IronFX Daily Commentary | 26/10/15

• China’s ruling Communist Party opened a key four day meeting. China’s ruling Communist Party opened a key four day meeting today that will focus on economic and social targets for the next five year. Following the soft GDP data for Q3, the Peoples Bank of China (PBoC) cut interest rates for the sixth time in less than a year on Friday, to support the slowing economy. It also lowered the reserve requirement ratio (RRR) and unbounded the interest rate market by removing the ceiling on deposit rates. The latter will allow the banks to price loans according to their risk. The next five-year plan is likely to reduce the GDP target to around 6.5%, and continue to shift to a more sustainable growth model focused on consumption. Already government officials downplayed the existing economic growth target, which raised expectations for a “new normal” of slower growth. A slower growth is likely to weigh on Australia and New Zealand, whose economies are heavily dependent on exports to China. AUD and NZD could come under selling pressure, but much will depend on what will be the measures the Chinese government will take to maintain that growth range.

• Today’s highlights: We have a relatively light calendar. The most important indicator we get is the German Ifo survey for October. Both the ZEW indices for the month declined sharply as the Volkswagen scandal coupled with the weak growth in EM deteriorated the economic outlook for Germany. Expectations are for all three Ifo Indices to decline as well, something that could put EUR under renewed selling pressure.

• In the US, we get new home sales for September and expectations are for a modest decline. However, following the improvement in existing home sales, housing starts and building permits for the same month, I don’t expect new home sales to change investors’ view over the strength of the US housing sector. We could even see a positive surprise, something that could boost the greenback somewhat. The Dallas Fed manufacturing activity index is also to be released.

• Only one speaker is scheduled on Monday: ECB Executive Board Member Yves Mersch.

• As for the rest of the week, we have a very eventful week ahead of us with several central bank meetings, including US Fed, as well as important economic indicators. The spotlight will be the FOMC monetary policy meeting on Wednesday. At their last meeting, Fed officials decided to remain on hold, as the market had expected, but surprised investors with a very dovish outlook. They lowered their inflation forecasts and lowered their median forecasts for end-year Fed funds by 25 bps for end-2015, 2016 and 2017. Moreover, they do not see core inflation moving back up to their 2% target until 2018, which means probably that even when they do start hiking rates, they will only hike slowly and perhaps stop at a lower rate than expected. What is more, the Committee did discuss the idea of hiking rates at this meeting, but decided not to because of global factors. With no press conference scheduled or new forecast available at this meeting, the focus will be on the statement accompanying the decision. Even though there is a minor chance of a hike, we would expect the Committee to remain on hold and wait for signs of further improvement in the data before risking a lift-off. We expect the statement to reflect the latest weakness in job growth but this could be downplayed again as several Fed speakers did recently. We will also look through the statement to see if the majority of Fed officials still wants to hike rates this year (apparently in December, if they don’t hike this week).

• On Tuesday, the main event will be the preliminary UK GDP for Q3. The forecast is for the growth to have slowed to 0.6% qoq from 0.7% qoq. Given the strong industrial production for August and the much-better-than expected retail sales for September, we see the likelihood for a positive surprise rather than a slowdown.

• From the US, we get durable goods orders for September. The headline figure is expected to fall for a second consecutive month, while durable goods excluding transportation equipment are estimated to have remained unchanged after falling somewhat in August. The focus is usually on the core figure, where a positive surprise could suggest a possible turnaround in business investment and could support the dollar.

• On Wednesday, besides the FOMC, two more Banks gather to decide on their interest rates: the Riksbank and the Reserve Bank of New Zealand.

• At its last meeting, the Riksbank decided to leave policy unchanged and noted that the expansionary monetary policy is supporting the continued positive development of the Swedish economy. With an economy running in line with the Riksbank’s forecasts, there should be no need for further stimulus. However, as Sweden’s neighbor central banks keep a softer tone, we see a high possibility for further action this week, either additional QE or a rate cut.

• The Reserve Bank of New Zealand is expected by most forecasters to keep its cash rate unchanged at 2.75% but a minority of economists, including us, believe that another 25 bps cut could be in the works. At its last meeting, the Bank cut rates by 25 bps and Gov. Graeme Wheeler recently said that “further easing seems likely, but this will continue to depend on the emerging flow of economic data.” Since then, inflation rose a bit but still lies well below the Bank’s target range of 1%-3%. In addition, China’s slowdown keep inflationary pressures in NZ weak and could prompt the RBNZ to act again.

• On Thursday, Germany’s preliminary CPI rate for October is forecast to have risen to +0.1% yoy from -0.2% yoy in September. A rise in the inflation rate of Eurozone’s growth engine could indicate a rise in Eurozone’s rate to be released on Friday. This could support the euro temporarily, but given the more-dovish-than expected remarks by ECB President Draghi at Thursday’s meeting, we could treat any rebounds in EUR as providing renewed selling opportunities.

• In the US, we get the 1st estimate of Q3 GDP. Given the drag from net exports and slower inventory accumulation, expectations are for a significant slowdown in Q3 growth despite the solid growth in private consumption. The quarterly PCE deflator is also forecast to have slowed.

• On Friday, the Bank of Japan monetary policy meeting will take center stage. The Bank will also publish its semi-annual outlook report for the fiscal year 2016, where it is expected to cut slightly the outlook for both growth and inflation. Even though Japan’s economy shrank in Q2 and might slip back into recession, Bank officials’ could refrain from adding fresh stimulus into the economy. BoJ Gov. Kuroda and several policymakers, maintained their optimistic tone regarding the underlying trend of inflation and still expect that they will meet their 2% target. As such, many members see no immediate need to ease further, stressing that a tightening job market will lead to wage gains and boost consumption. We will need a substantial downward revision of inflation and growth forecasts for the Bank to expand its already massive QQE program.

• As for the indicators, we have the usual end-of-month data dump from Japan. However, we expect the data to pass unnoticed this time, except the CPI data, as investors’ full attention will be on the BoJ policy meeting.

• In Eurozone, the preliminary CPI rate for October is forecast to come at 0.0% yoy from -0.1% in September. This could benefit the common currency, at least temporarily, as due to the ECB’s dovish rhetoric, we remain bearish on EUR.

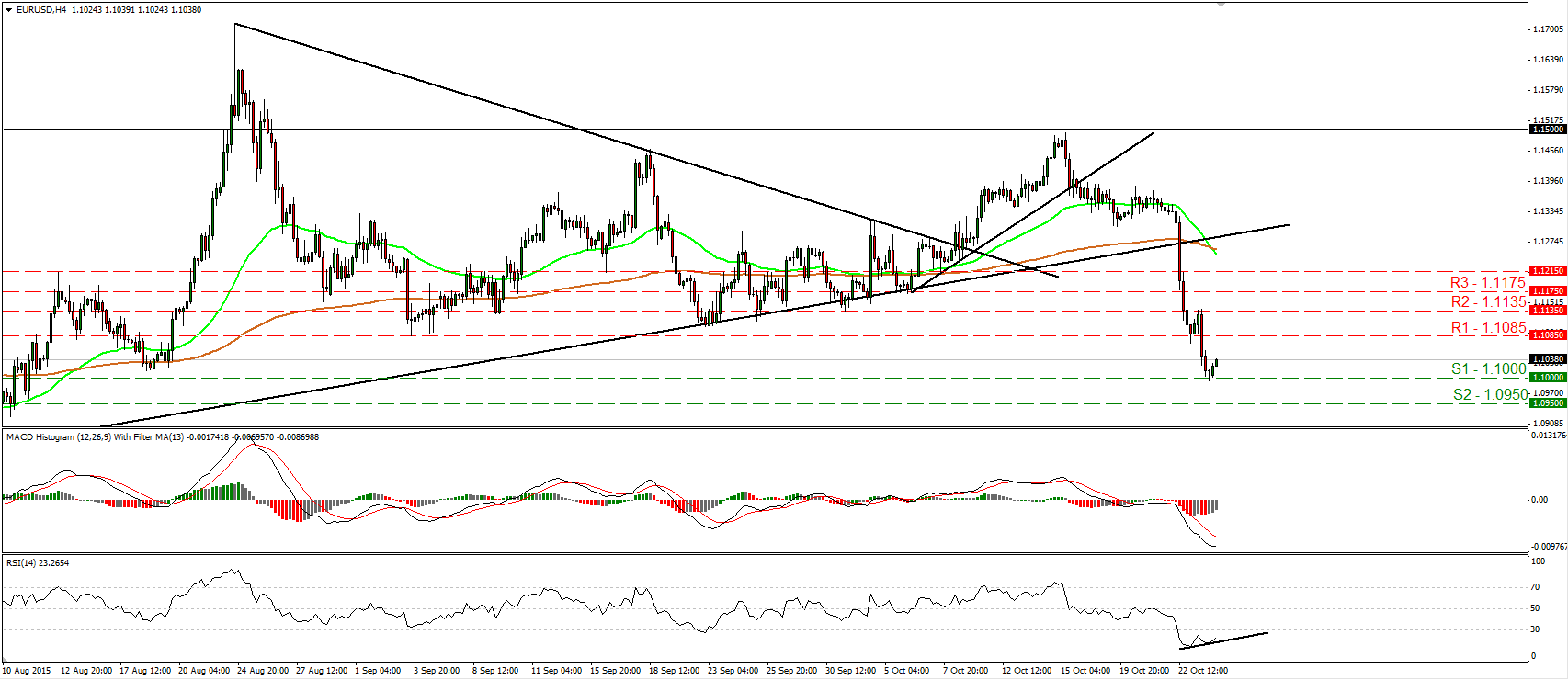

EUR/USD continues lower and hits support at 1.1000

• EUR/USD continued trading lower on Friday and managed to hit support near the psychological figure of 1.1000 (S1). Today, during the Asian morning the rate rebounded somewhat. The short-term outlook remains negative in my view and therefore, I would expect a clear break below 1.1000 (S1) to initially aim for the next support zone at around 1.0950 (S2). However, our momentum studies give evidence that further upside correction could be on the cards before sellers decide to shoot again, perhaps to challenge the 1.1085 (R1) hurdle as a resistance this time. The RSI has bottomed within its below-30 territory and is now pointing up, while the MACD, although below both its zero and trigger lines, shows signs of bottoming. What is more, there is positive divergence between the RSI and the price action. In the bigger picture, as long as EUR/USD is trading between the 1.0800 key support and the psychological zone of 1.1500, I would maintain my neutral stance as far as the overall picture is concerned. I would like to see a clear break below the 1.0800 hurdle before assuming that the longer-term trend is back to the downside. On the upside, another move above 1.1500 is needed to turn the overall outlook positive.

• Support: 1.1000 (S1), 1.0950 (S2), 1.0860 (S3)

• Resistance: 1.1085 (R1), 1.1135 (R2), 1.1175 (R3)

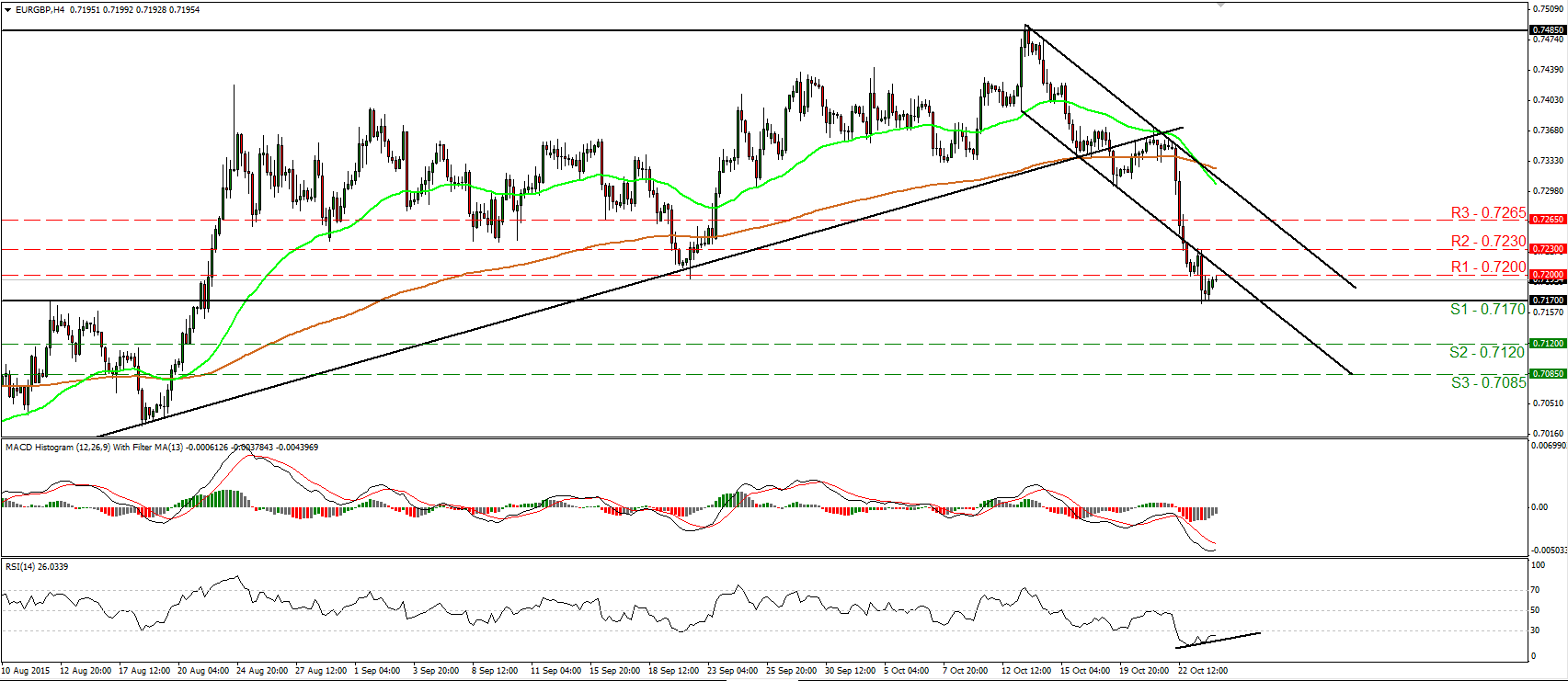

EUR/GBP tumbles and hits support at 0.7170

• EUR/GBP traded lower on Friday after it found resistance near 0.7230 (R2) and the lower bound of a downside channel that had been containing the price action from the 13th of October until last Thursday. The pair fell below the 0.7200 (R1) key line, but found support at the 0.7170 (S1) hurdle and rebounded. I still believe that the short-term picture remains negative but for now, I see signs that the current rebound may continue. A break back above 0.7200 (R1) could bring the rate back within the channel and is likely to aim for another test at 0.7230 (R2). Our short-term momentum indicators corroborate my view that further upside correction is possible. The RSI has bottomed within its below-30 field, while the MACD, although negative, has bottomed and could emerge above its trigger line soon. I also see positive divergence between the RSI and the price action. On the daily chart, I see that the rate started falling after it hit resistance near the key level of 0.7485. The recent declines also confirmed the negative divergence between our daily oscillators and the price action. However, I need a clear close below the strong hurdle of 0.7170 (S1) before I get confident on the downside again.

• Support: 0.7170 (S1), 0.7120 (S2), 0.7085 (S3)

• Resistance: 0.7200 (R1), 0.7230 (R2), 0.7265 (R3)

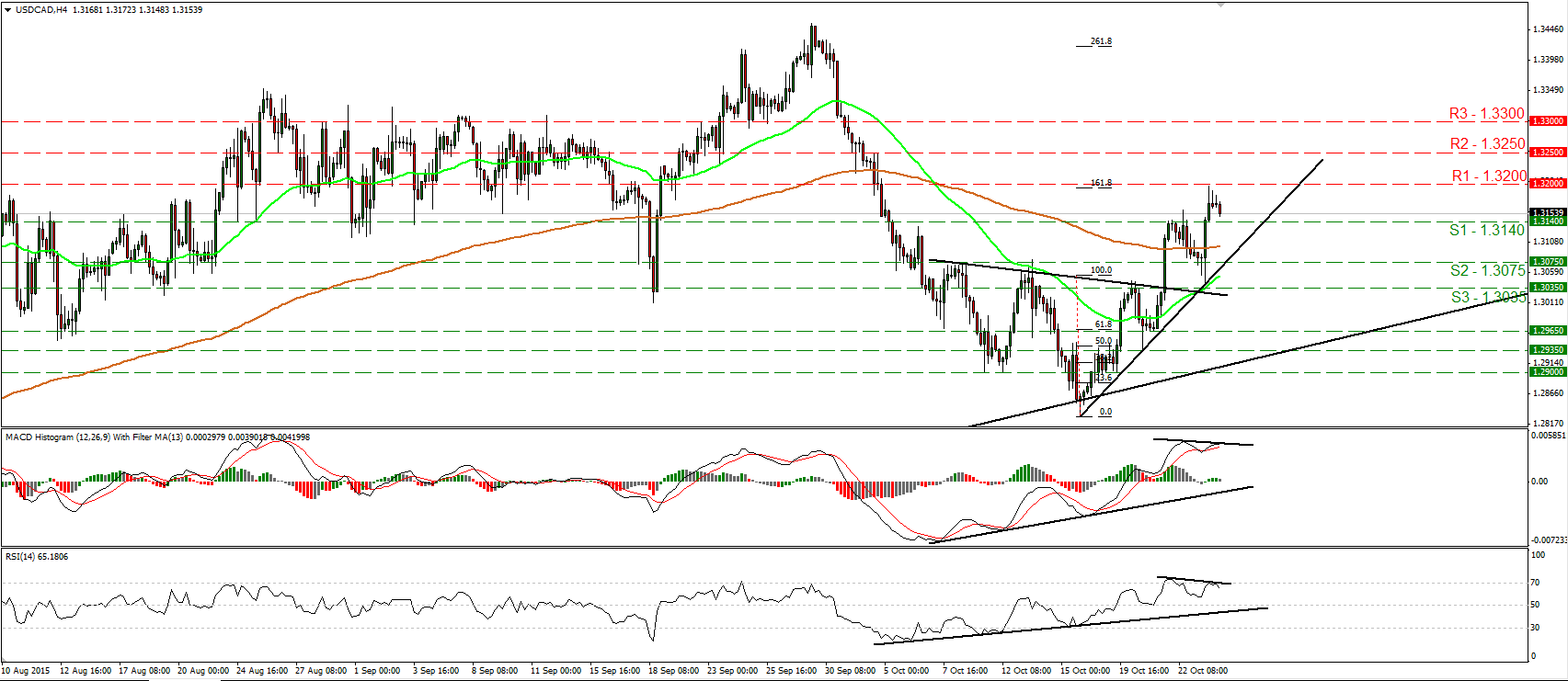

USD/CAD hits the 1.3200 zone following the weak Canadian CPI data

• USD/CAD rallied again after Canada’s inflation rate declined more than expected in September. The rate hit the uptrend line taken from the low of the 15th of October, shot up, and managed to hit resistance near the 1.3200 (R1) zone, which stands very close to the 161.8% extension level of the height of the inverted head and shoulders formation completed last Wednesday. As long as the rate is trading above the aforementioned uptrend line, I would consider the near-term path to stay positive. However, our momentum studies provide evidence that a pullback back below 1.3140 (S1) is likely for now. The RSI hit resistance at its 70 line and turned down, while the MACD shows signs of topping and could fall below its trigger soon. There is also negative divergence between both the indicators and the price action. On the daily chart, I see that on the 16th of October, the pair rebounded from the medium-term uptrend line taken from the low of the 14th of May. This keeps the longer-term outlook positive as well and increases the possibilities for the pair to trade higher in the foreseeable future.

• Support: 1.3140 (S1), 1.3075 (S2), 1.3035 (S3)

• Resistance: 1.3200 (R1), 1.3250 (R2), 1.3300 (R3)

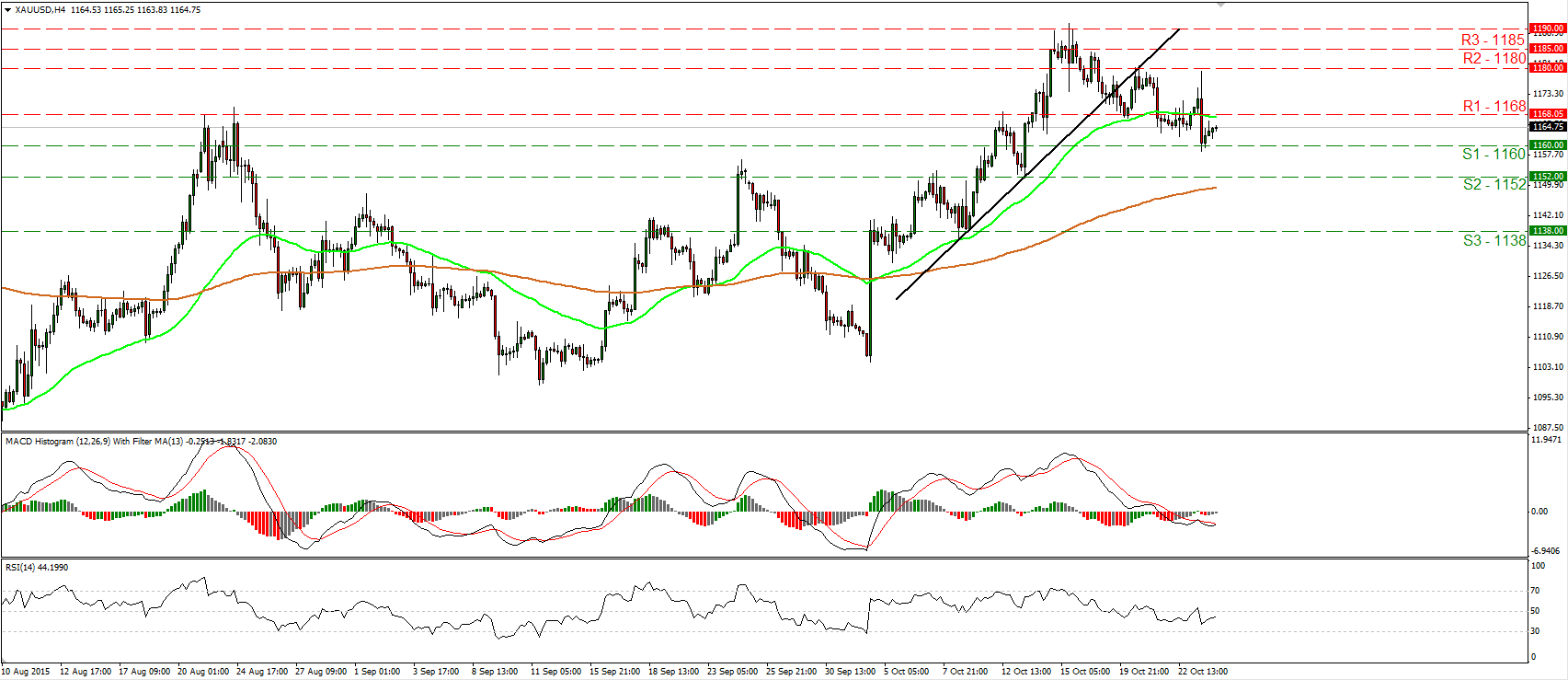

Gold finds resistance near 1180 and slides to hit 1160

• Gold traded lower on Friday after it found resistance at the 1180 (R2) resistance zone. However, the decline was halted near the 1160 (S1) barrier and then the metal rebounded. Although the price structure still suggests a short-term downtrend, I see the likelihood for the rebound to continue for a while. A clear move above 1168 (R1) could reaffirm the case and perhaps open the way for another test around the 1180 (R2) territory. Our short-term oscillators support further rebound as well. The RSI, although below its 50 line, has turned up again, while the MACD has bottomed and looks able to move above its signal line any time soon. On the daily chart, the longer-term outlook remains somewhat positive. As a result, I would consider the retreat started on the 15th of October as a corrective phase, at least for now.

• Support: 1160 (S1), 1152 (S2), 1138 (S3)

• Resistance: 1168 (R1), 1180 (R2), 1185 (R3)

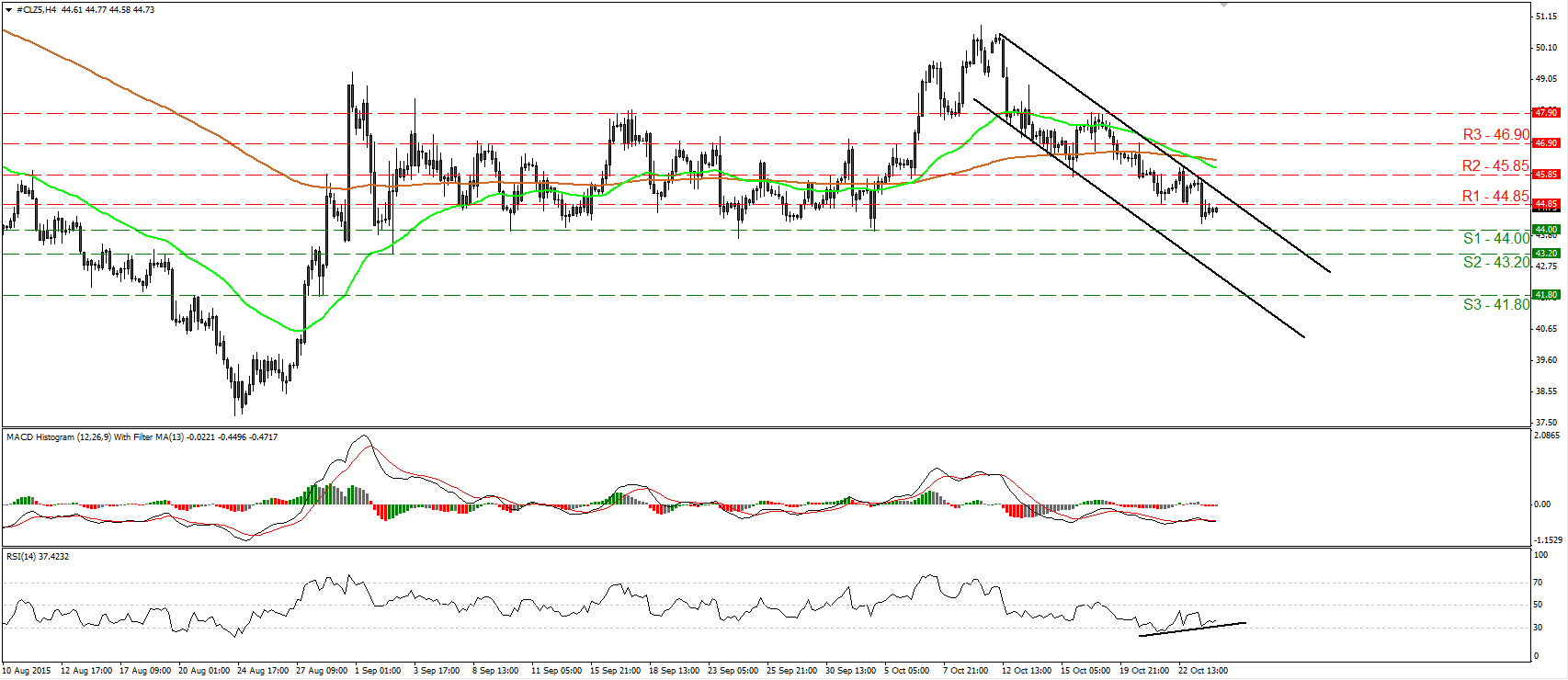

WTI falls below 44.85

• WTI slid on Friday and fell below the support (now turned into resistance) of 44.85 (R1). Nevertheless, the decline fell short of reaching the key hurdle of 44.00 (S1) and rebounded from slightly above it. The price is still trading within a downside channel and this keeps the short-term outlook negative in my view. Our short-term oscillators though, give evidence that the current bounce may continue a bit more, even back above the 44.85 (R1) line or above the upper bound of the channel. The RSI rebounded from near its 30 line and is now pointing up, while the MACD shows signs of bottoming and could move above its trigger line soon. There is also positive divergence between the RSI and the price action. On the daily chart, WTI printed a higher high on the 9th of October and there is still the possibility for a low near the key zone of 44.00 (S1). As a result, I would consider the medium-term picture to stay cautiously positive and I would treat the short-term downtrend as a corrective phase, at least for now.

• Support: 44.00 (S1), 43.20 (S2), 41.80 (S3)

• Resistance: 44.85 (R1), 45.85 (R2), 46.90 (R3)