Tageskommentar | 26/05/2017

Oil prices drop on a “buy the rumor, sell the fact” trade

• Yesterday, OPEC and non-OPEC producers concluded their meeting in Vienna, agreeing to extend the duration of the November output-cut deal by 9 months at the previous volume of 1.8 mbpd. However, even though the producers reached an accord, oil prices dropped in the aftermath of the event, which in our view reflects a “buy the rumor, sell the fact” reaction. An extension of 9 months was widely anticipated by markets, suggesting that all of the good news may have already been priced in. Thus, some investors that were looking for a longer extension or deeper cuts in production may have been left disappointed, which caused WTI prices to drop.

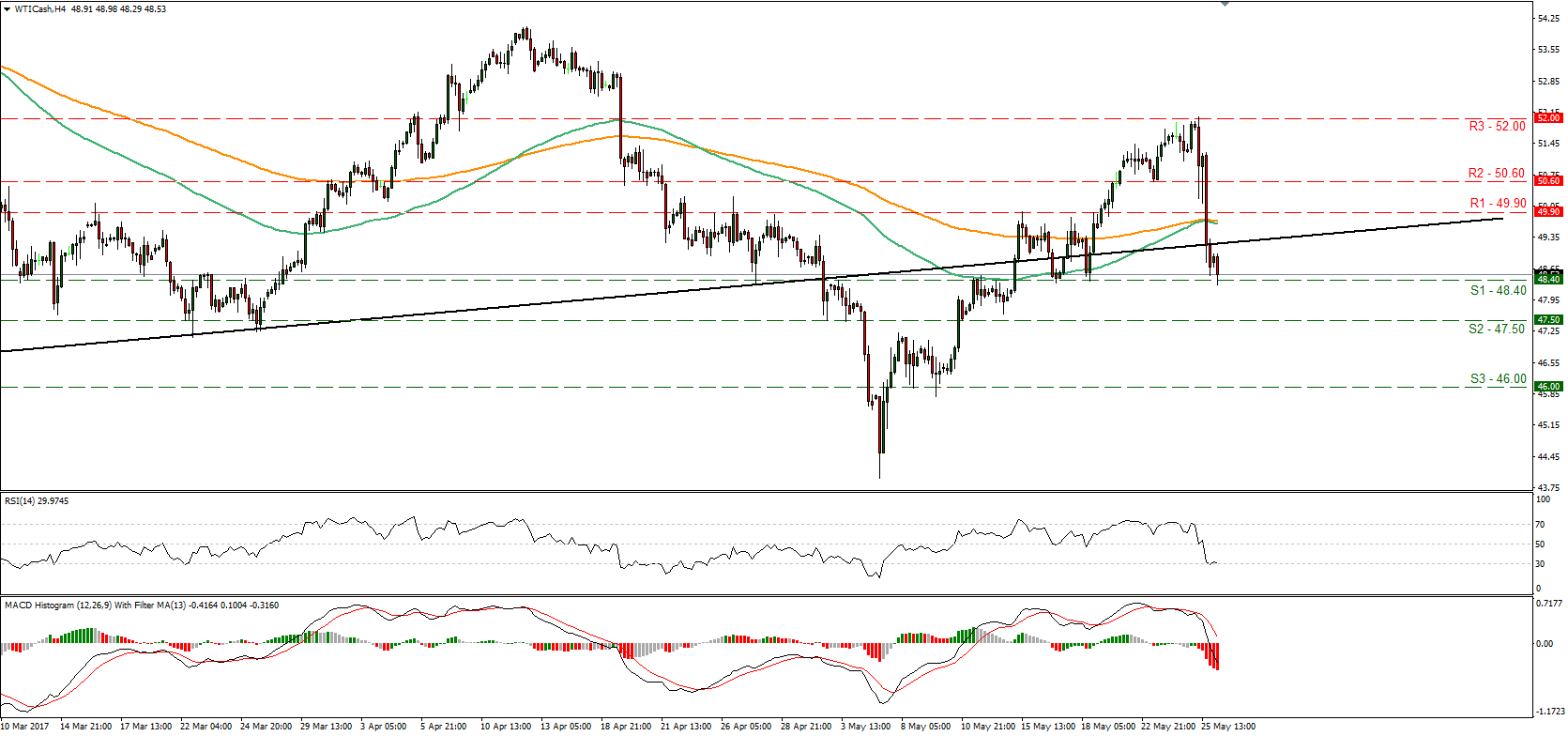

• WTI fell below two support (now turned into resistance) levels in a row and the longer-term upside support line taken from the low of the 5th of April 2016. The decline was halted near the 48.40 (S1) support level. Even though the price structure on the 4-hour chart suggests the near-term outlook is cautiously negative, in order for us to get confident on further declines, we would like to see a decisive break below the 44.00 zone. Such a break would signal a forthcoming lower low on the 4-hour chart, and may set the stage for further downside extensions.

• As for the bigger picture, we stick to our view that a long-term healthy uptrend in oil prices is still unlikely. The continued increase in US production – evident by the recent EIA data as well as the recovery in the Baker Hughes oil rig count – is likely to keep a lid on any significant gains in the precious liquid’s price. In addition, there is also the risk that the nations which are exempted from the production cuts, Libya and Nigeria, raise their output notably in the future, thereby offsetting some of the cuts from the other producers.

Sterling takes a hit from an election opinion poll

• The British pound dipped overnight, following the release of a UK election opinion poll by YouGov. The poll showed that although the Conservatives are still ahead, Labour is catching up, with the two parties expected to secure 43% and 38% respectively. Considering that the FT’s rolling average of polls currently shows the two parties at 46% and 33%, this poll likely triggered speculation that this election race may actually be closer than previously anticipated.

• In our view, fresh polls showing that the gap between these two parties continues to narrow could prove negative for sterling, on concerns that Theresa May and the Conservatives may not secure the strong majority they are seeking in Parliament. Finally, we believe that the British pound could become increasingly more sensitive to incoming polls as we approach Election Day, given that polls released just a few days ahead of the event may capture voters’ sentiment more accurately and thereby, carry more importance for investors.

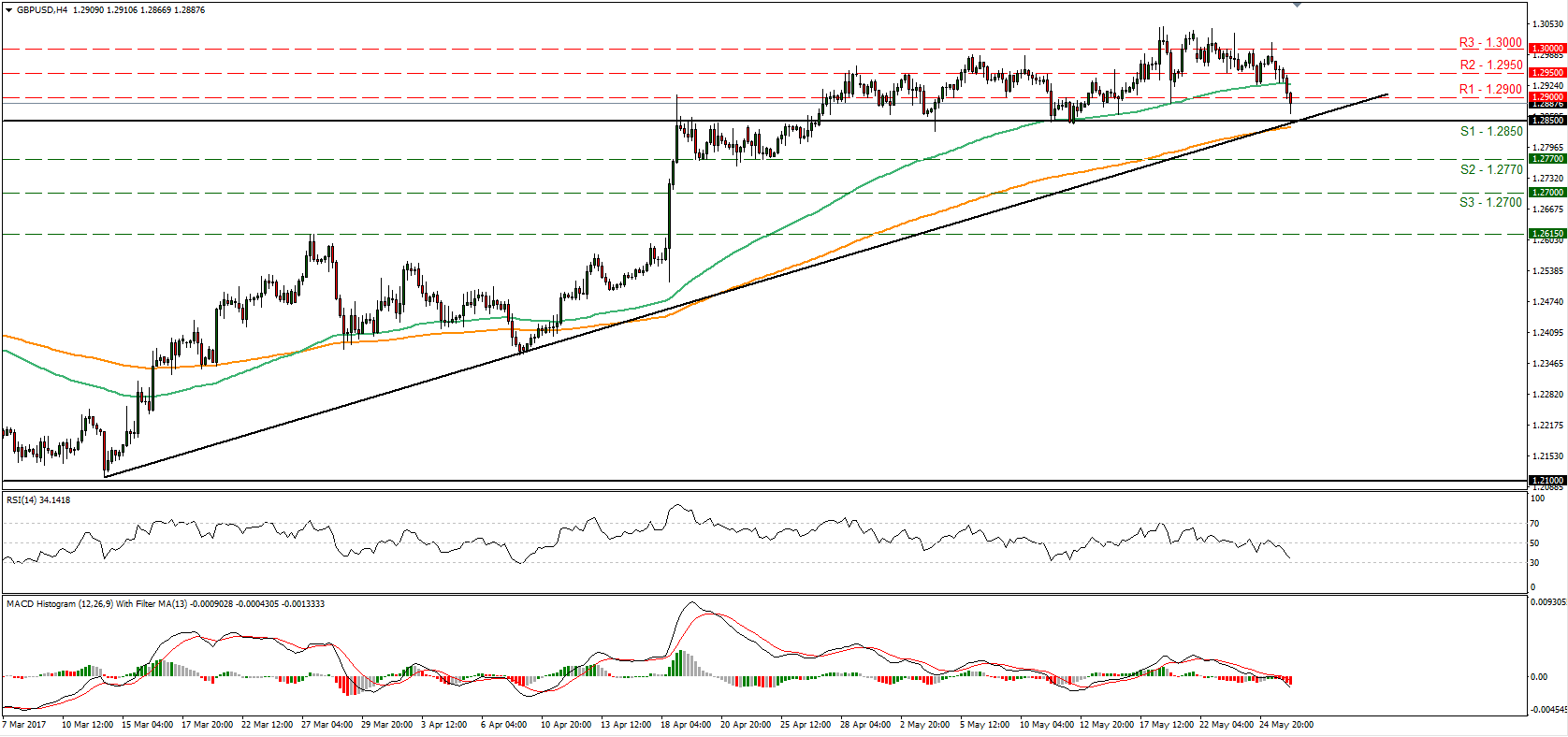

• GBP/USD fell overnight, breaking below the support (now turned into resistance) level of 1.2900 (R1). During the early European morning Friday, the pair looks to be headed for a test near the crossroad of the 1.2850 (S1) key support zone and a short-term uptrend line taken from the low of the 14th of March. New polls that show the Labour party catching up even further could trigger further declines in Cable. If the bears manage to overcome the aforementioned crossroad, they could initially aim for the next support hurdle at 1.2770 (S2).

Today’s highlights:

• The European morning is relatively quiet, with no major indicators due to be released. The only event that could attract some attention is the G7 summit in Italy. We think that market focus will be on the language the G7 use about free trade, considering that after US President Trump got elected, the G20 dropped their commitment to “resist all kinds of protectionism”.

• In the US, durable goods orders for April are due out. The forecast is for the headline print to have declined, while the core figure is expected to have risen, a rebound from previously. We share the view for a decline in the headline print, considering the slowdown in civilian aircraft orders in April, while we see the risks surrounding the core forecast as skewed to the downside. We base this view on the nation’s ISM manufacturing PMI, which showed that new orders slowed down notably during the month. Soft durable goods orders could bring USD under renewed selling interest.

• As for the rest of the US data, we also get the 2nd estimate of GDP for Q1. Expectations are for economic growth to have been revised upwards, albeit slightly. However, we doubt that it will have a significant market impact, given that the Fed has already pointed that it considers the soft growth in Q1 as transitory. As a result, we expect investors to pay more attention to incoming US data for Q2 (such as durable goods orders), as well as the Atlanta Fed GDPNow model, in order to get a better picture of whether economic growth has rebounded.

• We have one speaker on the agenda: ECB Executive Board member Benoit Coeure.

WTI

• Support: 48.40 (S1), 47.50 (S2), 46.00 (S3)

• Resistance: 49.90 (R1), 50.60 (R2), 52.00 (R3)

GBP/USD

• Support: 1.2850 (S1), 1.2770 (S2), 1.2700 (S3)

• Resistance: 1.2900 (R1), 1.2950 (R2), 1.3000 (R3)