Daily Commentary | Trump’s inauguration: A second wind for the USD rally, or further correction? | 20/01/17

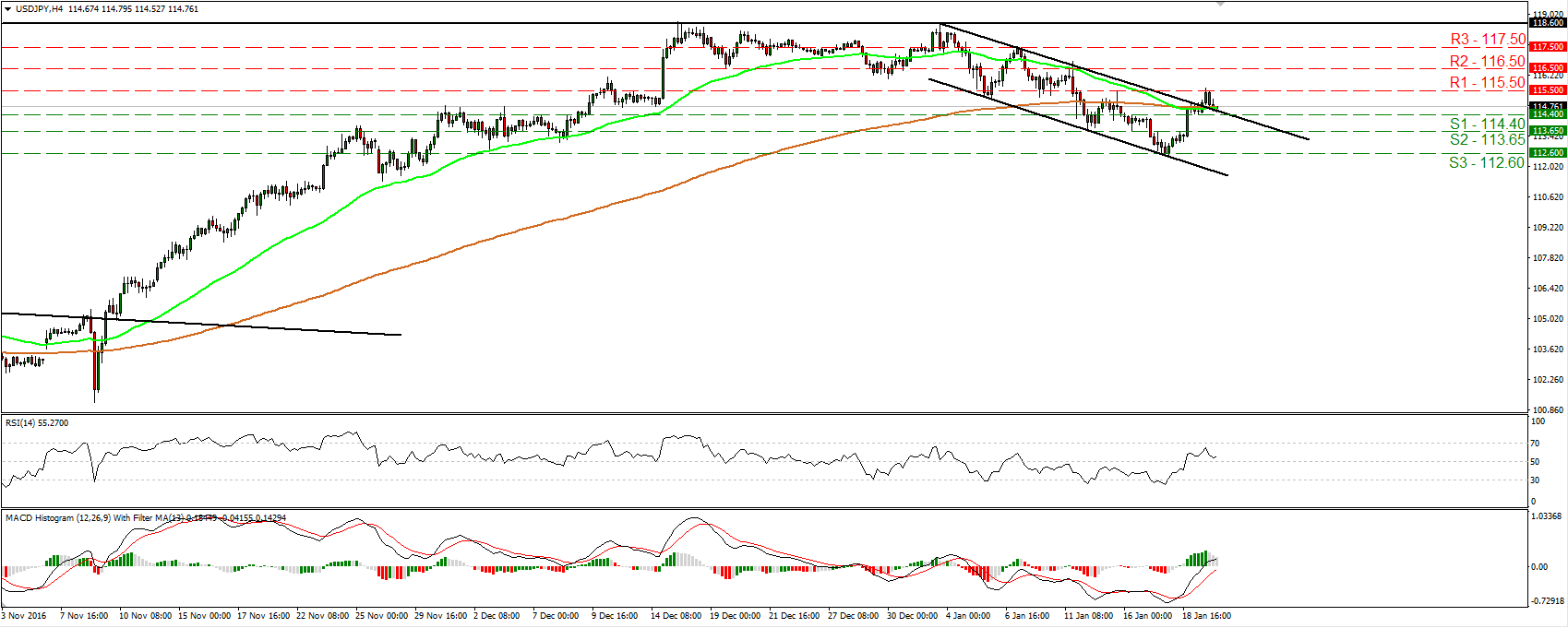

Daily Commentary • Trump’s inauguration: A second wind for the USD rally, or further correction? Today, all eyes will be turned to the US for the inauguration of Donald Trump as the 45th President. His latest press conference was somewhat disappointing, as he revealed nothing new regarding his upcoming fiscal or regulatory policies, something that led to a notable correction lower in USD. Given this lack of clarity, we expect investors to be on the lookout for any comments on these two key subjects once again. A confirmation that he plans to follow through with his pre-election rhetoric and push massive fiscal stimulus through Congress, as well as easing regulatory burdens, could reignite the post-election USD rally. Yesterday, USD/JPY broke above the upper bound of the downside channel that has been containing the price action since the 3rd of January. Nevertheless, the rate hit resistance near the 115.50 (R1) barrier, and then it retreated to test that bound as a support this time. If the bulls take advantage of that bound acting as a support, we would expect them to aim for another test near 115.50 (R1). A break above that hurdle could turn the short-term outlook back to the upside and perhaps open the way for the 116.50 (R2) resistance.

• On the other hand, if Trump avoids the crucial topics of fiscal and regulatory reforms once again, or if his stance towards them seems less confident than pre-election, USD could resume its downward correction, as investors become increasingly impatient regarding the absence of details on the nation’s fiscal direction. In this case, USD/JPY may return within the aforementioned downside channel and is possible to challenge the 112.60 (S3) support, marked by the low of the 18th of January.

• Our view is that at some point the incoming President will have to discuss these hot subjects and we see the inauguration as the ideal occasion. Even if he does not dig into details, such as the size and composition of any fiscal package, we consider it likely that we get some comments on these economic issues, though the tone he delivers them in will probably be vital for the dollar’s near-term performance.

• ECB remains ultra-dovish despite higher headline CPI The European Central Bank kept its stimulus program unchanged yesterday, as was widely expected, and was very dovish with regards to inflation. Even though December’s headline CPI rate surged to a level last seen in 2013, President Draghi downplayed the importance of that improvement by pointing out that he sees no convincing upward trend in underlying inflation, and that the latest progress in the CPI is mainly due to energy-related effects. Perhaps most importantly, the Governing Council indicated that it will continue to look through changes in headline inflation if they are judged to be transient, suggesting that the officials may focus primarily on underlying inflation in the future. Thus, we expect the bloc’s core CPI rate to attract much more market attention than previously. Furthermore, the Bank said that underlying inflation is expected to rise more gradually over the medium-term and that the risks surrounding Eurozone’s economy are still tilted to the downside.

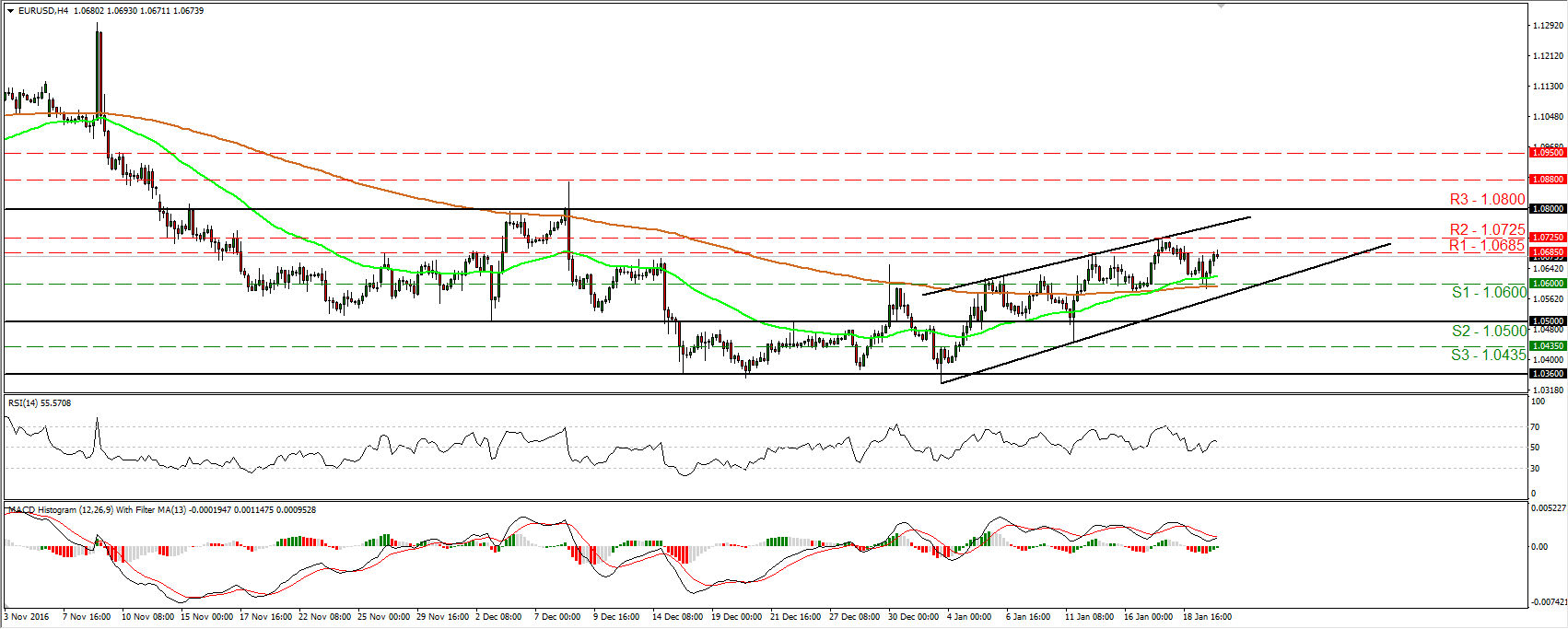

• In our view, all these signals suggest that the ECB will maintain its ultra-loose policy stance intact in the foreseeable future and that it is still far too early for investors to begin betting on the possibility of any ECB tapering. As a result of these dovish hints, EUR/USD tumbled, but hit support near 1.0600 (S1) and rebounded in the aftermath of Draghi’s conference. Now, the pair is testing the 1.0685 (R1) territory. The short-term trend remains positive in our view and as such, we would expect the rate to continue higher for a while, at least heading into Donald Trump’s inauguration. We believe that the bulls may aim for the 1.0725 (R2) barrier soon, where a break is possible to open the way for the key obstacle of 1.0800 (R3).

• Moving forward, the pair’s near-term direction will probably be decided by the rhetoric that incoming US President Trump will deliver today. But in the medium-term, we remain sceptical regarding a sustained rally in EUR/USD. We believe that the dynamics of monetary policy divergence, as well as the upcoming political risks in the Eurozone, are likely to keep any rallies in the pair somewhat limited in the foreseeable future. The price structure on the daily chart remains lower peaks and lower troughs, supporting our view. We will continue to treat the pair’s recent recovery, or any extensions that stay limited below 1.0800 (R3), as a corrective phase.

• As for the rest of today’s highlights: From the UK, we get retail sales for December. The forecast is for both the headline and the core rates to have declined, a turnaround from the previous month. Even though such a decline may bring GBP under renewed selling interest, considering the strength of retail sales in November and October, we doubt that a minor decline in December will change the BoE’s upbeat stance on the economy.

• From Canada, we get CPI data for December. The forecast is for both the headline and the core CPI rates to have risen, a rebound from November. The case for accelerating inflationary pressures is supported by the nation’s manufacturing PMI for the month, which showed that output inflation reached its fastest pace since May 2014. Coming on top of the nation’s employment figures for the month, which overshot expectations and improved significantly, we believe that a potential rebound in the CPI rates is likely to be another piece of evidence supporting no policy action by the BoC in coming months. As such, this could reverse some of CAD’s recent losses.

• Besides incoming US President Trump, we have one more speaker scheduled for Friday: Philadelphia Fed President Patrick Harker.