Politics take center stage again: Italian referendum | 02/12/16

• Politics take center stage again: Italian referendum The next political risk event that is likely to rattle financial markets is the Italian Constitutional referendum on Sunday. Italy’s PM Renzi is calling his citizens to decide on constitutional changes aimed at accelerating the pace of reforms and making Italian governments more stable, primarily by stripping the Senate of many of its powers and transferring them to the government.

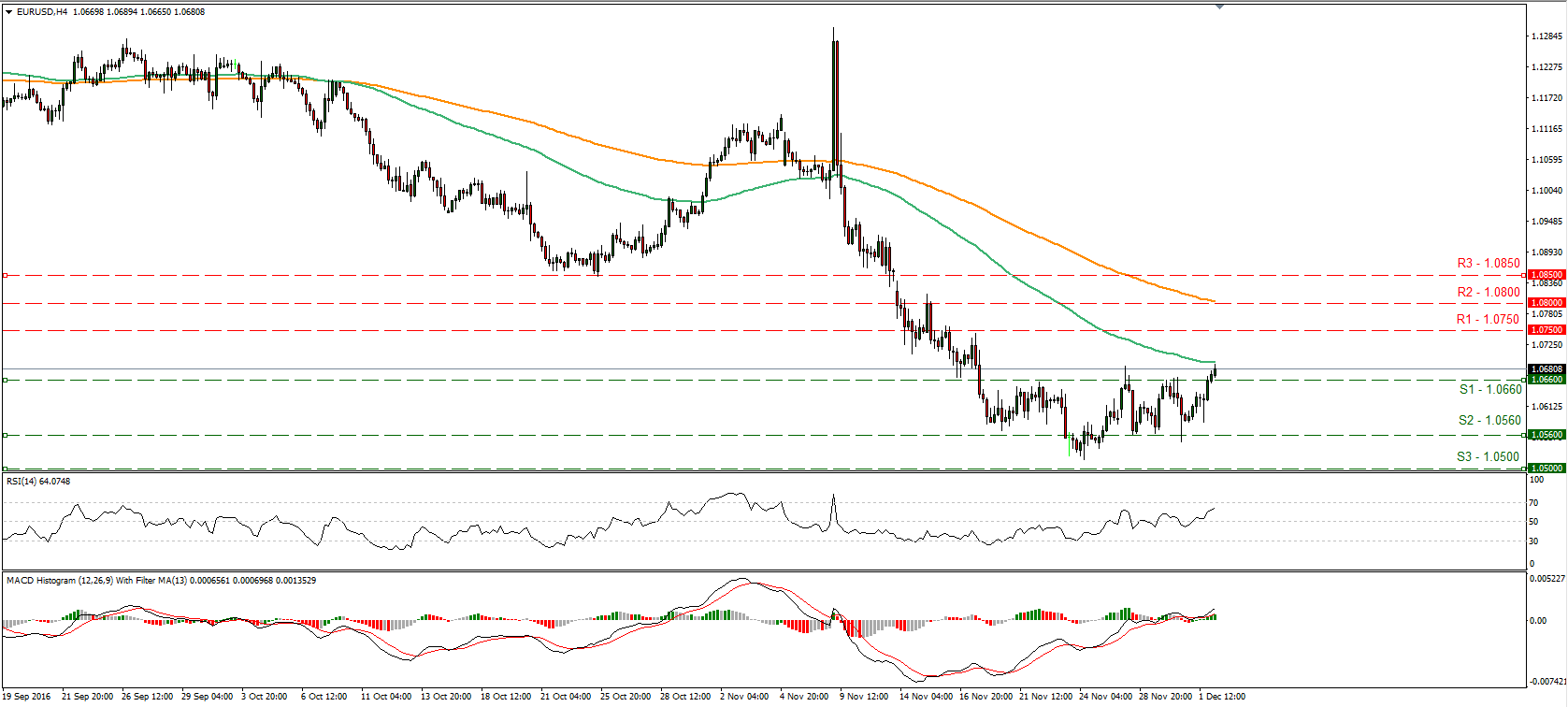

• If the Italian people decline Renzi’s proposals, he pledged to step down. So in such a case, political uncertainty is likely to mount and generate fresh questions regarding the nation’s stability, and by extension the Eurozone’s sustainability. If indeed Renzi quits, one of the prominent parties that could rise to power is the Five Star Movement, a political party that is considered anti-establishment, and has in the past advocated for holding a referendum on the euro. This is likely to impact confidence in the Italian economy and in its troubled banking system, something that could negatively impact the euro, as well as the Italian and Eurozone banking shares. Such an outcome is possible to be the trigger for EUR/USD to move back below the 1.0660 (S1) barrier, and if the bears are strong enough, they may be able to push the rate lower towards the 1.0560 (S2) hurdle again.

• If on the other hand Renzi remains in place, the status quo would be more or less maintained, which implies that uncertainty would be much less. Therefore, any adverse market reaction in EUR and bank equities could be smaller. Now, in case Italians accept these reforms, confidence over increasing stability in Eurozone’s 3rd largest economy is likely to rise. This could spell good news for the bloc and the common currency. A clear break in EUR/USD above 1.0750 (R1) may set the stage for larger bullish extensions and aim for the key zone of 1.0800 (R2).

• NFP to seal the deal for a December Fed hike Today, the main event will be the US employment report for November. Nonfarm payrolls are expected to have risen by 174k, more than October’s 161k. The fact that the ADP employment change for November came at 216k, significantly above its forecast, and the overall low initial jobless claims throughout the month, suggest that we could even see a higher-than-expected NFP figure. The unemployment rate is forecast to have remained unchanged at 4.9%, while average hourly earnings are expected to have slowed on a monthly basis. Despite the slowdown in earnings, the forecasts point to another month of solid employment gains overall, which may seal the case for a Fed hike at the upcoming gathering in December and thereby cause the dollar to add to its gains.

• At the November gathering, FOMC officials signaled that the case for a rate hike has continued to strengthen and that they are very likely to take action in December should the data hold up. Since that meeting, most US economic indicators have painted an upbeat picture of the economy, while Trump’s victory led investors to price in much higher inflation due to expectations of fiscal stimulus. Evident by the surge in 5-year inflation expectations, as well as Treasury yields. The market is now pricing in a 98% chance for a December hike according to the Fed funds futures. As such, we believe that at the December meeting investors will have their eyes locked on the policy statement and the updated “dot plot”, in order to get up-to-date forward guidance that reflects the aforementioned changes in financial conditions.

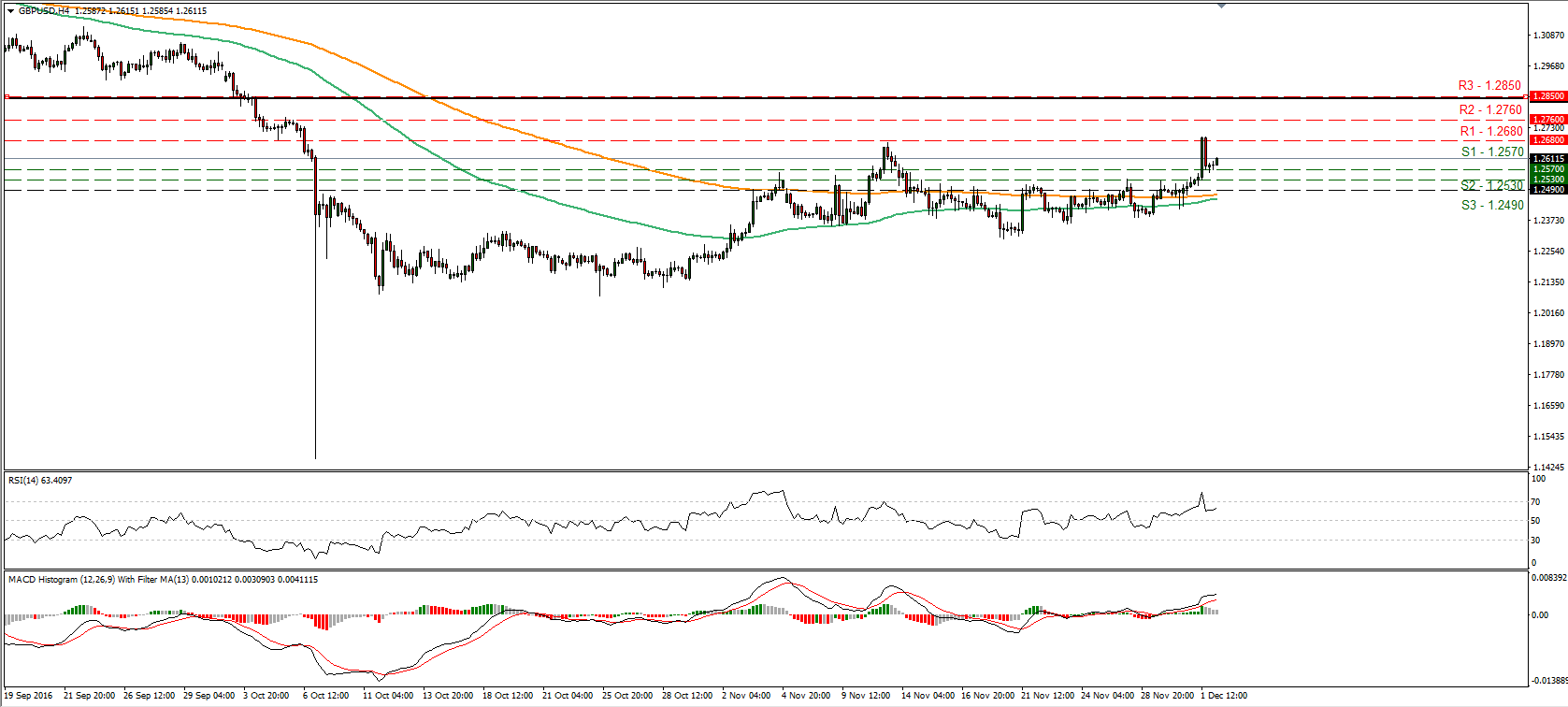

• GBP surges on “soft Brexit” comments The British pound surged yesterday, following comments from UK Brexit Minister David Davis and the head of the Eurogroup, Jeroen Dijsselbloem. The initial spike higher in Cable came from Davis’s remarks, who told lawmakers that Britain would consider making payments to the EU after it leaves, in order to achieve the best possible access to the bloc's markets. These comments may have diminished somewhat the likelihood for a “hard Brexit”, and caused GBP/USD to break above two resistance (now turned into support) barriers in a row, the 1.2530 (S2) level and subsequently, the 1.2570 (S1) zone. Dijsselbloem added fuel to the rally by indicating that the EU may be able to find ways for the UK to access the EU market even post-Brexit. This triggered larger bullish extensions in Cable, with the rate hitting resistance slightly above the 1.2680 (R1) before retreating somewhat. Given these “soft Brexit” signals and that the short-term trend of GBP/USD appears to be positive, we would expect the rate to continue higher and test the 1.2680 (R1) hurdle again. A clear break of that zone could initially aim for the 1.2760 (R2) level. However, given that we have the US employment report today and expectations are for another month of solid jobs gains, we could see some further pullback in the pair before the next leg higher.

• As for the rest of today’s highlights: During the European day, the UK construction PMI for November is due out and expectations are for a modest decline in the index. Coming on top of a similar decline in the manufacturing PMI for the month, this could diminish some optimism over the UK’s economic performance after the referendum, and may thereby hurt the pound somewhat.

• From Canada, we also get November’s employment data. The forecast is for the unemployment rate to have held steady, but for the net change in employment to have turned negative. Given also that the US and Canadian jobs reports are released at the same time and former is expected to be solid while the latter soft, USD/CAD could surge on the news. However, even though this appears like a very soft month for the labor market, we would like to note that in October the jobs market tightened significantly. Considering the volatility of employment indicators on a monthly basis, some softness in November appears more than normal to us, and we don’t expect that to significantly alter the view of the BoC on the economy. What’s more, given the outcome of the OPEC meeting and the subsequent surge in oil prices, we believe that the Bank will be somewhat content, given the nation’s high dependence on oil exports.

• We have two speakers on today’s agenda: Cleveland Fed President Loretta Mester and Dallas Fed President Robert Kaplan.