Daily Commentary | 08/11/2018

RBNZ remains on hold, but slightly more hawkish

RBNZ remained on hold at +1.75%, as was widely expected yesterday, however sounded a bit more hawkish in the accompanying statement. The bank moved the next possible rate hike a bit earlier in Q2 2020, as it forecasted the average official cash rate at +1.81% in that period. The statement also indicated that the CPI remains below the 2.00% yoy midpoint and necessitates continued supportive monetary policy. The bank noted that ongoing trade tensions are increasing risks to global growth and also stated that the GDP growth rate is expected to pick up over 2019. After the interest rate decision, the Kiwi could return to being influenced by the US-Sino trade war as well as data driven.

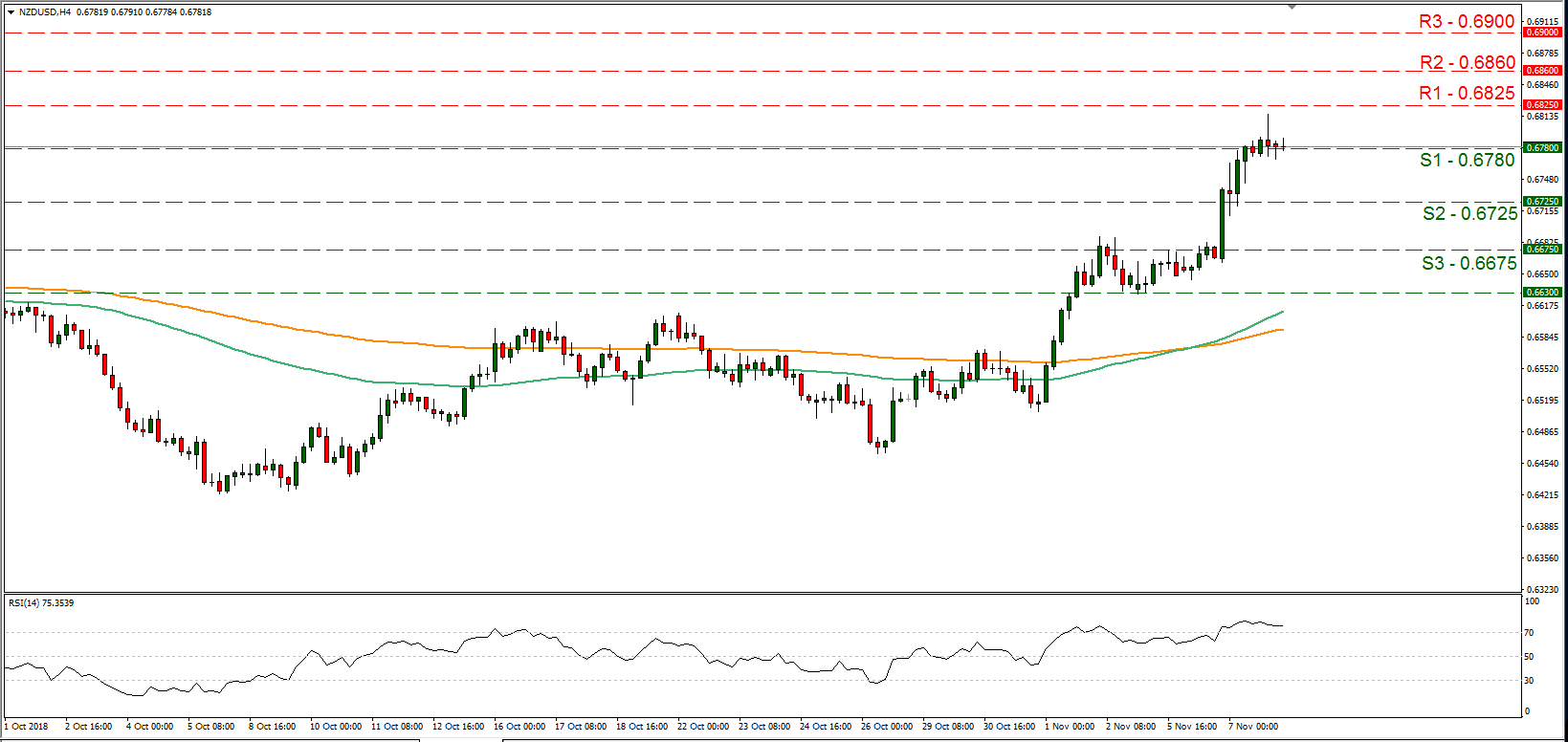

NZD/USD rose yesterday, breaking the 0.6780 (S1) resistance line (now turned to support). We could see the pair stabilising today and present some bearish tendencies as the USD side may start strengthening ahead of the FOMC interest rate decision. Please be advised that the RSI indicator remains above the reading of 70 in the 4 hour chart, insisting to point out the possibility of an overcrowded long position for the pair. Should the pair find fresh buying orders along its path we could see it breaking the 0.6825 (R1) resistance line, while if it comes under the selling interest of the market, we could see it breaking the 0.6780 (S1) support line and aim for the 0.6725 (S2) support barrier.

FOMC Interest rate decision

The FOMC is widely expected to remain on hold today (19:00 GMT), keeping Fed Funds Target rate at +2.25%. Currently, Fed’s Funds Futures imply a probability of 94.2% for the bank to maintain rates at their current level. Should the bank remain on hold as expected, the market’s attention could turn to the accompanying statement in the absence of any new forecasts and a following press conference. The recent acceleration of average earnings for October at +3.1% yoy, the unchanged record low unemployment rate of 3.7% and the increase of the non-farm payrolls figure to 250,000 from previous figure of 134,000, show a tight labour market, while the inflation rate still remains above the bank’s target of +2.00% yoy. It should also be mentioned that the GDP growth’s preliminary release for Q3 outperformed expectations, despite the slowdown if compared to Q2. Overall the US economy remains on a solid footing, which supports the bank’s current rate hike path. The recent turmoil of the stock-markets could leave the FOMC unaffected and the same applies for any comments made by US president Trump. Based on the previous analysis, we see the case for the bank to have a more hawkish tone in the accompanying statement which could provide support for the USD. Please be advised that venue may have market moving effects and increased volatility could be present for USD pairs at the time of the announcement.

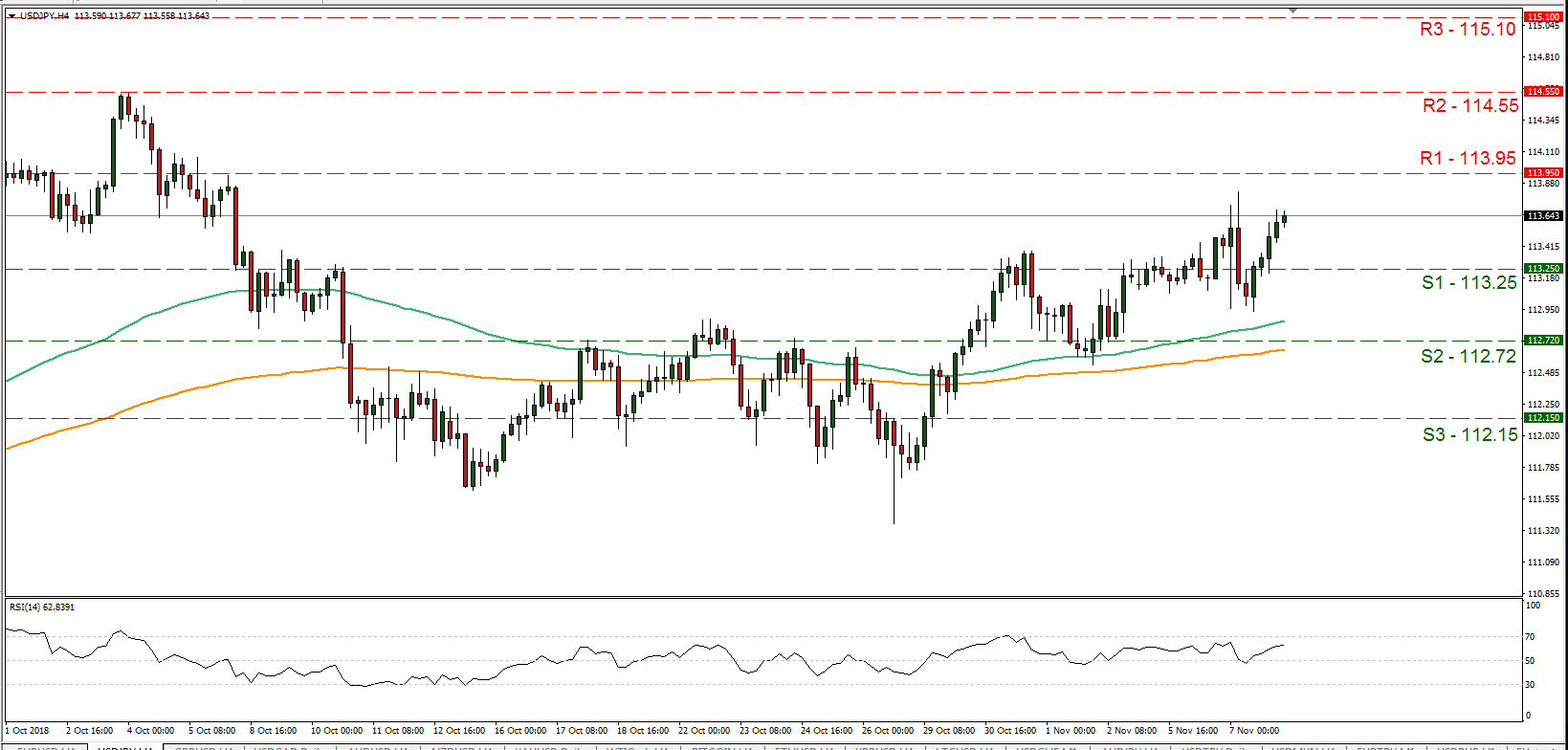

USD/JPY rose yesterday and during today’s Asian session, clearly breaking the 113.25 (S1) resistance line (now turned to support).We could see the pair continuing to trade in a bullish market as the USD side could strengthen ahead of the release of the FOMC interest rate decision today. Should the pair’s direction continue to be dictated by the bulls, we could see it breaking the 113.95 (R1) resistance line, while if the bears take over, we could see it breaking the 113.25 (S1) support line and aim for the 112.72 (S2) support zone.

In today’s other economic highlights:

In a rather quite Thursday, in the European session, we get Germany’s trade balance figure for September and from the Eurozone ECB’s economic bulletin will be released. As for speakers please note that ECB’s Benoit Coeure will be speaking today.

NZD/USD H4

Support: 0.6780 (S1), 0.6725 (S2), 0.6675 (S3)

Resistance: 0.6825 (R1), 0.6860 (R2), 0.6900 (R3)

USD/JPY 4H

Support: 113.25 (S1), 112.72 (S2), 112.15 (S3)

Resistance: 113.95 (R1), 114.55 (R2), 115.10 (R3)