Daily Commentary | 26/06/2017

Canada’s CPIs slow, drag the Loonie down

• The Canadian dollar took a hit on Friday, following the release of Canada’s CPI figures for May. Both the headline and the core rates declined notably, with the core falling for the 3rd consecutive month and reaching its lowest level since 2011. The soft readings probably poured cold water on recent speculation regarding a more hawkish stance by the BoC soon, which arose after Deputy Governor Wilkins noted that the Bank will assess whether all the monetary stimulus currently in place is still needed.

• Having said this though, we remain somewhat optimistic on the Loonie’s short-term outlook, despite slowing inflation. Canada’s broader economy remains solid, as the labor market continues to tighten, while there are signs that Q2 GDP growth may be stronger than previously expected. In addition, there is the prospect for a rebound in oil prices, following several weeks of declines and rising political tensions in the Middle East between Saudi Arabia and Qatar, which increase the risk of supply disruptions in the near-future.

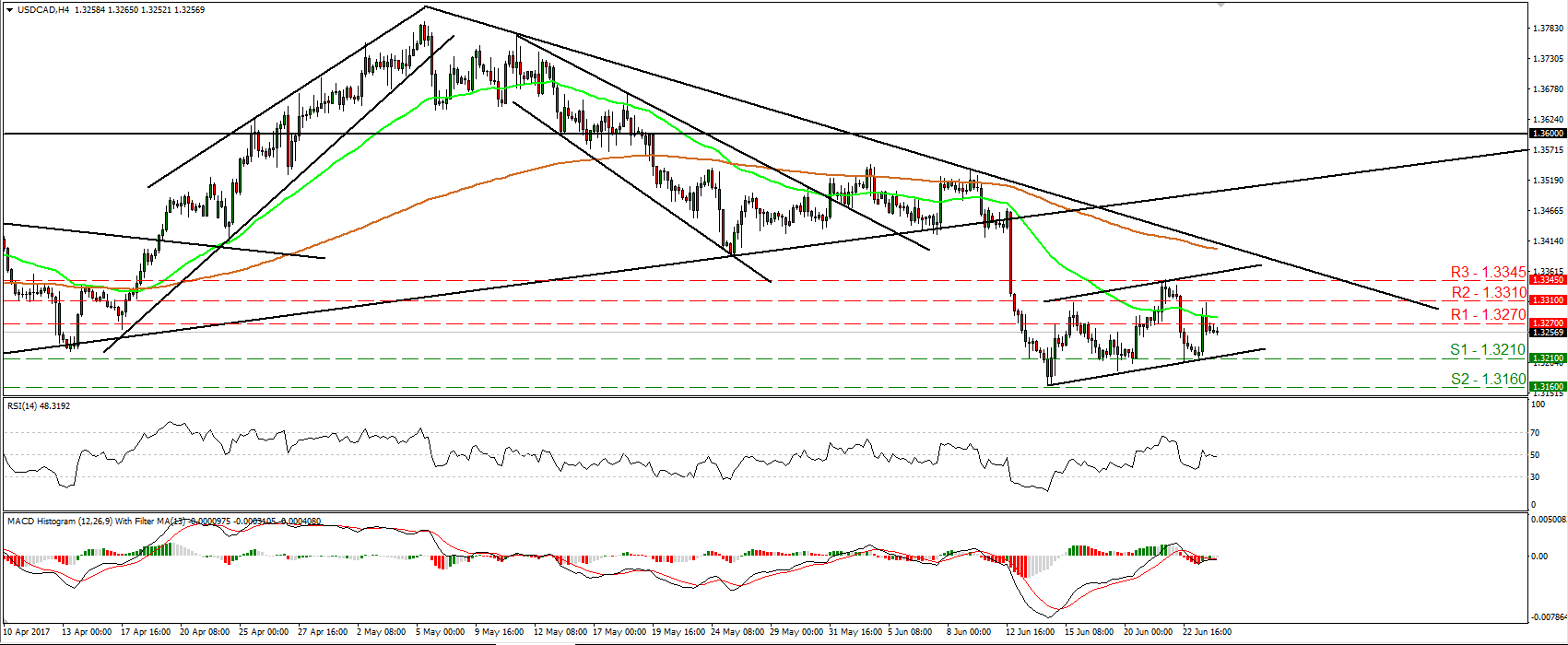

• USD/CAD edged north on Friday after the slide in Canada’s inflation rates. The pair rebounded from the lower bound of the flag formation that has been containing the price action since the 14th of June, so we prefer to stay neutral for now. However, given that the rate is still trading below the downtrend line taken from the peak of the 11th of May, we believe that the prevailing short-term trend remains cautiously to the downside. A clear break below the crossroad of 1.3210 (S1) and the lower bound of the flag could signal the continuation of that trend and could initially aim for our next support of 1.3160 (S2), marked by the low of the 14th of June. Another dip below the latter level will confirm a forthcoming lower low and may open the way for the 1.3080 (S3) obstacle, a support defined by the low of the 27th of February.

Today’s highlights:

• During the European day, we get Germany’s Ifo survey for June. Expectations are for an uptick in the current conditions index and a downtick in the expectations figure. Nonetheless, even if the expectations index comes down slightly, we don’t expect that to be particularly worrisome for ECB policymakers, considering that the composite Ifo index reached a fresh all-time high in May.

• In the US, durable goods orders for May are coming out. The forecast is for headline orders to have fallen again, but at a slower pace than previously, while the core rate that excludes transportation equipment is expected to have turned positive. The New Orders sub-index of the ISM manufacturing PMI showed a rebound in the month, which supports the core forecast. We believe that investors may focus primarily on the core print, which excludes volatile items. Thus, a potential rebound in core orders may bring the greenback under renewed buying interest.

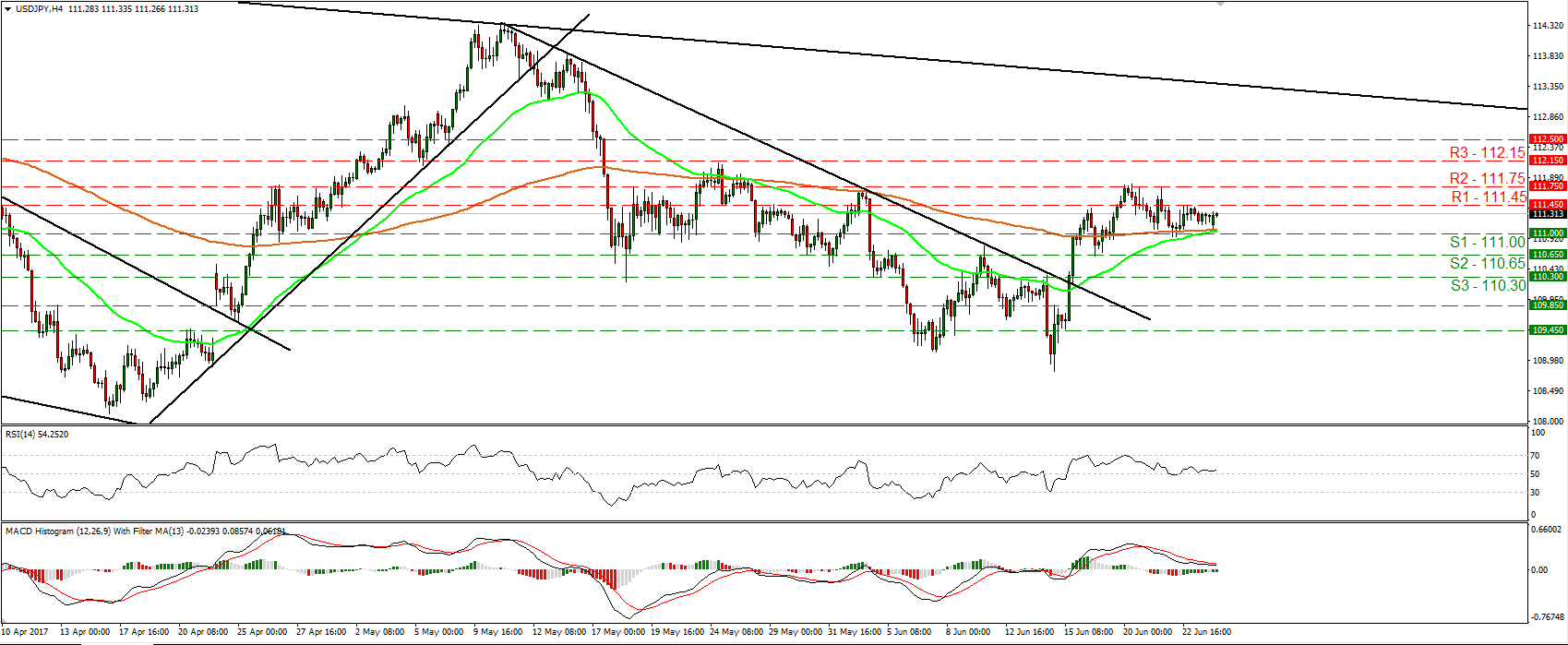

• USD/JPY has been trading in a quiet mode since the 22nd of June, staying between the 111.00 (S1) and 111.45 (R1) barriers. However, despite the recent trendless action, the rate continues to trade above the prior downtrend line drawn from the peak of the 10th of May. Therefore, we remain cautiously optimistic on the pair and we expect the bulls to take the reins again soon. A break above 111.45 (R1) could target the 111.75 (R2) hurdle first. Another break above 111.75 (R2) could set the stage for the 112.15 (R3) zone.

As for the rest of the week:

• On Tuesday, the only event that could attract some attention is a speech by Fed Chair Yellen that will focus on global economic issues. On Wednesday, we have a relatively quiet day with nothing major on the agenda, while on Thursday, the UK Parliament is expected to vote on the Queen’s Speech. We think that the vote could keep investors on the edge of their seats, as it will determine whether May keeps her position as the UK PM. As for the economic indicators, we get Germany’s preliminary CPI data for June. Finally on Friday, during the Asian morning, we get Japan’s CPI data for May and China’s official manufacturing and non-manufacturing PMIs for June. In Eurozone, preliminary CPI data for June are due out, while from the US, we get personal income, personal spending, as well as the core PCE price index, all for May.

USD/CAD

• Support: 1.3210 (S1), 1.3160 (S2), 1.3080 (S3)

• Resistance: 1.3270 (R1), 1.3310 (R2), 1.3345 (R3)

USD/JPY

• Support: 111.00 (S1), 110.65 (S2), 110.30 (S3)

• Resistance: 111.45 (R1), 111.75 (R2), 112.15 (R3)