The central bank torch is passed to the Bank of Canada | 07/12/16

• The central bank torch is passed to the Bank of Canada The highlight on today’s agenda is the BoC monetary policy gathering. Expectations are for the Bank to hold its fire at this meeting. We agree amid mixed Canadian economic data. The BoC struck a somewhat neutral tone the last time it gathered, an upgrade from its previously dovish stance. However, in the press conference following the decision, Governor Poloz backpedaled on the Bank’s neutral outlook, by indicating that policymakers actively discussed the possibility of adding more monetary stimulus at that gathering. Since then, economic indicators have painted a mixed picture of the economy. Although the labor market tightened in October and GDP growth was stronger than expected in Q3, the nation’s core CPI rate slipped in October, while its current account deficit widened in Q3. Poloz said in recent comments that the current account balance was likely to clear the Bank’s outlook and as such, these data could warrant a shift back to a dovish stance by the Bank, if viewed in isolation. However, this is not our base-case scenario. We believe that BoC officials are likely to be content with the OPEC meeting outcome and the subsequent surge in oil prices, considering Canada’s heavy dependence on oil exports. Thus, we expect the Bank to maintain its somewhat neutral tone in its policy statement, especially considering that the latest gains in oil prices and the optimism in the energy market may be sustained for a while.

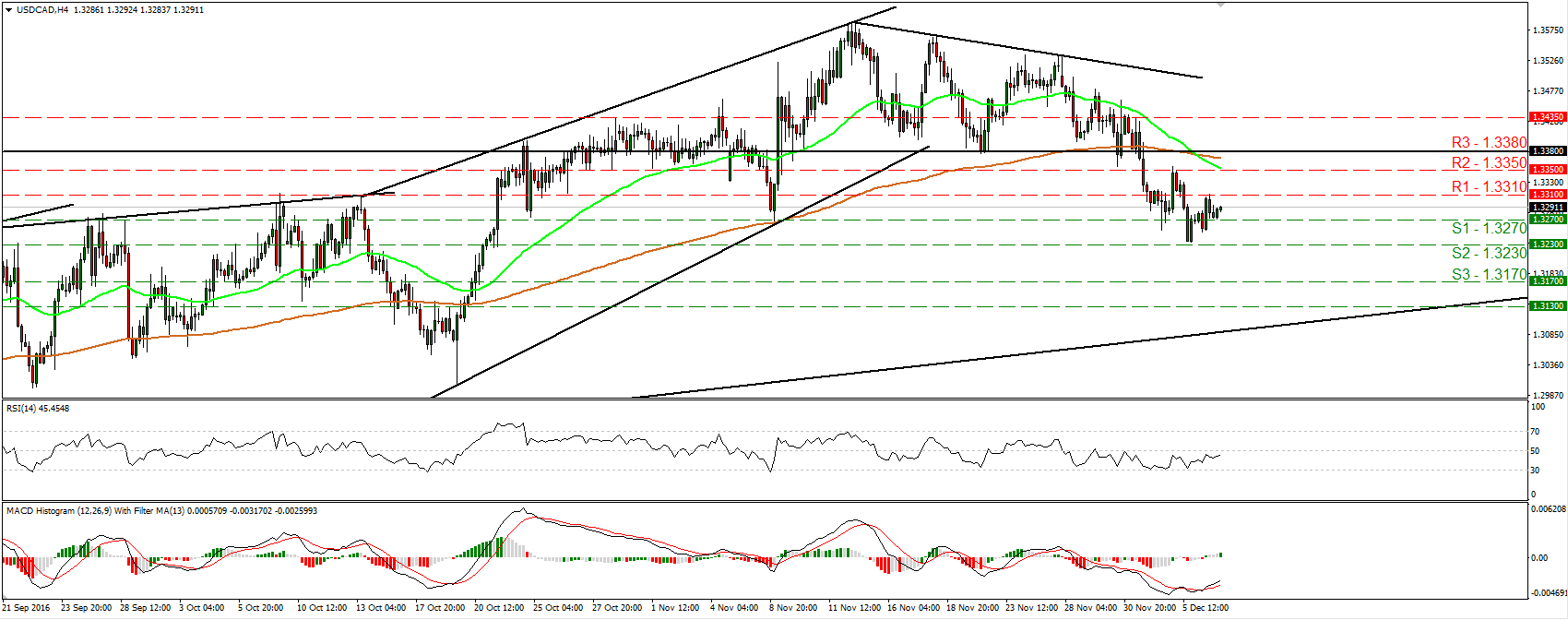

• USD/CAD has been in a short-term downtrend following the downside exit of a descending triangle that had been containing the price action from the 9th of November until the 1st of December. During the European morning, USD/CAD is trading slightly above the 1.3270 (S1) support level, and some optimistic points in today’s statement may trigger a break. Something like that may initially aim for the next obstacle of 1.3230 (S2) and if the bears are strong enough to overcome it, we would expect them to set the stage for extensions towards the 1.3170 (S3) territory.

• Overnight: During the Asian morning Wednesday, Australia’s GDP for Q3 came at -0.5% qoq from +0.5% qoq the previous quarter, missing estimates of a slowdown to +0.3% qoq. The nation’s economy probably shrank as businesses, consumers and the government, all scaled back spending throughout the quarter. This was the largest contraction for the Australian economy since 2008 and threatens both the first recession in a quarter of a century and the country’s triple-A credit rating. The SnP Global rating agency has warned several times that there is the likelihood to downgrade Australia if the government’s promises for a surplus by 2020 were to slip again. As a result, this figure is a headache for the government as it may prompt a greater fiscal response and thereby, delay the budget getting into surplus. What is more, the danger of a recession may force the RBA to alter its plans. Yesterday, at its latest meeting for the year, the Bank once again gave no signals on whether it plans to ease again in the foreseeable future, and judged that by keeping rates unchanged there are reasonable prospects for achieving sustainable growth.

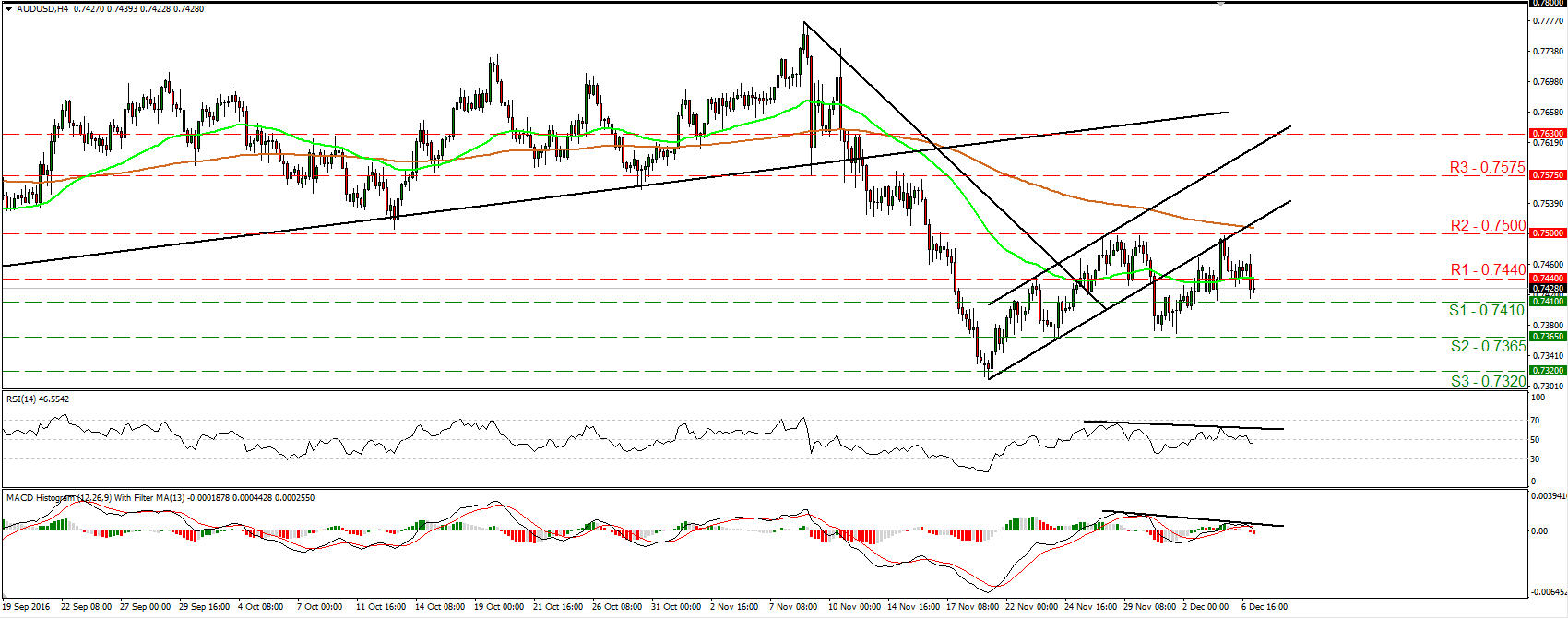

• The Aussie slid on the bad GDP figure and given that this lit the spark of speculation that Bank may consider taking action at its upcoming meetings, we would expect AUD/USD to continue trading lower, at least in the near term. The pair fell below the support (now turned into resistance barrier) of 0.7440 (R1) and stopped marginally above the 0.7410 (S1) line. A break below the latter level is possible to aim for the next key hurdle of 0.7365 (S2). However, we stick to our guns and we believe that Aussie will not move in a similar fashion against all its counterparts. For example, we still expect it to outperform the yen, especially following the overnight comments by the BoJ Deputy Governor that the Bank won’t hesitate to take additional easing steps if needed. As such, we would treat the overnight slide in AUD/JPY as a corrective setback.

• As for the rest of today’s events: The European day begins with Germany’s industrial production for October and expectations are for a decent rebound following the previous month’s slide. Coming on top of the spectacular increase in factory orders for the month, this would add to evidence that Eurozone’s growth engine is gaining steam.

• We get October industrial production data from the UK as well. The consensus is for a minor rebound, following a modest decline in September. However, given the slide in the manufacturing PMI for the month, we remain sceptical on whether IP could meet its forecast. A miss is possible to hurt somewhat the pound. Nevertheless, bearing in mind that the pound has been gaining ground lately on “soft Brexit” comments, we would treat any possible slide at this release as providing renewed buying opportunities.

• No speakers are scheduled on Wednesday’s agenda.