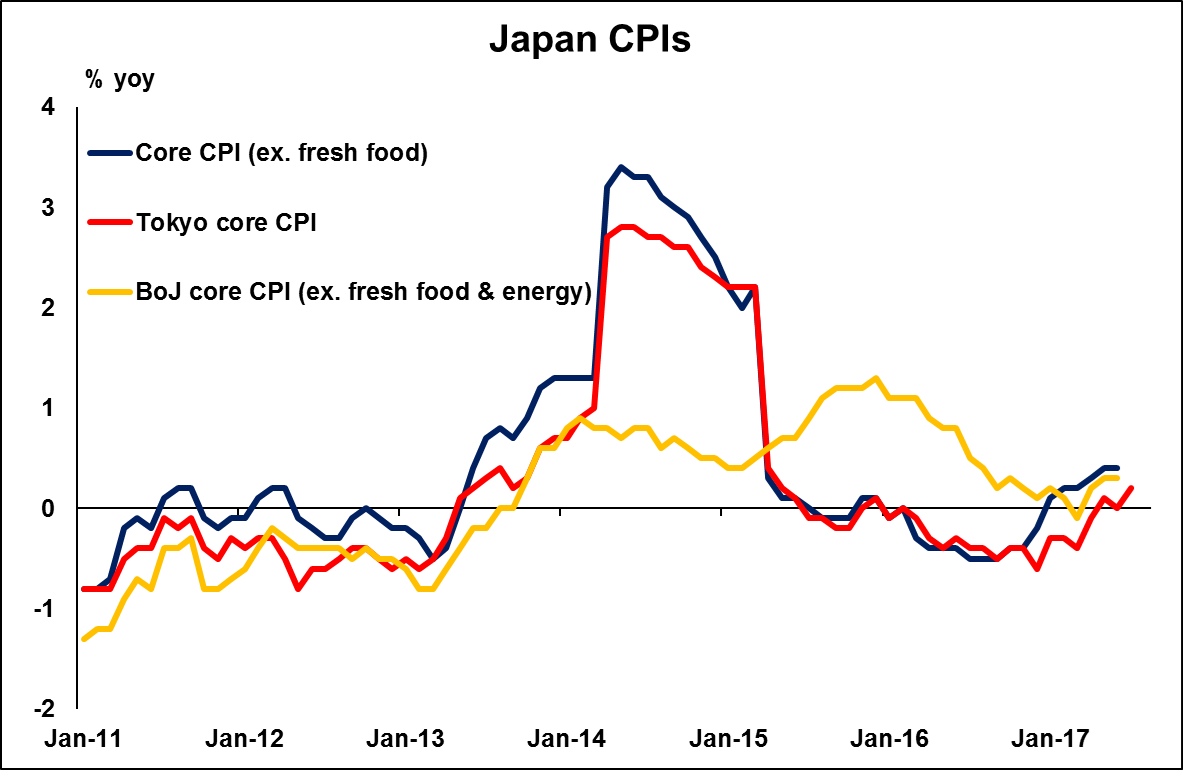

• In Japan, core inflation is expected to accelerate slightly. Even though that would be encouraging for the BoJ, we think it is far too early for speculation regarding a potential reduction in stimulus.

• We also get key economic data from Germany, Norway, the Eurozone, the UK, and the US.

On Monday, we have a relatively quiet day, with no major events or indicators on the economic agenda.

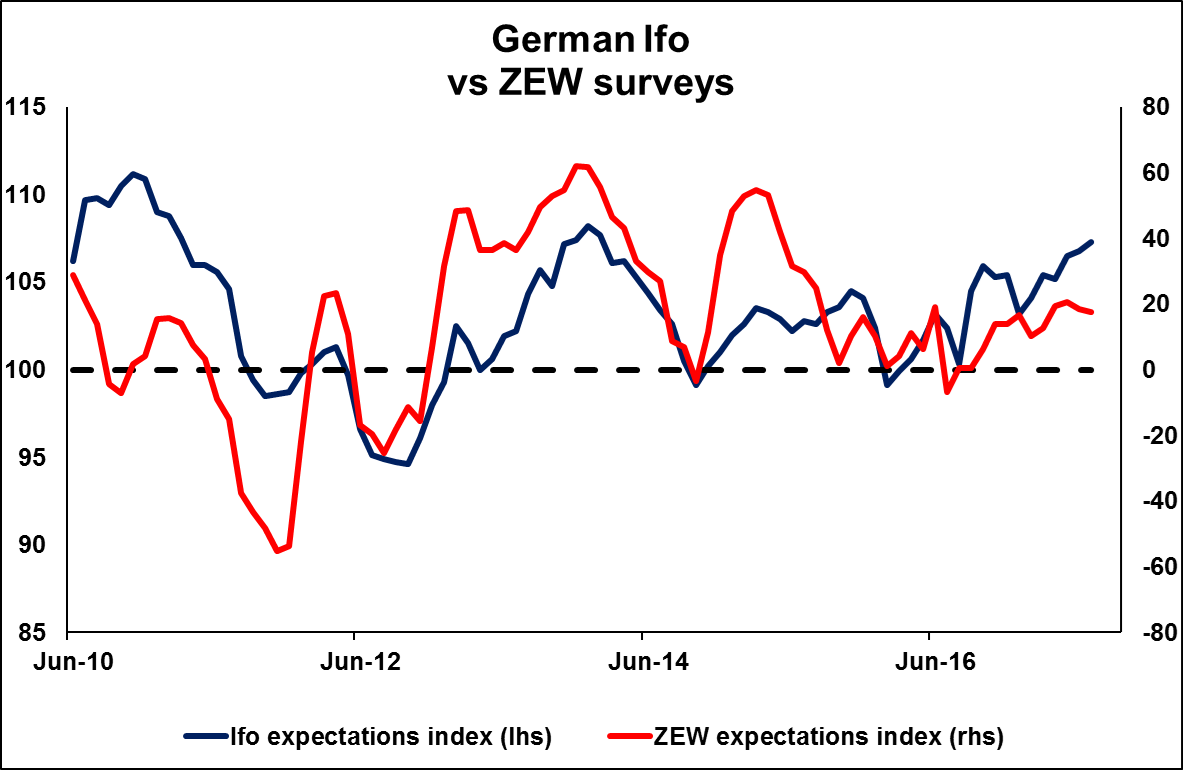

On Tuesday, Germany will release its ZEW survey for August, while on Friday, we get the nation’s Ifo survey for the same month. The forecast is for all of these indices to decline slightly, but to still remain at healthy levels. Even though the ZEW expectations index declined somewhat in recent months, the survey’s current conditions print remained near all-time highs. Meanwhile, the Ifo composite index hit a new record high in July for the third consecutive month, indicating that “sentiment among German businesses is euphoric”, as the Ifo institute phrased it. As such, we doubt that any minor decline in these figures will be particularly worrisome for ECB policymakers.

As for the bigger picture, the ECB remains set to make an announcement around QE tweaks in the “autumn”, which suggests we will probably get fresh signals at the September or October meetings. Although incoming data will likely play a critical role, we think that a realistic scenario is one where the Bank removes it QE easing bias in September, thereby paving the way for a formal announcement in October that the pace of QE purchases may be reduced by the turn of the year.

With regards to Fed Chair Yellen, her speech will center on financial stability and as such, any comments on the pace of future rate hikes appear somewhat unlikely. That said, same as with Draghi, her remarks will still be watched closely as she could always make a reference to the outlook of the US economy that indirectly conveys her policy view. Should she echo recent comments from New York Fed President William Dudley and hint that she could vote in favor of another rate hike this year, markets could reprice the likelihood for such action. The probability for another hike this year declined further recently, after the July FOMC minutes showed more officials being concerned with low inflation, and now rests at 40% according to the Fed funds futures.

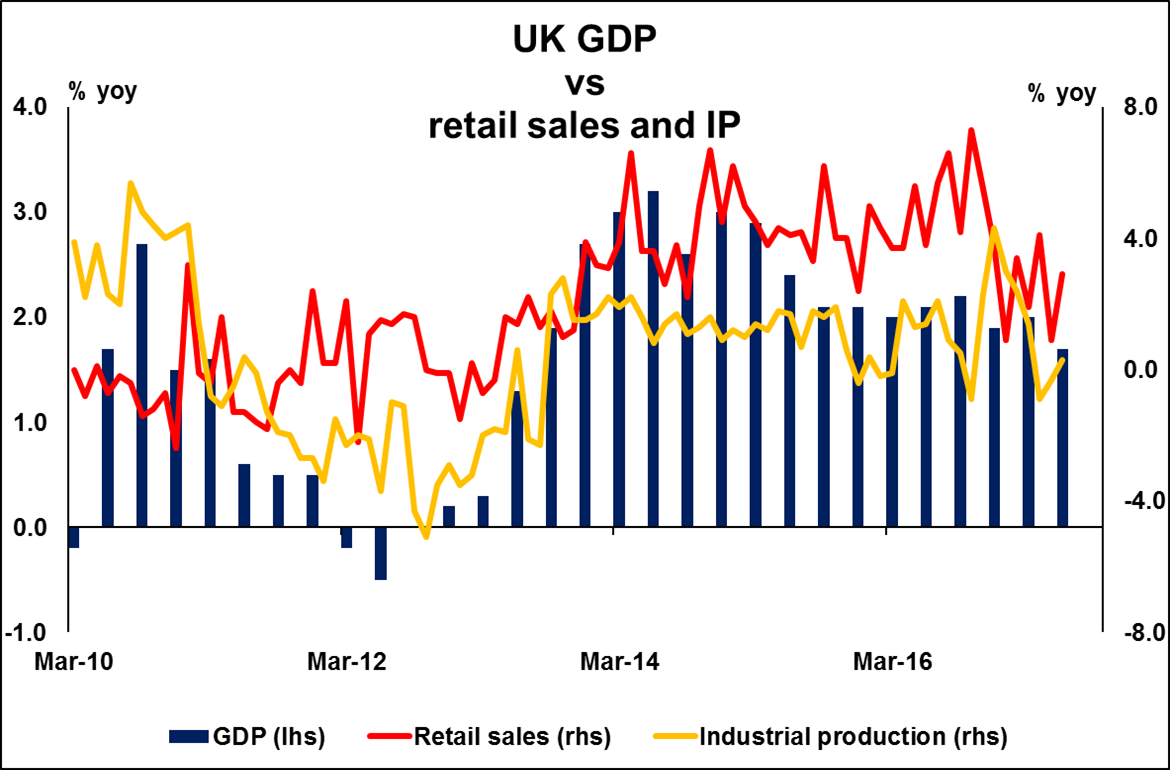

In the UK, the 2nd estimate of GDP for Q2 is due out. The forecast is for the 2nd reading to confirm the preliminary one and show that UK growth was only +0.3% qoq. If we were to see any revision, we think that it could be to the upside, as the only major indicator for Q2 released after the first GDP estimate was industrial production for June, which was stronger than expected. Besides the GDP print, this data set will also include business investment data for Q2, which we expect to attract a lot of attention. Back in June, BoE Governor Mark Carney noted that a BoE rate hike may depend mainly on whether weaker consumption growth is offset by stronger business investment, and on whether wages begin to firm. Given that wages have shown little-to-no signs of firming in recent months, a pick up in business investment may be needed to keep alive some speculation for a BoE hike. If we were to see investment moderating as well, then the market probability for a rate increase this year could drift towards 0%, from 20% currently according to the UK OIS.

Finally on Friday, Japan’s CPI data for July will be in the spotlight. No forecast is available for the headline print, while the core CPI rate is expected to have ticked up. Our own view is that the headline rate could rise as well, something that we base on the nation’s forward-looking Tokyo CPIs for the month, where both the headline and the core rates moved higher. Even though further progress in the inflation outlook would undoubtedly be encouraging news for BoJ policymakers, we think it is far too early for speculation regarding a potential reduction in stimulus. Under its QQE with yield curve control framework, the Bank has explicitly committed not only to achieve its 2% inflation target, but to actually overshoot it. Thus, even in case the CPI rates rise somewhat further, as long as they remain so far from the target, we maintain our view that the BoJ is likely to keep its ultra-loose policy framework in place.