Daily Commentary | 29/07/2019

USD keeps gains after GDP release

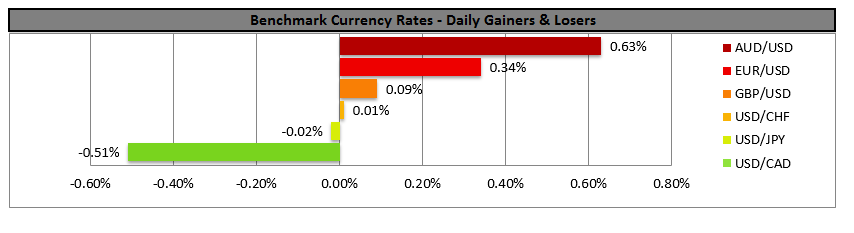

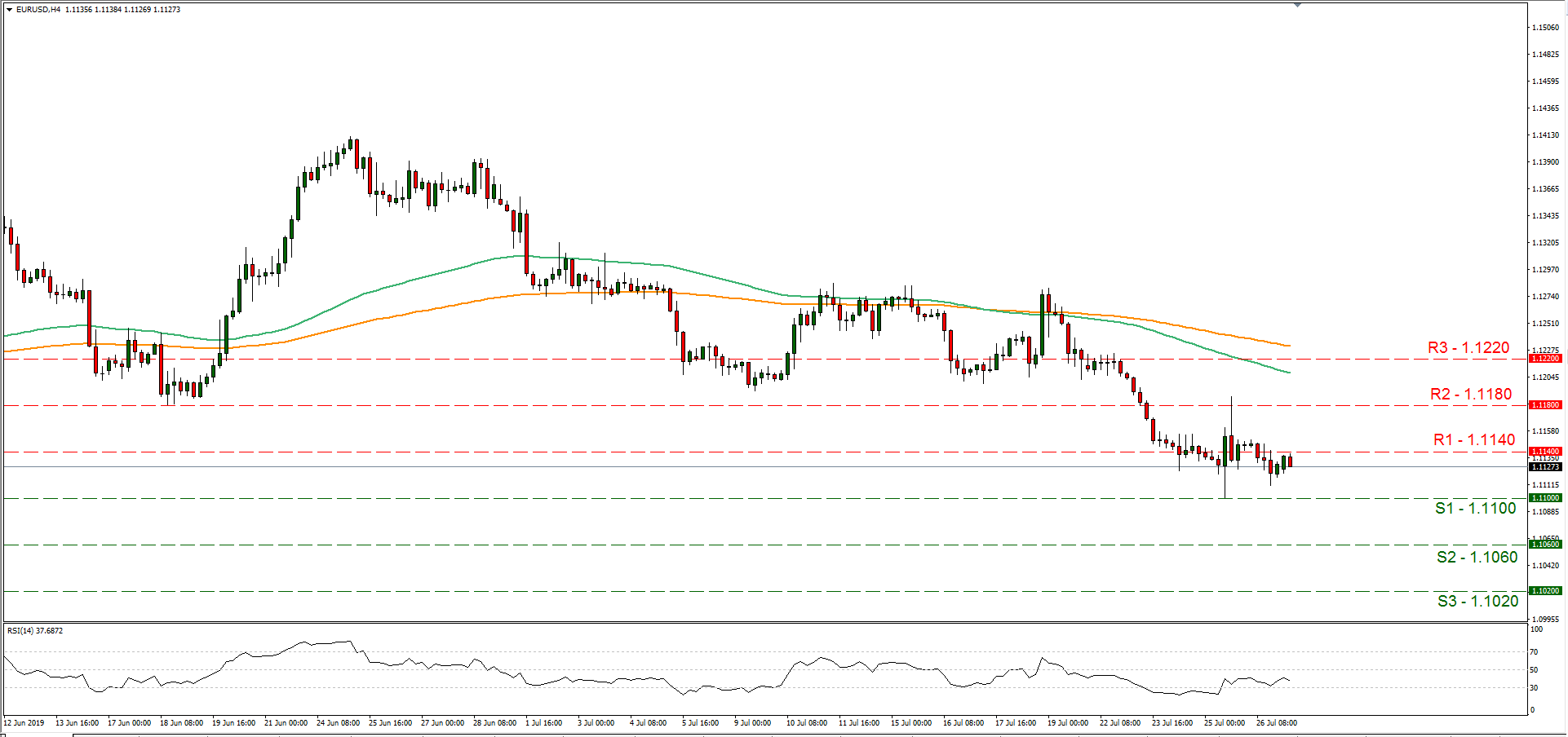

The USD remained rather strong against a number of its counterparts after the release for the preliminary US GDP for Q2. The GDP growth rate outperformed expectations reducing worries for a prolonged easing period by the Fed were reduced. The Fed is widely expected to cut rates in its next meeting, yet analysts point out that the cut may be of a preemptive nature. It should be noted that other currencies such as the EUR and the GBP have been weak for the past few days underscoring the strength of the USD. We expect volatility to be maintained for the USD this week as the Fed’s interest rated decision on Wednesday and the Employment data on Friday are due out. EUR/USD remained below the 1.1140 (R1) resistance line during today’s Asian session, maintaining a rather sideways motion. We could see the pair have some bullish tendencies, should the market start positioning itself for the FOMC interest rate decision on Wednesday. Should the pair’s long positions be favored by the market, we could see it breaking the 1.1140 (R1) resistance line and aim for the 1.1180 (R2) resistance level. Should EUR/USD come under the selling interest of the market, we could see it breaking the 1.1100 (S1) support line and aim for lower grounds.

Oil remains rather steady in midst of talks with Iran

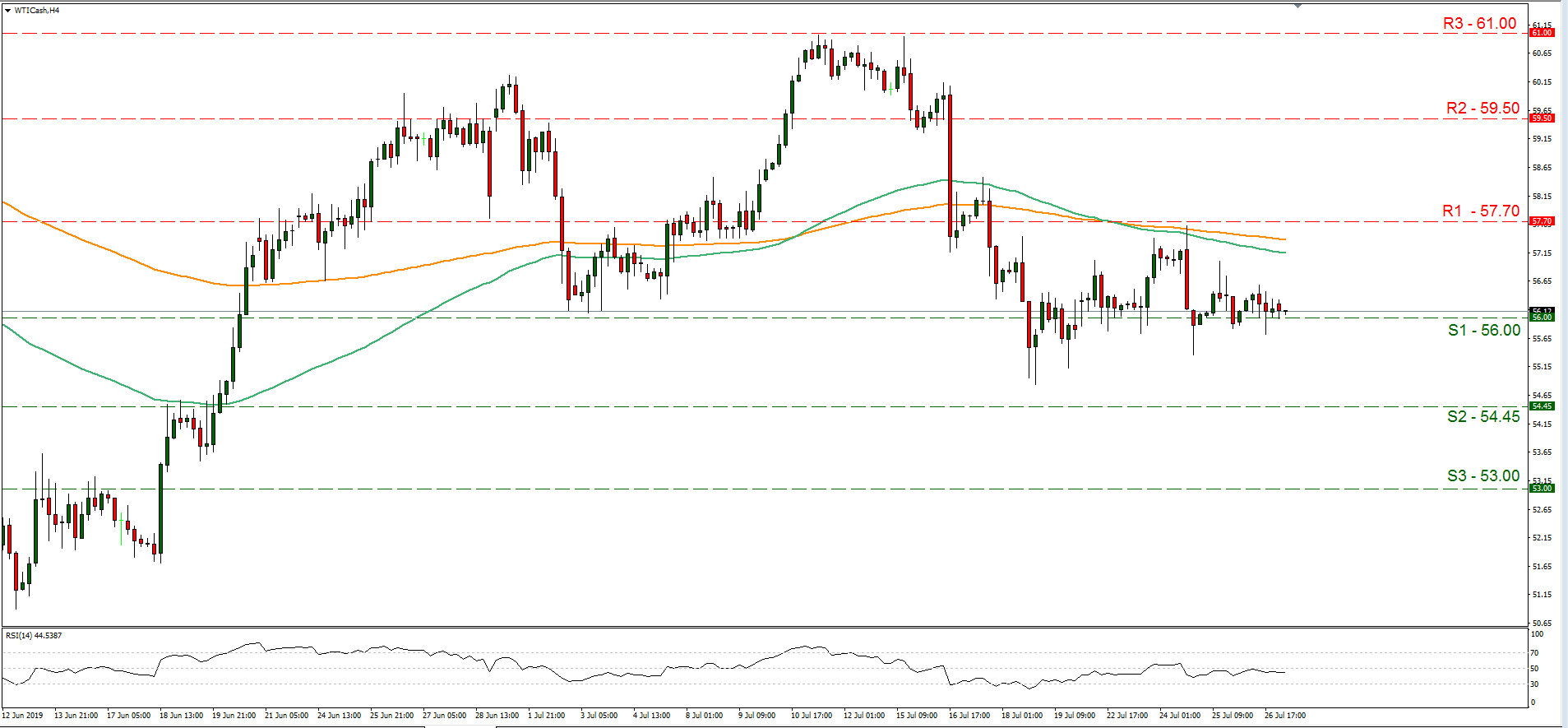

Oil prices remained rather steady despite worries seemingly easing somewhat about Iran. Iran had described emergency talks with some of the signatories of the Iran nuclear deal as constructive, easing worries somewhat. It should be noted though that there are still unresolved issues and Persia is expected to continue to reduce its commitments on its nuclear program, if European counterparts fail to strike a deal. Also, please bear in mind that tensions seem to be still ongoing near the straits of Hormuz, as the Iranians have still not released the British tanker seized. Also there seems to be an effort to form a multinational naval force to guard safe passage for shipping at the sensitive area. On another front the US-Sino negotiations are to restart and could also affect oil prices. WTI prices, maintained a rather range bound motion on Friday and today during the Asian session, comfortably supported by the 56.00 (S1) support line. Should the bears dictate the commodity’s direction, we could see it breaking the 56.00 (S1) support line and aim for the 54.45 (S2) support barrier. Should the bulls take over, we could see it breaking the 57.70 (R1) resistance line and aim for higher grounds.

Other economic highlights, today and early tomorrow

It could be a slow Monday today, yet tomorrow during the Asian session, we get BoJ’s interest rate decision. The bank is widely expected to remain on hold at -0.10%, yet the accompanying statement’s tone could be tilted to the dovish side. Should that be the case we could see the JPY slipping somewhat.

As for the rest of the week:

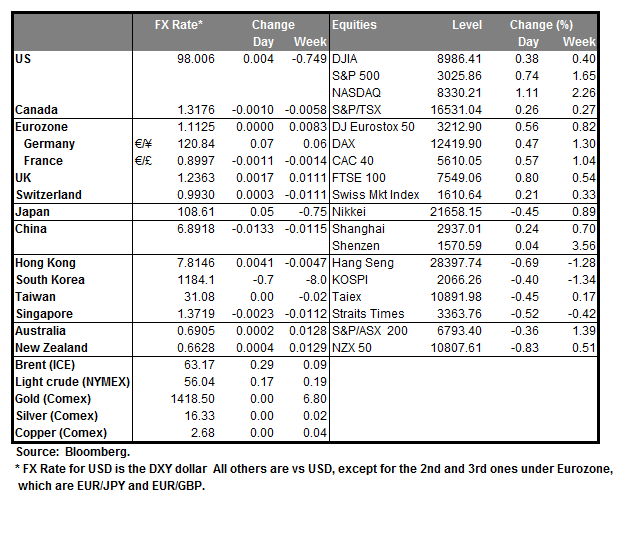

On Tuesday, Eurozone’s preliminary CPI rate for July, the US consumer confidence for July and the US Pending home sales also for July. On Wednesday, we get Australia’s CPI rate for Q2, China’s NBS Mfg PMI for July, Germany’s employment data for July and Canada’s GDP for June and the long awaited FOMC interest rate decision for the US. On Thursday, we get China’s Caixin Mfg PMI for July, from the UK BoE’s interest rate decision and form the US the ISM manufacturing PMI for July. On Friday, we get from Australia June’s retail sales growth rate, the US employment report for July, the US factory orders growth rate for June and Canada’s trade balance for June.

EUR/USD H4

• Support: 1.1100 (S1), 1.1060 (S2), 1.1020 (S3)

• Resistance: 1.1140 (R1), 1.1180 (R2), 1.1220 (R3)

WTI H4

• Support: 56.00 (S1), 54.45 (S2), 53.00 (S3)

• Resistance: 57.70 (R1), 59.50 (R2), 61.00 (R3)